From The Globe and Mail:

Via The Globe and Mail’s Android app

From The Globe and Mail:

Via The Globe and Mail’s Android app

The truth is that for all of the tough talk from Li Xinping about stopping the massive outflows of capital from China, some of it probably dark money obtained from dubious enterprises and kickbacks, nothing has changed in China or in the Western cities eager to share in the wealth. Rich, Young “Fuerdai” Chinese Are Buying Overseas Properties on Their Smartphones. Millennials acquire real estate in other countries as hedge against a weakening currency, homes for their own children when they study abroad

The truth is that for all of the tough talk from Li Xinping about stopping the massive outflows of capital from China, some of it probably dark money obtained from dubious enterprises and kickbacks, nothing has changed in China or in the Western cities eager to share in the wealth.

BEIJING— Zheng Xiaohei, a marketer from Urumqi in western China, made his first overseas property investment without so much as a visit.

Mr. Zheng, 29 years old, in March purchased a studio apartment in Thailand for about 650,000 yuan ($94,255) using his smartphone and an app called Uoolu that connects users to overseas property listings.

“Investing in overseas real estate was mainly due to my good impression of Thailand,” Mr. Zheng said.

Founded two years ago, Beijing-based Uoolu is focused on tapping a specific group of home buyers: Chinese millennials looking for foreign properties.

About 70% of Chinese millennials, those born between 1981 and 1998, own a home, the highest share of respondents from nine countries and regions who were surveyed in a recent HSBC study. Chinese parents often register home purchases under their child’s name to prepare the child for marriage and raising a family, which likely boosts the percentage.

Still, a growing sliver of Chinese millennials are looking to buy property abroad. Kevin Lee, chief operating officer of Beijing-based consulting firm Youthology, put the percentage in the low single digits but said it would continue to increase.

The lure? A millennial’s desire to hedge against yuan depreciation and find affordable homes in cities with cleaner air for their children to live in when they study abroad. In the past year, home prices have soared to more than 30 times household income in major Chinese cities.

Uoolu said about 80% of its monthly active users are between the ages of 20 and 39, and that 20,000 customers have bought or are in the process of purchasing overseas property. A similar real-estate platform, Juwai.com, estimates that roughly 30% to 40% of its buyers are millennials.

Cherubic Ventures, a venture-capital firm with offices in Beijing and San Francisco, invested an undisclosed sum in Uoolu. One selling point, said the firm’s founder, Matt Cheng, was Uoolu’s target of reaching young Chinese buyers who are tech savvy and interested in cross-border investments, “but don’t know where to begin.”

Overseas investing isn’t easy at a time when the Chinese government is clamping down on capital flight amid concerns about a weakening currency. Chinese citizens aren’t allowed to transfer more than $50,000 a year out of the country or use those funds to buy overseas property.

However, this increased government scrutiny is “slowing but not cutting off” the surge of investment in U.S. property, said Arthur Margon, partner at Rosen Consulting Group.

“The more the government limits people, the more they want to invest overseas,” said Wang Hao, Uoolu’s 33-year-old chief operating officer.

People often skirt the foreign-exchange rules by, for example, pooling money among family members and friends and separately sending it into overseas bank accounts. Also, Chinese citizens who have studied or worked abroad for a few years might already have bank accounts in other countries and those overseas funds are beyond the Chinese government’s control.

Alan Wang, a 19-year-old college student in Toronto who comes from Shenzhen, said he opened a bank account in Canada for education expenses. Now it is useful for buying property, too. He and his family are thinking about purchasing a home on a budget of about 1 million Canadian dollars (US$730,600) this summer. To do so, he will have relatives send money to his bank account, he said.

Uoolu helps buyers open bank accounts in other countries and apply for mortgages there. Users pay a deposit to reserve the right to purchase a home. The money is sent directly from a buyer’s bank account to the overseas developer—Uoolu says it doesn’t handle the cross-border transaction within the mobile app.

Chris Daish, a real-estate agent at Triplemint in New York, said one of his Chinese clients, an accountant in her mid-20s who works in New York, earlier this year pooled $110,000 from five family members to help buy her a condo in the city.

“It’s a really arduous task even to get a couple hundred grand out,” said Mr. Daish, who emphasized that he doesn’t help clients with money transfers.

