I want to return to France to give back my experience, skills, and technical knowledge to the country of my heritage. France’s industrial economy is in the doldrums, but new policies are stimulating innovation, the key to economic growth and productivity, and technology industry leaders in France with strong technology industry backgrounds are looking to contribute to this new economy in France. I want to join them and give back.

In less than 24 hours since our campaign launch, we are nearing 10% of our goal

I am a native-born Californian with French family heritage and a French wife. We are both French citizens preparing to return to France. My university background is in the Humanities and Social Sciences, with a year of graduate study at Oxford University, researching in the Bodleian Library. When I returned to northern California, I eventually landed an entry-level job at Intel Corporation, which proved to be the crucible for my entire career. I eventually rose to be a senior executive in international business development with Intel. I have continued in international business for all of my career, working for a number of tech startups and venture capital investment firms over the years. I have led two tech industry consortia to develop global industry standards. I have been the director of a tech entrepreneurial incubator in Silicon Valley for the government of New Zealand and collaborated on mentoring promising entrepreneurs in locations here and around the world. I was an Adjunct Professor of Management at the University of British Columbia for four years.

I want to return to France to give back my experience, skills, and technical knowledge to the country of my heritage. France’s industrial economy is in the doldrums, but new policies are stimulating innovation, the key to economic growth and productivity, and technology industry leaders in France with strong technology industry backgrounds are looking to contribute to this new economy in France. I want to join them and give back.

I am now semi-retired, but very eager to return permanently to France to donate my technology industry experience and knowledge to assist French entrepreneurs to transform France into an innovation-based economy.

FundRazr Campaign Story:

We are David Mayes and Isabelle Roux-Mayes, a married couple, who are also French citizens. I am also a native Californian who has spent my career working for a number of Silicon Valley companies and investment firms, beginning with Intel Corporation. I am now semi-retired, but very eager to return permanently to France to donate my technology industry experience and knowledge to assist French entrepreneurs to transform France into an innovation-based economy. I am focusing specifically on building working relationships with three major new initiatives that could benefit from my background and achievements: The Camp in Aix-en-Provence, launched last year, Startup Garage, Paris, and 1kubator in Bourdeaux.

I am more than happy to share my achievements and references to validate my credentials and verify my ability to make a serious contribution. You can start here with my LinkedIn profile and references David Mayes on LinkedIn. You may also contact me here or on FundRazr where we can discuss my crowdfunding project.

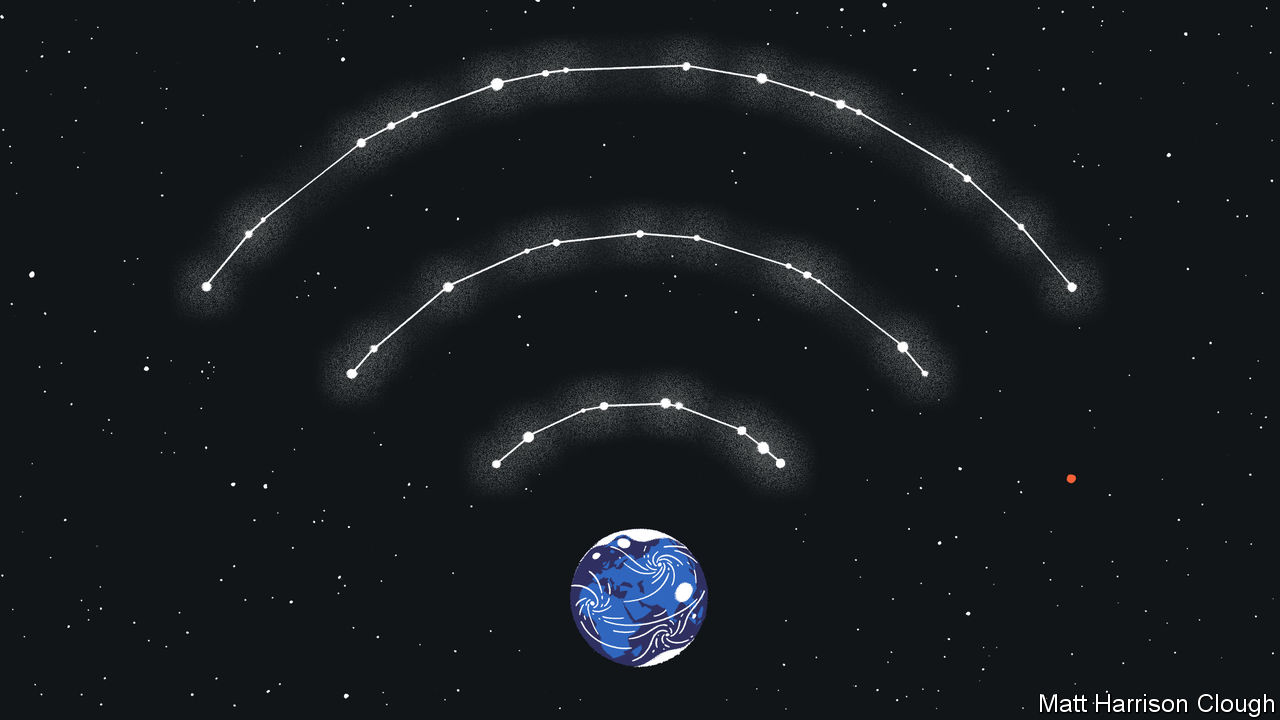

Years ago now Google quietly announced its “Loon Balloon Project” in New Zealand. The objective was to launch high altitude balloons that could potentially float over areas of the globe that did not yet have Internet access. The tech press predicted that the idea was “loony” indeed, though some called it “crazy cool.” Google has since also dabbled with the idea of low earth orbit satellites to achieve the same goal. With the rise of SpaceX, this seems an even more interesting technological approach, though other firms in the 1990s lost large amounts of money and failed. A modest aerospace company and a subsidiary of Airbus in Toulouse France is manufacturing low-orbit internet access satellites, hoping to launch as many as 650 such satellites. The idea that is captivating me is the potential for space-based Internet access to potentially provide an alternative to growing political and corporate control and Balkanization of the Internet.

Net Neutrality May Yet Be Achievable…Maybe

Years ago now Google quietly announced its “Loon Balloon Project” in New Zealand. The objective was to launch high altitude balloons that could potentially float over areas of the globe that did not yet have Internet access. The tech press predicted that the idea was “loony” indeed, though some called it “crazy cool.” Google has since also dabbled with the idea of low earth orbit satellites to achieve the same goal. With the rise of SpaceX, this seems an even more interesting technological approach, though other firms in the 1990s lost large amounts of money and failed. A modest aerospace company and a subsidiary of Airbus in Toulouse France is manufacturing low-orbit internet access satellites, hoping to launch as many as 650 such satellites in a “global constellation”. The idea that is captivating me is the potential for space-based Internet access to potentially provide an alternative to growing political and corporate control and Balkanization of the Internet.

OneWeb Launches First Six Internet Access Satellites

Ariane Soyuz rocket launch with six OneWeb satellites on board. February 27, 2019

Political Internet Censorship And Access In Developing World Potentially Solvable

But business challenges and technical problems remain

Aclear plastic box the size of a sofa sits in an underground factory in the suburbs of Toulouse in southern France. Inside it, a nozzle fixed to a robot arm carefully drips translucent gloop onto bits of circuitry. This is to help get rid of excess heat when the electronics start to operate. The slab that is created is then loaded onto a trolley and taken away as the next piece of electronics arrives for the same treatment.

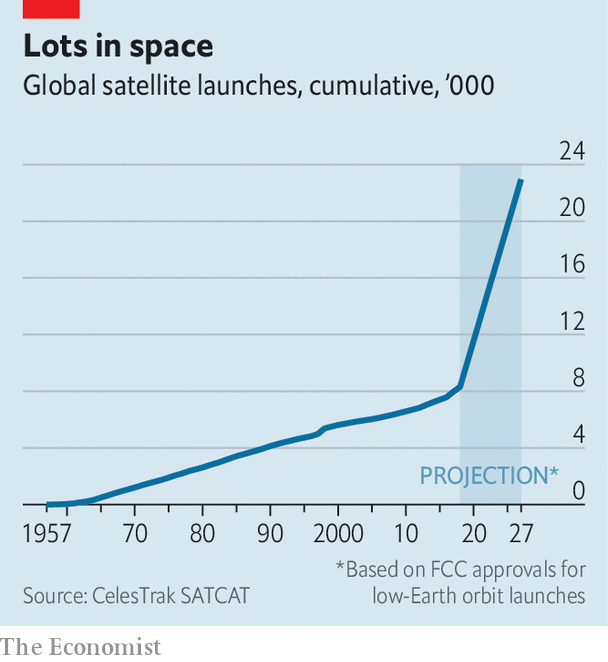

This is what the mass production of satellites looks like. Making them in quantity is a necessity for OneWeb. The company was founded in 2012, and it has yet to launch a single satellite. Yet it plans to have 900 in orbit by 2027. That seems a tall order. Intelsat, the firm which currently operates more communications satellites than any other, has been around for 54 years and has launched just 94.

OneWeb, which is part-owned by Airbus, a European aerospace giant, and SoftBank, a Japanese tech investor, needs such a large quantity of satellites because it wants to provide cheap and easy internet connectivity everywhere in the world. Bringing access to the internet to places where it is scarce or non-existent could be a huge business. Around 470m households and 3.5bn people lack such access, reckons Northern Sky Research, a consultancy. OneWeb is one of a handful of firms that want to do so. They think the best way to widen connectivity is to break with the model of using big satellites in distant orbits and instead deploy lots of small ones that sit closer to the ground.

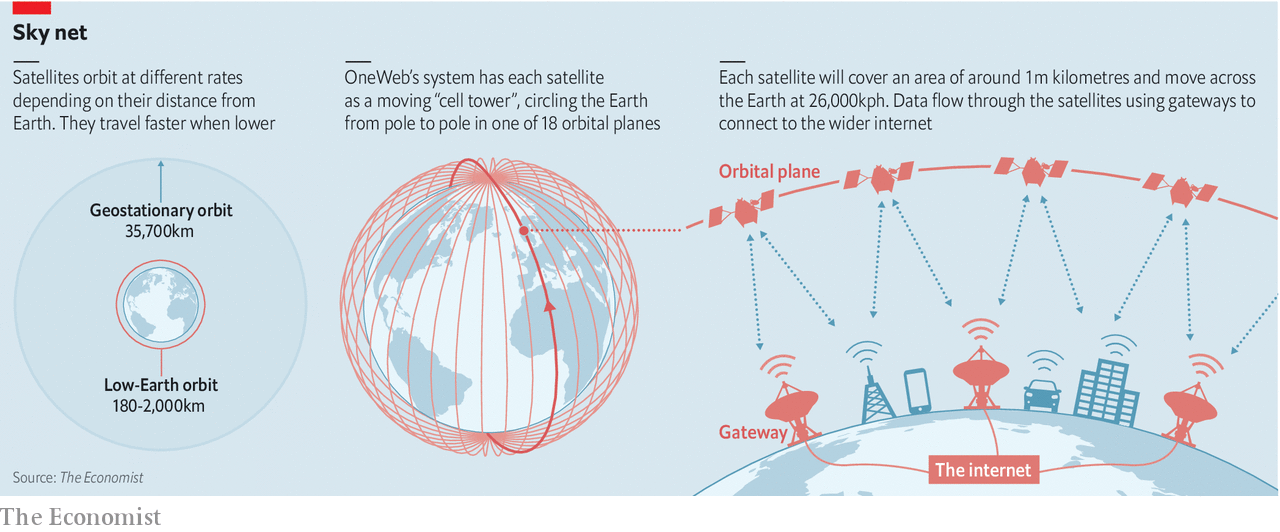

The rate at which an object orbits depends on how far away it is. At a distance of 380,000km, the Moon takes a month to travel around the Earth. The International Space Station, around 400km up, buzzes round in an hour and a half. In between, at an altitude of about 36,000km, there is a sweet spot where satellites make an orbit once a day. A satellite in this orbit is thus “geostationary”—it seems to sit still over a specific spot. Almost all today’s satellite communications traffic, both data and broadcasts, goes through such satellites.

The advantage of a geostationary orbit is that the antennae that send data to the satellite and those that receive data coming down from it do not need to move. The disadvantage is that sending a signal that far requires a hefty antenna and a lot of power. And even at the speed of light, the trip to geostationary orbit and back adds a half-second delay to signals. That does not matter for broadcasts, but it does a little for voice, where the delay can prove tiresome, and a lot for some sorts of data. Many online services work poorly or not at all over such a connection. And it always requires a dish that looks up at the sky.

Head in the clouds

Ships, planes and remote businesses rely for internet connections on signals sent from geostationary orbit, but this method is too pricey for widespread adoption. Beaming the internet via satellites orbiting closer to the planet has been tried before. The idea was popular at the height of the tech boom of the late 1990s. Three companies—Teledesic, Iridium and Globalstar—poured tens of billions of dollars into the low-Earth orbit (leo) satellite internet. It culminated in the collapse of Teledesic. Although the technology of the time worked, it was very costly and so the services on offer had to be hugely expensive, too. Iridium survived, but as a niche provider of satellite telephony, not a purveyor of cheap and fast internet access.

OneWeb is among several firms that are trying leo satellites again. SpaceX, a rocket company founded by Elon Musk, a tech entrepreneur, is guarded about its proposed system, Starlink, but on November 15th American regulators approved an application for 7,518 satellites at an altitude of 340km (bringing the total for which the firm has approval to nearly 12,000). Telesat, a Canadian firm, has plans for a 512-satellite constellation. LeoSat, a startup with Japanese and Latin American backers, aims to build a 108-satellite network aimed at providing super-fast connections to businesses. Iridium, still in the game, will launch the final ten satellites in its new constellation of 66 by the end of the year. Not to be outdone, a Chinese state-owned firm recently announced the construction of a 300-satellite constellation. In ten years’ time, if all goes to plan, these new firms will have put more satellites into orbit by themselves than the total launched to date (see chart).

These companies want to avoid the technical issues of geostationary satellites by putting theirs into a low orbit, where the data will take only a few milliseconds to travel to space and back. And because signals need not be sent so far the satellites can be smaller and cheaper. OneWeb claims they might weigh 150kg and cost a few hundred thousand dollars, compared with a tonne or more, and tens or even hundreds of millions of dollars, for the geostationary sort.

Floating in a most peculiar way

At 1,200km up, where OneWeb intends its first satellites to operate, they do not sit still in the sky. A satellite overhead will sink below the horizon seven minutes later. That has two consequences. First, to ensure that a satellite is always available to any user, a great many are required. Second, to talk to such a satellite you need an antenna that can track it across the sky.

One way to understand this is as a cellular-phone network turned inside out. On Earth, cell-phone towers are fixed; a user’s phone talks to the closest or least busy one, which may change as the user moves or traffic alters. In OneWeb’s system each satellite is a moving cell tower, circling the Earth from pole to pole in one of 18 orbital planes that look like lines of longitude (see diagram). The 900 cells, each one covering an area of a bit more than 1m kilometres, skim across the Earth at 26,000km an hour. Clever software hands transmission from one satellite to the next as they move into and out of range.

There are three ways to connect to such a network. One is to place an antenna on a terrestrial cell tower, which can use the satellites to get data to and from a mobile-phone network, in place of the fibre optic, microwave or cable links that are normally used. The second is for homes and businesses to have their own ground terminals, smaller and cheaper antenna that can talk to the satellite. The third is for vehicles to have ground terminals. This might be important for driverless cars, which will need to transmit and receive large volumes of data over an area which may be broader than that covered by appropriate terrestrial cellular networks.

In all cases data will make their way to the wider internet through large ground-based dishes, called gateways. An email sent from a house connected to one of the new satellite network, for example, would travel up to a passing satellite, down to a gateway then onward to its destination.

The firms involved today hope to overcome the obstacles confronting the previous generation of leo satellite firms because building and launching hundreds of satellites is now much cheaper. The cost of launch in particular has tumbled in the past decade with the arrival of better rockets and more competition. OneWeb has a contract, reportedly valued at over €1bn ($1.1bn), for 21 launches with Arianespace, a European consortium. Russian-built Soyuz craft will also take 34 to 36 satellites up at a time from either French Guiana or Kazakhstan. OneWeb may later use Blue Origin, a rocket firm owned by Amazon’s founder, Jeff Bezos; it also has a contract for launching single satellites to replace ones that break down with Virgin Orbit. Virgin Group, like Airbus and SoftBank, is an investor in the company. SpaceX intends to launch its satellites on its own rockets.

Space to grow

The bigger challenge is making satellites quickly and cheaply enough to fill up these rockets. It typically takes existing satellite-makers two years to build one after contracts are signed. They are not up to the challenge, says Jonny Dyer, who worked on a Google project that first brought the OneWeb team together (but stayed with Google when the two parted ways). “The supply chain does not scale,” he says. “They’re not used to working at those volumes, and they’re not used to the unit cost.”

OneWeb and SpaceX thus not only have to make new satellites, they have to build a system for building satellites. OneWeb has been doing so in Toulouse for the past two years. Its first satellite was completed in April and ten more will be ready in time for the company’s first launch, some time before February 2019. To step up manufacture, OneWeb is building two copies of its production line in a new factory in Florida. It hopes to have the first satellite from this facility ready before March 2019 and to raise output to ten a week not long after.

The factory floor in Toulouse has separate workstations for propulsion systems, communications payload, solar panels and so on. Satellites in the making move on robot carts from one station to the next. Cameras track the components and look out for errors—misalignments and the like. The finished cube is about the size of a beach ball bedecked with antennae and solar panels. After testing, it is shipped out. The system has had teething problems. The first launch will be more than a year behind schedule. But Greg Wyler, OneWeb’s boss, says he still hopes to offer connectivity in places in higher northern latitudes, such as Alaska and Britain, by the end of 2019.

Putting satellites in place is only part of the problem. How useful they will prove to be depends on designing and building antennae to get data to homes or vehicles that are not close to terrestrial cell towers. “The elephant in the room…has always been the ground terminal,” says Nathan Kundtz, the former boss of Kymeta, which makes antennae. Mr Kundtz says that tracking satellites across the sky mechanically is untenable if the antennae are to be affordable and widely used. His firm does tracking electronically. No moving parts, he says. Teledesic failed in part because no such ground terminal existed in the late 1990s. Fortunately, the necessary electronics have shrunk in size and cost.

Aerial combat

Firms such as Kymeta, along with at least two other companies, Phasor and Isotropic Systems, are producing flat, electronically “steerable” antennae with no moving parts that can send and receive signals from leo satellites. Kymeta’s antenna is the least orthodox. It relies upon the same kind of lcddisplay found in laptops and flat-screen televisions. Instead of using the 30,000 pixels in its screen to display images, it uses them to filter and interpret the satellite signal by allowing it to pass through at some pixels and blocking it at others. Different patterns of pixels act like a lens, focusing the signal onto a receiver beneath them; the pattern shifts up to 240 times a second, changing the shape of the “lens” and thus keeping track of the satellites overhead. Phasor’s system works similarly, but uses an electronically controlled array of microchips to perform the same task. Isotropic Systems, which has said that it is developing an antenna that will be able to receive signal from OneWeb’s satellites, uses an optical system more like Kymeta’s.