A 28-year-old who works in finance in Beijing in February bought two apartments in Bangkok for a total of 5 million yuan ($725,000), one for a vacation home and the other for rental income. She declined to disclose her name out of fear of government retaliation for violating capital controls.

As for some of her friends, she said, “They wish to buy but dare not.”

Source: Rich, Young Chinese Are Buying Overseas Properties on Their Smartphones – WSJ

Despite all of the revelations of the sources and methods of the Vancouver housing bubble over the last two years, the situation remains largely unresolved. Ditto in Toronto. The foreign buyers’ tax has had only a limited effect and has problems. Fueled by dark foreign money housed in anonymous offshore shell companies like those disclosed in the Panama Papers, the money is managed by local financial manipulators at the behest of unidentifiable persons overseas. The foreign buyers continue to enjoy the weakest enforcement jurisdiction in Canada

Despite all of the revelations of the sources and methods of the Vancouver housing bubble over the last two years, the situation remains largely unresolved. Ditto in Toronto. The foreign buyers’ tax has had only a limited effect and has problems. Fueled by dark foreign money housed in anonymous offshore shell companies like those disclosed in the Panama Papers, the money is managed by local financial manipulators at the behest of unidentifiable persons overseas. The foreign buyers continue to enjoy the weakest enforcement jurisdiction in Canada

Loopholes in Canadian law are allowing a “corrupt elite” to use the housing market for money-laundering, says a new report from Transparency International (TI).

The report found 10 problem areas with the laws related to real estate transactions in Canada, Australia, the U.K. and the U.S. — four countries it identifies as being hot-spots for real estate-related money laundering.

“Canada’s legal framework has severe deficiencies under four of the 10 identified areas,” TI stated in the report. “In the other six, there are either significant loopholes that increase risks of money laundering through the real estate sector or severe problems in implementation and enforcement of the law.”

This Grey’s Point “tear down” property shown here, recently sold for over $9 Million, more than $1 Million over the asking price of $7.8 Million. There were 11 offers, all cash, and no offer included any contingencies.

One glaring problem is a lack of rules requiring that the actual owner (or “beneficial owner”) of a property be identified. In Canada “there are no requirements for any person involved in real estate closings to identify the beneficial owner,” the TI report stated.

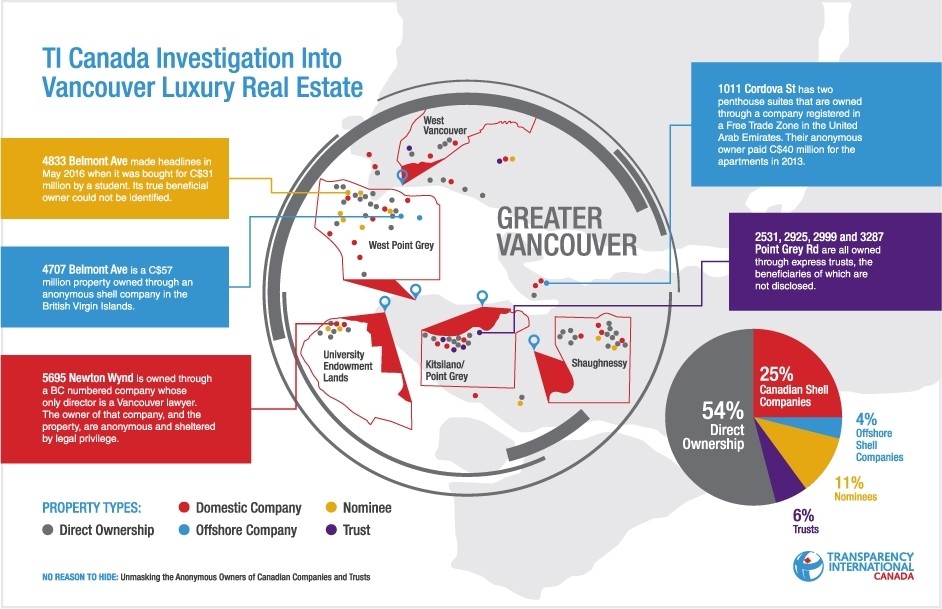

In a study published last December, TI found that the government does not know who owns 46 of the 100 most expensive homes in Vancouver.

The report found that 29 of the homes were owned by shell companies, either Canadian or offshore.