Kymeta and Phasor have both said that they do not want to sell antennae directly to consumers, but will focus on businesses, cellular networks, maritime and aviation customers instead. Isotropic Systems has announced that it will use its technology to produce a “consumer broadband terminal” in time for OneWeb’s launch. Once available, consumers are most likely to get the new pizza-size antennae through their internet service providers. But if it is too expensive for people to receive signals on the ground—most of the world’s unconnected are poor—those ventures selling direct to consumers will struggle. Mr Wyler says his firm needs antennae that cost $200 at most for the consumer business to thrive.

Telesat, the next biggest firm in terms of constellation size, is taking a different approach. It does not plan to offer services to consumers directly, but instead is focusing on filling in gaps for cellular networks, as well as businesses, ships and planes. Specialised telecoms companies would buy bandwidth and resell it. In contrast to Messrs Wyler and Musk, and their aspirations for global coverage, Telesat has divided the surface of the planet into thousands of polygons, and modelled exactly in which ones it makes financial sense to offer strong connectivity. This means its constellation needs fewer expensive gateways.

Mr Wyler, in contrast, is known as something of a connectivity evangelist. His first satellite internet firm, o3b (Other 3 Billion), placed large satellites in a higher orbit, providing a connection only slightly slower than a leosatellite. Now owned by ses, a larger satellite company, o3b specialises in providing connectivity to islands that are otherwise cut off. OneWeb’s goal of connecting consumers is largely in the hands of SoftBank, its main investor, which owns the exclusive rights to sell the new bandwidth.

Even if the new satellites bring the internet to people and parts of the planet that have been ill-served up until now, putting ever more objects in space brings another set of difficulties. Satellites in densely packed constellations may crash into each other or other spacecraft. “If there are thousands [of satellites] then they’ll have much higher probability of colliding,” says Mr Dyer. “If there is a collision in these orbits it will be a monumental disaster. At 1,000km, if there’s an incident it will be up there for hundreds of years.” Geostationary satellites, because they do not move relative to each other, are unlikely to collide.

Managing constellations is particularly difficult, says Mr Wyler, because each satellite has only a tiny amount of power to work with (equipping small ones with bigger thrusters would be hugely expensive). So even if a crash were imminent, there would be little that could be done about it other than watch. “What are you gonna do? Nothing. Get popcorn. There’s nothing to do,” says Mr Wyler. OneWeb has designed its constellation so that faulty satellites fall out of orbit immediately to avoid this risk.

Access all areas

The new constellations will also raise tricky questions of national jurisdiction. Countries generally have control of the routers which connect them to the wider terrestrial internet. Satellites threaten that control. The national regulators that OneWeb has talked to are uneasy, says Mr Wyler, because it would create a route to the internet that countries could not monitor. OneWeb’s intention is to build 39 “gateways” on the ground around the world that will beam up and receive traffic from its satellites.

The first is under construction in Svalbard, a remote Norwegian island chain. These access points, and those planned by other firms, present another difficulty. Some countries are willing to share gateways with other countries. Others want their own because they are concerned that third parties will be able to monitor internet traffic, potentially using it to hack data flows of national importance.

Questions remain about whether the businesses involved can do all they promise cheaply enough. But if these companies succeed, their impact will go beyond helping to bring 3.5bn people online. Mr Musk has hazy plans to use Starlink as the foundation for a deep-space network that will keep spacecraft connected en route to Mars and the Moon.

With a network of satellites encircling the planet, humans will soon never be offline. High-quality internet connections will become more widespread than basic sanitation and running water. The leo broadband firms are trying to reinvent the satellite industry. But the infrastructure they are planning will provide a platform for other industries to reinvent themselves, too.

Correction (December 11th, 2018): This piece originally stated that Intelsat has launched 59 satellites in its 54-year history. That is the number of active satellites the firm has in orbit. The firm has successfully launched 94. Sorry.

In one of the more bizarre recent articles on the state of the Canadian venture investment market, The Globe & Mail offered this story of the entry of Canadian commercial banks like CIBC, RBC and TD into the world of entrepreneurial finance. Not more than a few weeks ago, Toronto University Professor Richard Florida also published an opinion piece in the Globe & Mail, in sharp contrast which is entitled “Canada is losing the global innovation race”, describing the long term decline of Canadian venture capital and decades of poor investment in basic R&D compared to its other OECD industrialized nations. Recently, a colleague in Canadian venture capital told me of his retirement, citing the enormous difficulty his firm had raising capital from the Canadian financial industry. This is prima facie evidence of how disconnected Canada is from the reality of entrepreneurial finance and venture capital. The Canadian financial industry mindset is Problem One. Name another major entrepreneurial ecosystem that operates like this.

Canada’s Entrepreneurial Finance Industry Is Living In A Bubble

Bank ‘slugfest’ leaves the Canadian tech sector piled high with cheap debt offers

Canadian Entrepreneurs Are Being Exploited By The Banking Elite While VC’s Struggle To Raise Capital

In one of the more bizarre recent articles on the state of the Canadian venture investment market, The Globe & Mail offered this story of the entry of Canadian commercial banks like CIBC, RBC and TD into the world of entrepreneurial finance. Not more than a few weeks ago, Toronto University Professor Richard Florida also published an opinion piece in The Globe & Mail, in sharp contrast which is entitled “Canada is losing the global innovation race”, describing the long term decline of Canadian venture capital and decades of poor investment in basic R&D compared to its other OECD industrialized nations. Recently, a colleague in Canadian venture capital told me of his retirement, citing the enormous difficulty his firm had raising capital from the Canadian financial industry. This is prima facie evidence of how disconnected Canada is from the reality of entrepreneurial finance and venture capital. The Canadian financial industry mindset is Problem One. Name another major entrepreneurial ecosystem that operates like this.

Banks spent 2018 fighting to give Canada’s fast-growing tech sector something it hasn’t had much taste for in years: debt.

Canadian scale-ups and venture-capital-firm partners spent much of the past year watching offers for debt financing pile higher than they can ever remember. In interviews with The Globe and Mail, founders, partners, and lenders used phrases like “slugfest” and “arms race” to describe the phenomenon. Both Canadian and American banks are racing to serve young tech companies, by improving loan terms and shoving down rates. This has reshaped how Canadian tech startups secure financing: Debt is so cheap that some small companies that would have never considered it are taking it on as a cushion, giving them extra runway between equity raises without diluting founders’ ownership.

The trend is partly a reflection of Canada’s tech sector’s coming-of-age after its post-financial-crisis doldrums. But it’s also the result of deliberate moves by two major players – one established in debt financing, the other making its return.

California’s Silicon Valley Bank is taking steps to formalize its ability to lend to Canadian clients and hopes to be fully licensed here early next year. Meanwhile, Canadian Imperial Bank of Commerce bought the private specialty-finance firm Wellington Financial in January with ambitions to better serve early- and mid-stage companies with broader banking services. In Wellington, CIBC found a team of experienced tech bankers after Canadian institutions largely shed that expertise in the long tail of the dot-com bust; in CIBC, Wellington found a lower cost of capital thanks to its scale, making debt cheaper to sell for clients.

While both players offer a suite of banking services, it’s been their debt offers that caused jaws to drop in Canada’s tech community in 2018 – and has pushed other lenders, including Royal Bank of Canada and Bank of Montreal, to try harder to entice startups with similar offerings.

While no one interviewed for this story would share numbers on specific rate offers they’d seen – rates vary across lenders as well as by company size, stage and revenue model – they all agreed that the past year saw remarkable drops in cost of capital. Two sources who were not authorized to share confidential rate proposals said that interest rate offers had fallen from 15 to 20 per cent a year ago, but now hover between 10 and 15 per cent, sometimes falling as low as 6 per cent.

“Entrepreneurs 10 years ago wouldn’t have known about venture debt – now they know about it,” says Mark Usher, the veteran technology banker who is managing director and North American market leader for CIBC Innovation Banking – Wellington’s new moniker – and chair of the Canadian Venture Capital & Private Equity Association.

Mr. Usher cautions that founders should be careful and seek the advice of their investors and board when considering debt financing – and warns, too, that the super-competitive Canadian market is not sustainable in the long run. “It will normalize back to historical returns and rates,” he says. “Venture-debt lenders will take losses at some point, then they’ll realize that they weren’t charging enough to make up for the losses, and that’s how it corrects.”

Many in the sector suggest the first sign of the shifting Canadian venture-debt ecosystem happened in March, when Vancouver social-media company Hootsuite Media Inc. signed a $50-million deal with the newly minted CIBC Innovation Banking, having previously largely worked with Silicon Valley Bank. (The American bank says Hootsuite also remains a current client.)

“Even if we never use it, it’s just a nice cushion, and it really doesn’t cost that much to have it,” says Sid Paquette, a managing partner at OMERS Ventures, who oversees the firm’s investment in Hootsuite. “At almost all of my companies … I’m doing a disservice if I don’t encourage them to take on a little bit of debt right now, because it is so cheap.”

Since then, venture-capital partners and tech executives say, the debt rally in Canada has been adopted by firms of all sizes and stages. Janet Bannister, general partner at Real Ventures in Toronto – which focuses on early-stage investments – says that many companies in her portfolio and on her radar are taking on debt financing, largely to accelerate growth without diluting owners’ stakes.

“The banks are increasingly saying, ‘We need to be the banking partners of these young companies, because some of them are going to grow up and be the next Shopify,’” Ms. Bannister says. Still companies need to be prepared for the debt, she says. “If the interest expenses become so onerous that they are impacting growth by forcing the company to curtail spending on things such as development, sales and-or marketing, that can become a problem.”

Bryn Jones, the co-founder of PartnerStack, a Toronto firm that helps software companies grow through partnerships, has spent the last few months evaluating term sheets. “The only banks that really cared before were from the Bay Area,” Mr. Jones says. Now, he continues, “everybody wants to get into it.” The phenomenon has been helpful for companies such as ChatKit, a Toronto e-commerce chat-marketing startup, which did a debt-financing round with CIBC Innovation Banking last July, says founder and chief executive Mazdak Rezvani. “To build a successful Series A round, you need metrics to appeal to an investor. A few extra months of runway really helps.”

Since the debt-rate battle began earlier this year, “all of the banks now have a tech-lending focus and strategy,” says Mr. Usher. His own firm, CIBC Innovation Banking, even hired tech financier Robert Rosen away from American rival Comerica Inc., a long-time leader in offering debt financing for Canadian startups.

Banks’ embrace of tech companies has in some cases turned into a talent war. Devon Dayton, who’d been a part of CIBC’s technology push, left to join the Bank of Montreal in April, just three months after the Wellington deal. He says he’s now charged with “accelerating” BMO’s tech coverage, including both through banking services and providing debt capital to the sector.

Royal Bank of Canada, meanwhile, turned to established Toronto tech lender Espresso Capital in August to partner for venture-debt deals. Espresso has funded more than 230 deals since 2009, the company says, and recently established a new program to lend to software-as-a-service cloud companies up to 24 times their monthly recurring revenue in growth financing, to a maximum of $10-million.

“For the longest time we were the beneficiary of a massively under-served market,” says Alkarim Jivraj, Espresso’s chief executive. Amid what he calls a “slugfest” between banks to offer debt, he says, “we continue to grow, even with the noise around us.”

A rash of Canadian debt-funding options have emerged, in fact, offering loans on such highly specific terms. Toronto’s Fundthrough offers cash advances between clients’ invoices; Clearbanc, co-founded by serial entrepreneur and Dragons’ DenDragon Michele Romanow – and which just raised US$120-million – helps finance young e-commerce businesses by fronting online ad revenue. “How you fund your company probably ends up being the most important decision you make as a founder,” Ms. Romanow says. “With equity, you never get to give it back …. Coming up with as much alternatives around that is really powerful.”

Silicon Valley Bank, which serviced Canadian businesses for about a dozen years but until recently, did so largely from offices in Seattle and Boston, is looking forward to a formal Canadian licence from the Office of the Superintendent of Financial Institutions.

“What the licence will give us in the new year is the opportunity to have feet on the street [and] meet with clients and investors in a more proactive kind of way,” says Barbara Dirks, the bank’s Canadian head. Her colleague Win Bear, who long worked for the lender’s Boston office, says that it’s a historic moment for startup financing – not just in Canada.

“There’s a lot more competition,” Mr. Bear says. “It’s really driven down pricing, much in the same way that increased competition on the growth equity side has increased valuations up to levels that some would argue are unprecedented.”

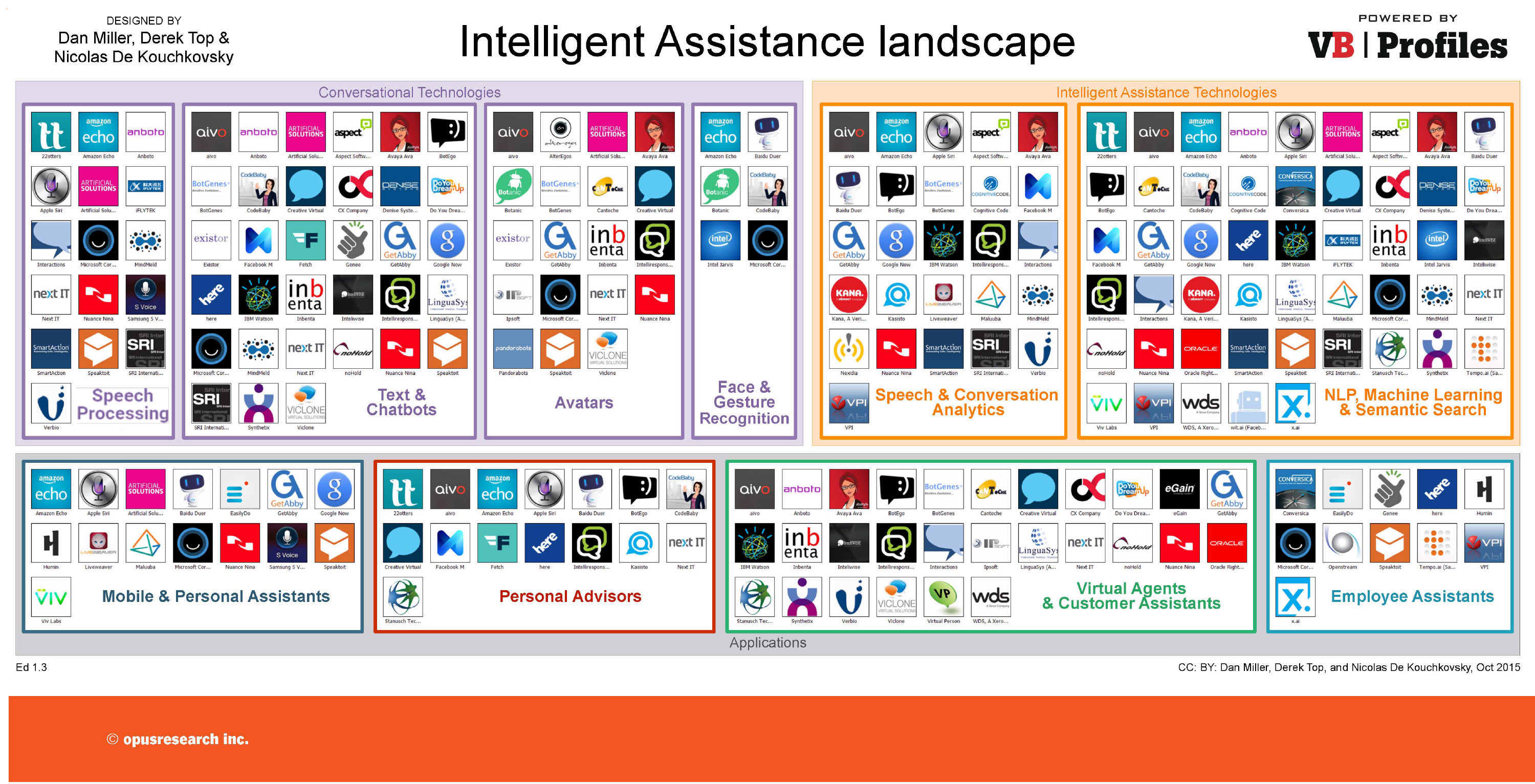

Five years ago, I wrote a post on this blog disparaging the state of the Internet of Things/home automation market as a “Tower of Proprietary Babble.” Vendors of many different home and industrial product offerings were literally speaking different languages, making their products inoperable with other complementary products from other vendors. The market was being constrained by its immaturity and a failure to grasp the importance of open standards. A 2017 Verizon report concluded that “an absence of industry-wide standards…represented greater than 50% of executives concerns about IoT. Today I can report that finally, the solutions and technologies are beginning to come together, albeit still slowly.

The Evolution of These Technologies Is Clearer

The IoT Tower of Proprietary Babble Is Slowly Crumbling

The Rise of the Intelligent Assistant

Five years ago, I wrote a post on this blog disparaging the state of the Internet of Things/home automation market as a “Tower of Proprietary Babble.” Vendors of many different home and industrial product offerings were literally speaking different languages, making their products inoperable with other complementary products from other vendors. The market was being constrained by its immaturity and a failure to grasp the importance of open standards. A 2017 Verizon report concluded that “an absence of industry-wide standards…represented greater than 50% of executives concerns about IoT.” Today I can report that finally, the solutions and technologies are beginning to come together, albeit still slowly.

One of the most important factors influencing these positive developments has been the recognition of the importance of this technology area by major corporate players and a large number of entrepreneurial companies funded by venture investment, as shown in the infographic above. Amazon, for example, announced in October 2018 that it has shipped over 100 Million Echo devices, which effectively combine an intelligent assistant, smart hub, and a large-scale database of information. This does not take into account the dozens of other companies which have launched their own entries. I like to point to Philips Hue as such an example of corporate strategic focus perhaps changing the future corporate prospects of Philips, based in Eindhoven in the Netherlands. I have visited Philips HQ, a company trying to evolve from the incandescent lighting market. Two years ago my wife bought me a Philips Hue WiFi controlled smart lighting starter kit. My initial reaction was disbelief that it would succeed. I am eating crow on that point, as I now control my lighting using Amazon’s Alexa and the Philips Hue smart hub. The rise of the “intelligent assistant” seems to have been a catalyst for growth and convergence.