“Offshore companies pose a serious risk … because they are able to purchase property without needing to disclose any information relating to who ultimately owns and controls them to any government authority,” TI said in the report published Wednesday.

The report noted that money-laundering through real estate is growing increasingly popular.

“Large amounts of money can be legitimized at once, maintaining or increasing its value. Investments in real estate are seen as an alternative for those who fear having offshore accounts frozen.”

This chart from Transparency International shows what is known, and not known, about the ownership of Vancouver’s 100 most expensive homes.

Because of over-reliance on banks to spot money-laundering activities, and because banks aren’t involved in cash purchases of homes, money-laundering is going unnoticed, the report said.

And like in the other countries studied, in Canada “there are no data on prosecutions against real estate agents or other professionals for facilitating money laundering.”

Canada has “the best model” for enforcement of money-laundering laws among the four countries studied, the report said, but Canada’s financial intelligence agency, FINTRAC, investigates relatively few real estate transactions.

The report lays out a series of recommendations for governments, including requiring all professionals involved in a real estate transaction to disclose the actual buyer. This should also be required of companies that are buying real estate, the report said.

It also suggested that professionals involved in real estate transactions, such as lawyers and realtors, be registered with a country’s anti-money laundering authorities before they are allowed to practice.

“Governments must close the loopholes that allow corrupt politicians, civil servants and business executives to be able to hide stolen wealth through the purchase of expensive houses in London, New York, Sydney and Vancouver,” TI chair José Ugaz said in a statement.

“The failure to deliver on their anti-corruption commitments feeds poverty and inequality while the corrupt enjoy lives of luxury.”

British Columbia has no limits on political donations, leading critics to say the provincial government has become a lucrative business dominated by special interests. As the premier of British Columbia, Christy Clark is on the public payroll, pulling down a salary of 195,000 Canadian dollars in taxpayer money. But if that were not enough, she also gets an annual stipend of up to 50,000 Canadian dollars — nearly $40,000 — from her party, financed by political contributions. Personal enrichment from the handouts of wealthy donors, some of whom have paid tens of thousands of dollars to meet with her at private party fund-raisers? No conflict of interest here, according to a pair of rulings last year by the province’s conflict-of-interest commissioner — whose son works for Ms. Clark.

British Columbia has no limits on political donations, leading critics to say the provincial government has become a lucrative business dominated by special interests.

Source: British Columbia: The ‘Wild West’ of Canadian Political Cash – NYTimes.com

VANCOUVER, British Columbia — As the premier of British Columbia, Christy Clark is on the public payroll, pulling down a salary of 195,000 Canadian dollars in taxpayer money. But if that were not enough, she also gets an annual stipend of up to 50,000 Canadian dollars — nearly $40,000 — from her party, financed by political contributions.

Personal enrichment from the handouts of wealthy donors, some of whom have paid tens of thousands of dollars to meet with her at private party fund-raisers? No conflict of interest here, according to a pair of rulings last year by the province’s conflict-of-interest commissioner — whose son works for Ms. Clark.

“B.C. is the wild west,” said Duff Conacher, a founder of Democracy Watch, a Canadian civic organization that has petitioned the Supreme Court of British Columbia to void the commissioner’s decision. The group argues that there is a “reasonable apprehension of bias” because the commissioner’s son is a deputy minister in Ms. Clark’s cabinet. The court heard arguments in the case on Friday.

Ethics in politics is a hot topic right now in Ottawa. Prime Minister Justin Trudeau has faced criticism for attending exclusive fund-raisers, and other Canadian provinces are tightening the reins on political contributions. Against that backdrop, the case in British Columbia stands out for the unabashedly cozy relationship between private interests and government officials in the province, a political state of affairs that will be tested at the ballot box in May.

Unlike many other provinces in Canada, British Columbia has no limits on political donations. Wealthy individuals, corporations, unions and even foreigners are allowed to donate large amounts to political parties there. Critics of the premier and her party, the conservative British Columbia Liberal Party, say the provincial government has been transformed into a lucrative business, dominated by special interests that trade donations for political favors, undermining Canada’s reputation for functional, consensus-driven democracy.