The situation with proprietary silos of offerings that do not work well or at all with other offerings is still frustrating, but slowly evolving. Amazon Firestick’s browser is its own awkward “Silk” or alternatively Firefox, but excluding Google’s Chrome for alleged competitive advantage. When I set up my Firestick, I had to ditch Chromecast because I only have so many HDMI ports. Alexa works with Spotify but only in one room as dictated by Spotify. Alexa can play music from Amazon Music or Sirius/XM on all Echo devices without the Spotify limitation. Which brings me to another point of aggravation: alleged Smart TV’s. Not only are they not truly “smart,” they are proprietary silos of their own, so “intelligent assistant” smart hubs do not work with “smart” TV’s. Samsung, for example, has its own competing intelligent assistant, Bixby, so of course, only Bixby can control a Samsung TV. I watched one of those YouTube DIY videos on how you could make your TV work with Alexa using third-party software and remotes. Trust me, you do not want to go there. But cracks are beginning to appear that may lead to a flood of openness. Samsung just announced at CES that beginning in 2019 its Smart TV’s will work with Amazon Echo and Google Home, and that a later software update will likely enable older Samsung TV’s to work with Echo and Home. However, Bixby will still control the remote. Other TV’s from manufacturers like Sony and LG have worked with intelligent assistants for some time.

The rise of an Internet of Everything Everywhere, the recognition of the need for greater data communication bandwidth, and battery-free wireless IoT sensors are heating up R&D labs everywhere. Keep in mind that I am focusing on the consumer side, and have not even mentioned the rising demands from industrial applications. Intel has estimated that autonomous vehicles will transmit up to 4 Terabytes of data daily. AR and VR applications will require similar throughput. Existing wireless data communication technologies, including 5G LTE, cannot address this need. In addition, an exploding need for IoT sensors not connected to an electrical power source will require more work in the area of “energy harvesting.” Energy harvesting began with passive RFID, and by using kinetic, pizeo, and thermoelectric energy and converting it into a battery-free electrical power source for sensors. EnOcean, an entrepreneurial spinoff of Siemens in Munich has pioneered this technology but it is not sufficient for future market requirements.

Fortunately, work has already begun on both higher throughput wireless data communication using mmWave spectrum, and energy harvesting using radio backscatter, reminiscent of Nikola Tesla’s dream of wireless electrical power distribution. The successful demonstration of these technologies holds the potential to open the door to new IEEE data communication standards that could potentially play a role in ending the Tower of Babble and accelerating the integration of AI, IoT, and Big Data. Bottom line is that the market and the technology landscape are improving.

My IEEE Talk from 2013 foreshadows the development of current emerging trends in advanced technology, as they appeared at the time. I proposed that in fact, they represent one huge integrated convergence trend that has morphed into something even bigger, and is already having a major impact on the way we live, work, and think. The 2012 Obama campaign’s sophisticated “Dashboard” application is referenced, integrating Big Data, The Cloud, and Smart Mobile was perhaps the most significant example at that time of the combined power of these trends blending into one big thing.

READ MORE: Blog Post on IoT from July 20, 2013

The term “Internet of Things” (IoT) is being loosely tossed around in the media. But what does it mean? It means simply that data communication, like Internet communication, but not necessarily Internet Protocol packets, is emerging for all manner of “things” in the home, in your car, everywhere: light switches, lighting devices, thermostats, door locks, window shades, kitchen appliances, washers & dryers, home audio and video equipment, even pet food dispensers. You get the idea. It has also been called home automation. All of this communication occurs autonomously, without human intervention. The communication can be between and among these devices, so-called machine to machine or M2M communication. The data communication can also terminate in a compute server where the information can be acted on automatically, or made available to the user to intervene remotely from their smart mobile phone or any other remote Internet-connected device.

Another key concept is the promise of automated energy efficiency, with the introduction of “smart meters” with data communication capability, and also achieved in large commercial structures via the Leadership in Energy & Environmental Design program or LEED. Some may recall that when Bill Gates built his multi-million dollar mansion on Lake Washington in Seattle, he had “remote control” of his home built into it. Now, years later, Gates’ original home automation is obsolete. The dream of home automation has been around for years, with numerous Silicon Valley conferences, and failed startups over the years, and needless to say, home automation went nowhere. But it is this concept of effortless home automation that has been the Holy Grail.

But this is also where the glowing promise of The Internet of Things (IoT) begins to morph into a giant “hairball.” The term “hairball” was former Sun Microsystems CEO, Scott McNealy‘s favorite term to describe a complicated mess. In hindsight, the early euphoric days of home automation were plagued by the lack of “convergence.” I use this term to describe the inability of available technology to meet the market opportunity. Without convergence, there can be no market opportunity beyond early adopter techno geeks. Today, the convergence problem has finally been eliminated. Moore’s Law and advances in data communication have swept away the convergence problem. But for many years the home automation market was stalled.

Also, as more Internet-connected devices emerged it became apparent that these devices and apps were a hacker’s paradise. The concept of IoT was being implemented in very naive and immature ways and lacking common industry standards on basic issues: the kinds of things that the IETF and IEEE are famous for. These vulnerabilities are only now very slowly being resolved, but still in a fragmented ad hoc manner. The central problem has not been addressed due to classic proprietary “not invented here” mindsets.

The problem that is currently the center of this hairball, and from all indications is not likely to be resolved anytime soon. It is the problem of multiple data communication protocols, many of them effectively proprietary, creating a huge incompatible Tower of Babbling Things. There is no meaningful industry and market wide consensus on how The Internet of Things should communicate with the rest of the Internet. Until this happens, there can be no fulfillment of the promise of The Internet of Things. I recently posted “Co-opetition: Open Standards Always Win,” which discusses the need for open standards in order for a market to scale up.

A recent ZDNet post explains that home automation currently requires that devices need to be able to connect with “multiple local- and wide-area connectivity options (ZigBee, Wi-Fi, Bluetooth, GSM/GPRS, RFID/NFC, GPS, Ethernet). Along with the ability to connect many different kinds of sensors, this allows devices to be configured for a range of vertical markets.” Huh? This is the problem in a nutshell. You do not need to be a data communication engineer to get the point. And this is not even close to a full discussion of the problem. There are also IoT vendors who believe that consumers should pay them for the ability to connect to their proprietary Cloud. So imagine paying a fee for every protocol or sensor we employ in our homes. That’s a non-starter.

The above laundry list of data communication protocols, does not include the Zigbee “smart meter” communications standards war. The Zigbee protocol has been around for years, and claims to be an open industry standard, but many do not agree. Zigbee still does not really work, and a new competing smart meter protocol has just entered the picture. The Bluetooth IEEE 802.15 standard now may be overtaken by a much more powerful 802.15 3a. Some are asking if 4G LTE, NFC or WiFi may eliminate Bluetooth altogether. A very cool new technology, energy harvesting, has begun to take off in the home automation market. The energy harvesting sensors (no batteries) can capture just enough kinetic, peizo or thermoelectric energy to transmit short data communication “telegrams” to an energy harvesting router or server. The EnOcean Alliance has been formed around a small German company spun off from Siemens, and has attracted many leading companies in building automation. But EnOcean itself has recently published an article in Electronic Design News, announcing that they have a created “middleware” (quote) “…to incorporate battery-less devices into networks based on several different communication standards such as Wi-Fi, GSM, Ethernet/IP, BACnet, LON, KNX or DALI.” (unquote). It is apparent that this space remains very confused, crowded and uncertain. A new Cambridge UK startup, Neul is proposing yet another new IoT approach using the radio spectrum known as “white space,” becoming available with the transition from analog to digital television. With this much contention on protocols, there will be nothing but market paralysis.

Is everyone following all of these acronyms and data comm protocols? There will be a short quiz at the end of this post. (smile)

The advent of IP version 6, strongly supported by Intel and Cisco Systems has created another area of confusion. The problem with IPv6 in the world of The IoT is “too much information” as we say. Cisco and Intel want to see IPv6 as the one global protocol for every Internet connected device. This is utterly incompatible with energy harvesting, as the tiny amount of harvested energy cannot transmit the very long IPv6 packets. Hence, EnOcean’s middleware, without which their market is essentially constrained.

The Brave New World of Internet privacy issues relating to this tidal wave of Big Data are not even considered here, and deserve a separate post on the subject. A recent NBC Technology post has explored many of these issues, while some have suggested we simply need to get over it. We have no privacy.

Stakeholders in The Internet of Things seem not to have learned the repeated lesson of open standards and co-opetition, and are concentrating on proprietary advantage which ensures that this market will not effectively scale anytime in the foreseeable future. Intertwined with the Tower of Babbling Things are the problems of Internet privacy and consumer concerns about wireless communication health & safety issues. Taken together, this market is not ready for prime time.

NOTE: My original post, originally published in January 2013, continues to be one of the most viewed on the site. Android and Apple have enjoyed an estimated 98% market share between the two, and many of my earlier projections regarding this market appear to have been borne out. However, the smartphone market has now matured to the point that it is at a strategic inflection point which has major implications for the future of this market and the major competitors. The rapid maturation of the smartphone market should have been foreseen: the rise of domestic Chinese competition combined with the predictable end of the Western consumer fascination with “the next smartphone”

NOTE: My original post, originally published in January 2013, continues to be one of the most viewed on the site. Android and Apple have enjoyed an estimated 98% market share between the two, and many of my earlier projections regarding this market appear to have been borne out. However, the smartphone market has now matured to the point that it is at a strategic inflection point which has major implications for the future of this market and the major competitors.