“What it says to people is money talks and votes don’t,” said Dermod Travis, the executive director of IntegrityBC, a nonpartisan political watchdog group based in Victoria, the provincial capital. “When anyone anywhere in the world can donate as much as they want to the system, you have an even bigger threat to the system.”

Much of what is considered business as usual in British Columbia is illegal elsewhere in Canada. The federal government bars unions, corporations and foreigners from donating to candidates for federal office, and donations by individual citizens are limited to 1,525 Canadian dollars, about $1,150, a year. Those limits were imposed after a fund-raising scandal in the 1990s.

Provincial ethics rules are a patchwork of restrictions and loopholes. Corporate and union donations are banned in Nova Scotia, Manitoba, Alberta and, since Jan. 1, in Ontario. Ontario provincial officials, their staff members and party leaders are also barred from attending fund-raisers. Quebec goes even further, limiting party donations to 100 Canadian dollars, roughly $76 a year, and only by individual citizens.

British Columbia is not the only province to refuse to impose such tight limits, but democracy advocates say the large amounts of money flowing there are a particular cause for concern.

Critics say that big donors to Ms. Clark’s party often appear to have benefited financially from their political generosity. These include banks, Chinese real estate developers, and companies like Imperial Metals, the owner of a mine tailings pond that spilled billions of gallons of toxic debris in 2014, and was then permitted to operate an even larger mine. Imperial Metals did not respond to a request for comment.

On Thursday, Ms. Clark’s government approved the Kinder Morgan Trans Mountain oil pipeline project, after opposing the proposal at hearings last January. Political donation records show that Kinder Morgan and other oil industry supporters of the project had donated more than 718,000 Canadian dollars, about $546,000, to the BC Liberal party through March 2016.

Some pooled donations have ended up in the pockets of the premier, following a longstanding practice by her political party. Ms. Clark has received more than 277,000 Canadian dollars, or $210,000, from the BC Liberal Party since 2011, according to Canadian news media reports. No other party in British Columbia pays its leader a stipend, and only one other Canadian premier, in Saskatchewan, receives such funds; the practice has largely vanished elsewhere as the provinces have tightened their political finance rules.

Ms. Clark’s office declined to answer specific questions about her conduct and her relationship with the conflict-of-interest commissioner and his son. Instead, British Columbia’s minister of justice, Suzanne Anton, who is also its attorney general, sent a statement saying that the province’s standards “should give the public confidence in the electoral system.”

In an email, the B.C. Liberal Party said its leader’s stipend was a longstanding tradition that previous conflict-of-interest commissioners had found acceptable.

Last April, Ms. Clark’s stipend was challenged by David Eby, a member of the provincial legislative assembly from the B.C. New Democratic Party. He filed complaints with the conflict-of-interest commissioner about the stipend and about Ms. Clark’s attendance at fund-raisers where donors paid thousands of dollars to meet with her privately.

“In practice, it means that if you’re part of a coterie of high-net-worth donors, your private interests get priority over what’s best for the province,” Mr. Eby said.

In nine years as British Columbia’s conflict of interest commissioner, Paul Fraser said he has never found any government official to be in violation of the province’s Conflict of Interest Act. Mr. Fraser has donated to Ms. Clark’s political party, and so has his son, John Paul Fraser, who worked on Ms. Clark’s election campaign and now serves in her cabinet as the deputy minister for government communications and public engagement.

The elder Mr. Fraser ruled in May that his son’s boss did not violate the act by accepting tens of thousands of dollars from her party while attending exclusive party fund-raisers, despite the law prohibiting actions by officials that may create even the “reasonable perception” that they might be affected by private interests.

Democracy Watch asked the provincial Supreme Court in October to overturn the ruling, arguing that the commissioner should have recused himself, as he did in a 2012 case against Ms. Clark.

In a telephone interview, Mr. Fraser rejected accusations of bias over his son’s job. “The issue, I guess, is, should people’s children and their career aspirations trump other considerations,” he said. He added that his 2012 recusal was a special case, because his son had been in business with the premier’s ex-husband.

Mr. Fraser’s lawyers have tried to get the case dismissed by arguing that the commissioner’s opinions are immune to judicial review.