The Rapid Maturation of the Smartphone Market Should Have Been Foreseen

The signs of a dangerous strategic inflection point in the global smartphone market have been evident for some time: the rapid rise of domestic Chinese competition combined with the predictable end of the Western consumer fascination with “the next smartphone.” Five years ago, Samsung Electronics, the South Korean technology giant sat atop the Chinese market, selling nearly one of every five devices there. Today, Samsung is an also-ran, controlling less than 1% of the world’s largest smartphone market. Samsung has trimmed local staff and last month closed one of its two Chinese smartphone factories. Surely, Apple must have been aware of this and the growing number of much lower cost domestic Chinese competitors that were already hammering Samsung. Apple’s release of a lower cost iPhone, the XR, in Asia in October 2018 appears to have been a case of too little too late. Sales of the device have been disappointing in both Japan and China, and Apple has been relegated to offering “trade-ins” to camouflage slashing the price of the XR. Apple had ample warning over at least a five year period.

Meanwhile, I sensed a very different kind of maturation of the smartphone market in North America and Europe. In what I like to call the smartphone market “Star Wars” phenomenon, each new generation of smartphones was greeted with a hysteria that was only paralleled by the Star Wars craze. This simply could not continue indefinitely. Beginning in 2017 it was apparent the smartphone market as a whole was already shrinking, and there was significant anecdotal information in the media that smartphone hysteria was waning, if not publicly available hard data. I began having discussions about this with Tim Bajarin, one of the top Apple analysts. As Apple moved to launch the iPhone X and broke the $1000 price point barrier it encountered clear if perhaps not overwhelming evidence that the smartphone market was softening: more people chose not to upgrade their phones. I like to say that the last major feature consumers seemed to want/need was water resistance, as so many had already experienced the disastrous “toilet drop.” I view the Bluetooth earbud phenomenon as a distraction and perhaps a hint of the coming change. Samsung flirted with water resistance as early as the Samsung Galaxy S5, perhaps because water resistance had become a standard feature in the Japanese market. By 2018, water resistance was standardized, and the market began experimenting with “the next big thing” for phones, folding screens. WTF? It was clear to me that the smartphone market had run out of gas, and was undergoing rapid maturation, as phones were no longer fascinating and novel, but just simply commodity devices.

To my mind, and IMHO, this has been a case study in a classic “strategic inflection point” that was missed by both Samsung and Apple. Samsung might be forgiven for being the first to cross into the inflection point, while the media was still promoting “the next smartphone” hysteria, and not yet recognizing the sense of the market. Apple has no such excuse. The rapid maturation of the smartphone market should have been foreseen by Apple. Apple’s most disturbing move was the decision to increase pricing rather than delivering greater value, at exactly the wrong time. The crucial rhetorical question is what are the larger implications for Apple’s future business?

Smartphone vendors shipped a total of 355.6 million units worldwide during the third quarter of 2018 (Q3 2018), resulting in a 5.9% decline when compared to the 377.8 million units shipped in the third quarter of 2017. The drop marks the fourth consecutive quarter of year-over-year declines for the global smartphone market.

Quarter

2017Q1

2017Q2

2017Q3

2017Q4

2018Q1

2018Q2

2018Q3

Samsung

23,2%

22,9%

22,1%

18,9%

23,5%

21,0%

20,3%

Huawei

10,0%

11,0%

10,4%

10,7%

11,8%

15,9%

14,6%

Apple

14,7%

11,8%

12,4%

19,6%

15,7%

12,1%

13,2%

Xiaomi

4,3%

6,2%

7,5%

7,1%

8,4%

9,5%

9,5%

OPPO

7,5%

8,0%

8,1%

6,9%

7,4%

8,6%

8,4%

Others

40,2%

40,1%

39,6%

36,8%

33,2%

32,9%

33,9%

TOTAL

100,0%

100,0%

100,0%

100,0%

100,0%

100,0%

100,0%

2009 to 2012

In one of the most interesting high tech scenarios in years, the “smart mobile” OS (operating system) market is shaping up to be a classic Battle of the Titans. Key strategic issues, theories, speculation, and money, lots of it, are making this a great real-time strategy and marketing case study for management students of all ages (smile). So as Dell prepares to fade into the sunset, get yourself a drink of your choice, and some popcorn, sit back and watch it all unfold.

The best metaphor I can apply to this might be a “destruction derby” featuring at least two players, or perhaps a bizarre multidimensional Super Bowl or Rugby World Cup match, with four teams on one playing field with four goal posts at each cardinal point of the compass.. At the moment all four teams are tackling, passing, and running at each other in a confused pile. There are scrums, rucks and mauls in multiple locations. Two competitors, Google and Apple appear to be winning. The other two, Microsoft and Research in Motion, are pretty banged up, but still playing.

The two currently dominant competitors, Google Android with its acquisition of Motorola Mobility, and Apple IOS are rapidly consolidating and expanding their global market positions, via partnerships, vertical integration, and application development ecosystems. Microsoft has publicly committed to spending massively to make Windows 8 the third OS option, but a recent IDC mobile OS market forecast projects Microsoft with only a miniscule share in 2015. Something tells me that Steve Ballmer will go on a rampage if that happens, rather like the video of him screaming and dancing on stage in my post “Extrovert or Introvert, Authentic Presentations Take Practice,” November 30th. http://mayo615.com/2012/11/30/introvert-or-extrovert-authentic-presentations-take-practice/

The key question is whether Microsoft or RIM, will be able to establish a third mobile OS to a survivable market position. It is not at all clear that either can do so at this point. The market is also speculating that mobile hardware market leader Samsung, is possibly considering making its own play by creating its own mobile OS ecosystem. While this may seem far fetched, this kind of vertical integration seems to be making a resurgence as a strategic move, after having been discredited. Then there is the perennial Nokia, who has seemed to be on death’s door, but may be coming back. As a strategic partner for Microsoft, Nokia’s fate may have a huge bearing on Microsoft’s strategy to reinvent itself as the PC goes into atrial fibrillation. Will Amazon enter the fray with its own smart phone entrant, and if so, with whose OS? Will Research in Motion and the Blackberry be able to achieve a survivable market share, or is RIM already a walking zombie?

Finally, in a kind of death dance patent dispute reminiscent of the film, Gladiator, Nokia and RIM are now locked in new lawsuits and counter-lawsuits, as if to say, “If neither of us are going to survive, we might as well kill each other for the entertainment value.”

Here’s a more concise overview of the race to be the third mobile platform:

For Management students, this real time case study offers the opportunity to apply and ponder:

1. The time tested 1976 Boston Consulting Group (Bruce Henderson)“rule of three and four.” In a stable mature market there can be no more than three surviving competitors, the largest of which can have no more than four times the share of the smallest of the three. Here, the question is whether a third competitor can successfully emerge at all?

2.Barriers to market entry. Former Intel Marketing VP, Bill Davidow‘s book, Marketing High Technology, An Insider’s View, still considered the standard on the topic, suggested his own metric for a barrier to a new market entrant, or even a competitor just struggling to survive the market shakeout. The market entry barrier rule of thumb in dollars is three-quarters the most recent annual revenue of the market leader. In this case, that is a very big B number… Microsoft has the bucks, but is it just too late?

3. Vertical integration. Rumors of Samsung introducing its own mobile OS seem implausible, but hey Nvidia just announced its own gaming console to compete with Microsoft, Nintendo, and Sony.

4. Resources and capabilities. It is necessary to consider the respective resources and capabilities of each of the many direct players, and those playing in related markets that bear on the mobile OS market.

5. Related markets, new markets, peripherally involved competitors and products which all could play a role in the eventual outcome of this. The integrated Internet HDTV market is only one example. Featuring Apple, Microsoft, Google, and Samsung, and the HDTV manufacturers, it could influence things. What if Amazon were to vertically integrate and introduce its own smart phone?

This is the hairball of this Century so far. Are you all still with me, here?

How business schools are adapting to the changing world of work

Creativity, adaptability are now cornerstones of business education

Brandie Weikle · CBC News ·

Students chat in a hallway at Western University’s Ivey Business School in London, Ont. Business schools say they’ve adapted

their programming to fit a changing work world that prizes creative, agile workers who can adapt to rapid change. (Ivey Business School)

Forget about accounting class and marketing 101.

Canadian business school leaders say soft skills such as creativity and agility are now cornerstones of business education, as universities and colleges adapt to a world where many of the jobs graduates will hold don’t even exist today.

They say there’s still a role for those business basics, but they’re no longer enough to satisfy workplaces that prize employees who can adapt to swiftly changing industries, disruptive technology and the thorny issues facing humanity in the years to come.

“The goal of a university education is to teach people how to deal with uncertainty, how to be a critical thinker, how to be okay when things are changing,” said Darren Dahl, a senior associate dean at the University of British Columbia’s Sauder School of Business in Vancouver.

“The notion of going to work for the big corporation, and the jobs that we traditionally do, are evolving and changing,” said Dahl. That’s put a lot of pressure on business schools to change what and how they teach, he said.

To keep on top of what employers are looking for, the staff at the Ivey School of Business at the University of Western Ontario in London, Ont., recently completed 250 interviews with leaders in government, business and non-profits around the globe, said acting dean Mark Vandenbosch.

Mark Vandenbosch, acting dean of Ivey Business School, seen in this March 25, 2015, file photo, said today’s job market prizes soft skills. (Ivey Business School)

“Although people do need to have technical literacy that’s probably higher than before — the skills that are really demanded are the soft skills that will allow them to adapt,” said Vandenbosch.

‘Embracing creativity in a big way’

These include the ability to bring alternative viewpoints to a problem, he said, as well as things like creativity, grit, teamwork, communications effectiveness and decision-making skills.

At UBC, Dahl said the MBA program includes a required course in creativity. “That surprises some people,” he said. “Traditionally, you might think of a business school as beating out the creativity in students.”

The creativity class curriculum isn’t centered around business innovation, such as coming up with a new product. “It’s more base creativity,” he said.

Creativity is a muscle. How do we strengthen that muscle for you as a leader, whether you work in corporate or a non-profit or your own entrepreneurial venture?– Darren Dahl , associate dean, UBC’s Sauder School of Business

“Creativity is a muscle. If you stopped exercising it years ago — some people say you’re the most creative when you’re five or six years old and then it’s just downhill — how do we strengthen that muscle for you as a leader, whether you work in corporate or a non-profit or your own entrepreneurial venture?

“That’s a fundamental tool in the toolbox, and I think society has just woken up to that in the last five years,” said Dahl.

Joe Musicco, who teaches at Sheridan College’s Pilon School of Business in Toronto, said: “business is certainly embracing creativity in a big way.”

There are a number of factors contributing to the business world’s increasing interest in creativity, said Musicco.

“You could point to things like technology and AI [Artificial Intelligence]. You could point to things like the changing nature of work and being more of a thinker and a consultant, and expectations of people in general that [graduates] are going to be able to bring innovation and creative problem-solving skills to the table.”

Students have more diverse goals

What students want has changed, too.

“The younger generations today are very much interested in having an impact,” said Dahl.

“That could mean anything from having an impact by building their own business, to having a positive influence on society.”

In the past, most business school students would strive for the same jobs at large, branded international corporations, he said.

While some still do, others want to work for non-profits, and some want to be their own bosses, said Dahl.

Students are seen in class at Ivey Business School. (Ivey Business School)

Preparation for the entrepreneurial world

Dahl said there’s also been “a sea change in respect to the importance of entrepreneurial activity in the economy.”

To meet that need, course material is now taught differently, he said, moving away from “the classic lecturing on the stage” to methods that involve more action and applied learning.

Business school classes could be challenged to partner up with engineering students on a project, or to work with start-ups, for example.

At Ivey Business School, Vandenbosch said “a huge percentage of our graduates run their own businesses.”

The typical route they take, though, is to work for somebody else for a few years after graduation to get on-the-ground experience, then return to the school to take advantage of the entrepreneurial incubator it offers for alumni, he said.

“We provide a lot of support post graduation for those who want to come back at a later time to start a venture two, three or four years later.– Mark Vandenbosch, acting dean, Ivey Business School

“We provide a lot of support post-graduation for those who want to come back at a later time to start a venture two, three or four years later.”

One of the ways Ivey prepares graduates for a more entrepreneurial world is by throwing out the traditional undergraduate schedule where students make their own course selections then keep that schedule over a semester.

Instead, starting when they join Ivey in the third year, students show up at expected times each day, then programming is varied all year long, said Vandenbosch.

“Our focus is primarily on building experiences for students so they can build the capabilities to adapt to a future world, rather than, ‘Here is what you need to know about subject X.'”

Over five years ago now, March 11, 2013, I published this mayo615 blog post on the Alberta bitumen bubble, and the budgetary problems facing Alberta Premier Alison Redford, and the federal Finance Minister Jim Flaherty at that time, both of whom were surprisingly candid about the prospect for ongoing long-term budgetary problems for both the Alberta and Canadian national economies. Fast forward five years to today and the situation has essentially worsened dramatically. The current Alberta Premier Rachel Notley is facing another massive budget deficit, just as Alison Redford predicted years ago, and was forced to call a new election. My most glaring observation is that despite years of rhetoric and arm-waving, almost nothing has changed. Meanwhile, the Canadian economy is on the precipice of a predicted global economic downturn which could easily become a global financial contagion.

Bitumen prices are low because the province has ignored at least a decade of warnings.

Over five years ago now, March 11, 2013, I published this mayo615 blog post on the Alberta bitumen bubble, and the budgetary problems facing Alberta Premier Alison Redford, and the federal Finance Minister Jim Flaherty at that time, both of whom were surprisingly candid about the prospect for ongoing long-term budgetary problems for both the Alberta and Canadian national economies. Fast forward five years to today and the situation has essentially worsened dramatically. The current Alberta Premier Rachel Notley is facing another massive budget deficit, just as Alison Redford predicted years ago, and was forced to call a new election. My most glaring observation is that despite years of rhetoric and arm-waving, almost nothing has changed. Meanwhile, the Canadian economy is on the precipice of a predicted global economic downturn which could easily become a global financial contagion.

Today, the Tyee has published an excellent article detailing how and why this trainwreck of Alberta fossil fuel-based economic policy developed, and has persisted for so long without changing course.

In 2007, an Alberta government warned that bitumen prices could eventually fall so low that the government’s royalty revenues — critical for its budget — would be at risk. Photo via the Government of Alberta.

The Alberta government has known for more than a decade that its oilsands policies were setting the stage for today’s price crisis.

Which makes it hard to take the current government seriously when it tries to blame everyone from environmentalists to other provinces for what is a self-inflicted economic problem.

In 2007, a government report warned that prices for oilsands bitumen could eventually fall so low that the government’s royalty revenues — critical for its budget — would be at risk.

The province should encourage companies to add value to the bitumen by upgrading and refining it into gasoline or diesel to avoid the coming price plunge, the report said.

Instead, the government has kept royalties — the amount the public gets for the resource — low and encouraged rapid oilsands development, producing a market glut.

With North American pipelines largely full, U.S. oil production surging and U.S. refineries working at full capacity, Alberta has wounded itself with bad policy choices, say experts.

The Alberta government and oil industry is in crisis mode because the gap between the price paid for Western Canadian Select — a blend of heavy oil and diluent — and benchmark West Texas Intermediate oils has widened to $40 US a barrel.

Some energy companies have called on the government to impose production cuts to increase prices.

The business case for slowing bitumen production was made by the great Fort McMurray fire of 2015.

The fire resulted in a loss of 1.5 million barrels of heavy oil production over several months. As a result, the price of Western Canadian Select rose from $26.93 to $42.52 per barrel.

Premier Rachel Notley has appointed a three-member commission to consider possible production cuts, something Texas regulators imposed on their oil industry in the 1930s to help it recover from falling prices due to overproduction.

Oilsands crude typically sells at a $15 to $25 discount to light oil such as West Texas Intermediate. It costs more to move through pipelines, as it has to be diluted with a high-cost, gasoline-like product known as condensate. According to a recent government report, it can cost oilsands producers $14 to dilute and move one barrel of bitumen and condensate through a pipeline.

And transforming the sulfur-rich heavy oil into other products is more expensive because its poor quality requires a complex refinery, such as those clustered in the U.S. Midwest and Gulf Coast.

But the growing discount has cost Alberta’s provincial treasury dearly because royalties are based on oil prices.

Earlier this year, an RBC report pegged the loss at $500 million a year, while a more recent study estimates the losses could be as high as $4 billion annually.

While a few oilsands companies such as heavily indebted Cenovus say they are losing money due to the heavy oil discount, others are making record profits and say no market intervention or change is necessary.

The difference is those companies heeded the decade-old warnings and invested in upgrades and refineries to allow them to sell higher-value products.

Canada exports about 3.3 million barrels of oil a day. About half of that is diluted bitumen or heavy oil.

And the current dramatic price discount has divided oilsands producers into winners and losers.

The winners invested in upgrades and refineries, while the losers are producing more bitumen than their refinery capacity can handle or the market needs.

During Alberta’s so-called bitumen crisis, the three top oilsands producers — Suncor, Husky, and Imperial Oil — are posting record profits.

All three firms have succeeded this year because they own upgraders and refineries in Canada or the U.S. Midwest that can process the cheap bitumen or heavy oil into higher value petroleum products.

Imperial Oil, for example, boosted production at its Kearl Mine to 244,000 barrels in the most recent quarter but refined and added value to that product.

As a result, its net income for the quarter doubled to $749 million.

CEO Rich Kruger said that the collapse in bitumen prices was not a concern.

“Looking ahead, in the current challenging upstream price environment, we are uniquely positioned to benefit from widening light crude differentials,” he stated in a press release.

Suncor also reported that most of its 600,000-barrel-a-day production is not subject to the price differential because it upgrades the junk resource into synthetic crude or refines heavy oil into gasoline.

In its most recent business report, Husky reported a 48-per-cent increase in profits as cheap bitumen has fed its refineries and asphalt-making facilities.

The Alberta government knew this was coming.

A technical paper on bitumen pricing for Alberta Energy’s 2007 royalty review warned the province about the perils of increasing production without increasing value-added production.

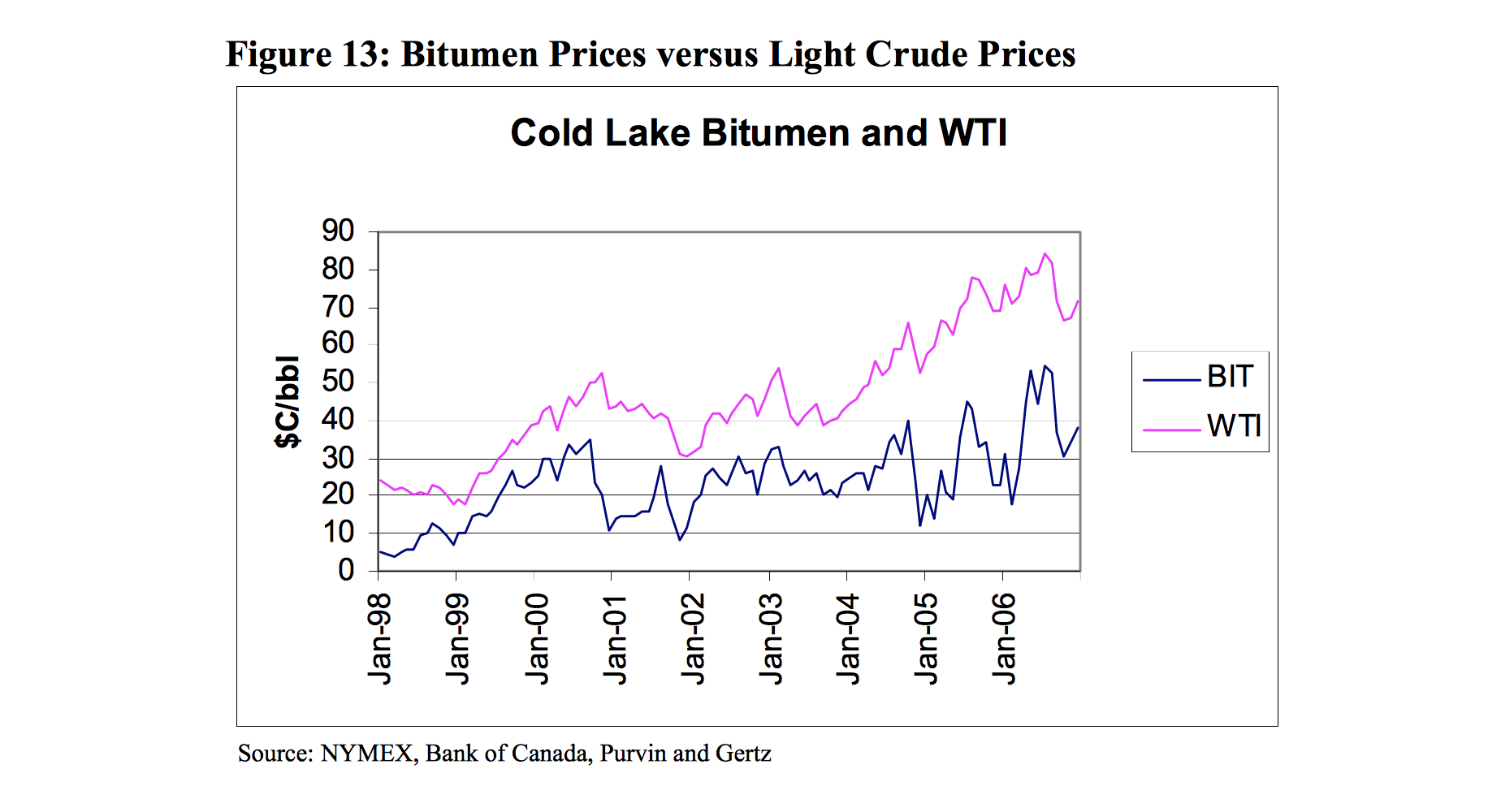

“Bitumen prices, when compared to light crude oil prices, are typified by large dramatic price drops and recoveries,” it noted. Between 1998 and 2005, “bitumen prices were 63 percent more volatile than West Texas Intermediate prices,” it said.

Two things are apparent from the bitumen (BIT) and West Texas Intermediate (WTI) price series shown above. First, bitumen prices, when compared to light crude oil prices, are typified by large dramatic price drops and recoveries. In fact, over the period shown, bitumen prices were 63 percent more volatile than WTI prices. Image from 2007 Alberta government report.

The analysis added that “for bitumen to attract a good price, it needs refineries with sufficient heavy-oil conversion capacity.”

The province’s push to develop the oilsands quickly increased the risk, the report said. “Price volatility for bitumen, especially the extremely low prices that have been witnessed several times over the past several years, is the most obvious risk.”

And the report noted that increasing bitumen production posed “a revenue risk for the resource owner” — the people of Alberta. When the differential widens, Alberta makes less money on its already low royalty bitumen rates.

Companies can compensate for the price risk by buying or investing in U.S. refineries; securing long-term pipeline contracts; investing in storage or using contracts to protect them from price swings.

Many oilsands producers, including Suncor, Imperial, and Husky, have lessened their vulnerability to bitumen’s volatility by doing all of these things.

But the provincial government is more exposed to price swings, the report said.

“For the province, the variety of risk mitigation strategies that can be pursued by industry is generally not available. Therefore Alberta is absorbing a higher share of price risk, particularly where royalty is based on bitumen values.”

Van Meurs noted that upgrading considerably enhances the value of bitumen and would generate more revenue for the province.

But that did not appear to be the policy the government was pursuing, warned Van Meurs in his report to the government.

Low royalties “raise the issue whether it is in the interest of Alberta to continue to stimulate through the fiscal system such very high-cost production ventures,” wrote Van Meurs, a chief of petroleum developments for the Canadian government in the 1970s.

Charging higher royalties would not only slow down production and avoid cost overruns in the oilsands but also encourage “upgrading projects with higher value-added opportunities,” he wrote.

But Alberta succumbed to sustained oil patch lobbying in 2007 and ignored Van Meurs’ advice.

As a result oilsands royalties remained low and there was little incentive for companies to add value or build more upgraders and refineries.

In 2009 the province’s energy regulator said in an annual report on supply and demand outlooks that low bitumen prices were a direct consequence of overproduction.

Planned additions for upgrading and refining would resolve the problem in the future.

But after the 2008 financial crisis, planned upgrades in Alberta did not materialize.

With no provincial policy encouraging value-added processing, the industry took a strip-it-and-ship-it approach on bitumen and depended solely on pipelines to deal with overproduction.

Robyn Allan, an independent B.C. economist and former CEO of the Insurance Corporation of British Columbia, says the 2009 report by the energy regulator clearly shows the Alberta government knew the risks of overproduction.

“It won’t matter how many pipelines are built if oil producers continue to increase the amount of low-quality product they pump from the oil sands. Pipelines do nothing to improve quality and with new regulations on sulfur content, the world is telling us the downward pressure on heavy oil prices will only get worse,” said Allan.

In 2017, only 43 percent of the bitumen produced was actually upgraded in Canada while 57 percent was shipped raw to U.S. refineries.*

As bitumen prices plunged this year, U.S. refinery margins jumped to record levels.

According to a Nov. 6 article in the Wall Street Journal, Phillips 66, a major buyer of cheap Canadian bitumen, ran its refineries at 108 percent of capacity and was “earning an average $23.61 a barrel processed there.” Profits jumped to $1.5 billion, an increase of 81 percent over last year.

“U.S. refining has really gone from being a dog to being a fairly attractive business model,” one consultant told the Wall Street Journal. “I don’t think that’s going to change any time soon.”

Another beneficiary of Alberta’s no-value-added policy has been the billionaire Koch brothers.

They own the Pine Bend refinery in Minnesota, which turns more than 340,000 barrels of Canada’s crude into value-added products every day.

A widening of the price discount of heavy oil by just $15 adds an additional $2 billion in windfall profits a year for Koch Industries, one of the most powerful companies in North America.

The risks of Alberta’s policy of shipping raw bitumen to U.S. refineries was outlined again during the province’s 2015 royalty review, which like the 2007 report, resulted in little change due to successful industry lobbying.

In 2015, Barry Rogers of Edmonton-based Rogers Oil and Gas Consulting warned the government that low royalties for bitumen simply encouraged the industry to export the heavy oil to U.S. refineries with no value added in Canada.

“By not charging a competitive fiscal share Alberta is, in fact, subsidizing the industry. This gets government directly into the business of business and removes the benefits of market-priced signals — leading to reduced innovation, higher costs, reduced competitiveness, a transfer of economic rent from resource owners to industry and reduced economic diversification.”

Rogers added that the current policy might benefit a few powerful companies but was “a disaster for the overall industry, and, therefore, a disaster for Alberta — both for current and future generations.”

I was very interested yesterday to read the article in the Globe & Mail by University of Toronto Professor Richard Florida, and Ian Hathaway, Research Director for the Center for American Entrepreneurship, and Senior Fellow at the Brookings Institute. The article by Florida and Hathaway draws the same conclusions as my research, providing even more precise data to support their disturbing conclusions. It is not hard to find many additional articles on these issues. Ironically, also yesterday, a LinkedIn connection shared a post by Sciences, Innovation, and Economic Development Canada with a very upbeat, positive assessment of venture capital for startups in Canada. This is the essence of the problem. Since I came to Canada years ago now, I have seen a pollyannaish state of denial about the true situation for entrepreneurship, immigration policy, and the lack of “smart” venture capital for Canadian startups. No amount of counter-evidence has changed this mistaken rosy outlook. Without a recognition of these problems, nothing will change.

Canadian Venture Investment Is In Decline

Canada’s investment in R & D Has Been Anemic For Decades Compared to OECD Nations

U.S. Tech Giants Are Exploiting Canada’s Talent Base At The Expense of Canadian Startups

My long-time business partner and I, one of us in Canada and the other in Silicon Valley, last year launched a business targeted at bringing immigrant entrepreneurs to Canada, Vendange Partners. http://www.vendangepartners.com. We spent months analyzing and investigating the Canadian entrepreneurial ecosystem, particularly Vancouver and Toronto, Canadian immigration policy, and the Canadian venture capital industry. What we found was very concerning. Last December, I wrote a blog post here detailing our findings (read more below) that Canada was nowhere close to being the next Silicon Valley. With regard to venture capital, we found that there was a lack of adequate risk capital, which could be traced to deeply rooted conservative values in the Canadian financial industry. Immigration policy was a mixed bag, with a “startup” visa program that had become a magnet for immigration scams. Despite these disadvantages, we decided to press ahead, and are making progress.