How many shell companies exist in Canada? How many legal trusts? Who are the beneficial owners protected by such unnecessary veils of secrecy? No one knows because in most cases there is no legal requirement to disclose actual ownership even to regulators. In fact, more information is required to get a library card than to set up a company in most jurisdictions in Canada. What we do know is that Canada ranks near the bottom among our OECD partners in terms of corporate disclosure requirements to fight money laundering and tax evasion. A recent report from Transparency International detailed the dismal situation and why our country has become a haven for dubious offshore property speculation.

How many shell companies exist in Canada? How many legal trusts? Who are the beneficial owners protected by such unnecessary veils of secrecy? No one knows because in most cases there is no legal requirement to disclose actual ownership even to regulators. In fact, more information is required to get a library card than to set up a company in most jurisdictions in Canada.

What we do know is that Canada ranks near the bottom among our OECD partners in terms of corporate disclosure requirements to fight money laundering and tax evasion. A recent report from Transparency International detailed the dismal situation and why our country has become a haven for dubious offshore property speculation.

“The Canadian government must take immediate steps to require all companies and trusts in the country to identify their beneficial owners to ensure Canada does not become a haven for corrupt capital,” warns Transparency International Canada executive director Alesia Nahirny.

Canada is one of the few developed countries that does not require the identities of company directors to be verified or any information on shareholders. In most provinces, it is legal to use “nominee” directors or shareholders without disclosing that they are acting on someone else’s behalf.

A nominee is essentially a sock puppet — the proverbial student or homemaker often listed as the title owner of some of Canada’s most expensive homes. Why would someone list a multi-million dollar property in someone else’s name? Some plausible reasons include to avoid taxes or to launder money. This practice remains completely and inexplicably legal in most parts of our painfully polite country.

Lawyers can also act as nominee directors, offering their clients an additional level of secrecy under solicitor-client privilege unavailable in most other countries. A ruling from the Supreme Court of Canada in 2015 exempted lawyers and their firms from important parts of the Proceeds of Crime and Terrorist Financing Act, further widening the yawning loopholes in our laws meant to fight money laundering. According to an international oversight body, the Financial Action Task Force of which Canada is a member, “the legal profession in Canada is especially vulnerable to misuse.”

Toronto lawyer Simon Rosenfeld was secretly taped in 2002 during a meeting in a Miami bar with an undercover RCMP officer, who was posing as a member of a Columbian drug cartel needing money-laundering services. According to the officer’s testimony, after exchanging a token dollar to cement solicitor-client secrecy, Rosenfeld bragged that moving illegal funds through Canada was “20 times” easier than the U.S., where arrest and convictions are much more likely. He described the Canadian enforcement regime as “la la land” and said that five other lawyers in Vancouver laundered $200,000 per month through trust accounts for a seven per cent commission.

The transcript of this conversation did not endear Rosenfeld to the jury during his prosecution and he was sentenced to three years in jail. He appealed the conviction and the higher court judge increased his sentence to five years. This rare successful enforcement provides some fleeting schadenfreude, but Rosenfeld’s seasoned and sad assessment of “la la land” continues to ring true.

Legal black boxes

Millions of legal trusts are estimated to exist in Canada, but there is no way of knowing since there is no requirement for them to be registered or file any record of their existence — again an outlier among other countries. They are supposed to file information on assets and trustees with the Canada Revenue Agency but only a small fraction actually do.

A trust is the consummate legal black box. Considered a mere private contract under Canadian law, trusts do not need to keep records on beneficial owners, let alone file such documents with the federal government. Trustees can conduct transactions without disclosing their role as go-betweens, making it difficult or impossible for financial institutions to comply with money laundering regulations. To our international embarrassment, the Financial Action Task Force found in 2016 that Canada was less than fully compliant in 29 out of 40 anti-money laundering measures and “non-compliant” regarding transparency and beneficial ownership of such legal arrangements.

Real estate in Vancouver and Toronto is where the rubber really hits the road on these national regulatory failings. Transparency International looked at the title documents for the 100 most expensive homes in the Lower Mainland and unsurprisingly found a sampling of all these methods to conceal the beneficial owners. Twenty-nine properties were held by Canadian or offshore shell companies, 11 were owned by nominees with no obvious source of income, six more were held by trusts. In total, 49 of these luxury estates collectively worth more than $1 billion had opaque ownership.

Canada’s lax legal oversight coupled with a decades-long public policy effort to incentivize wealthy citizenship has turned Vancouver into a global hedge city. Like London, New York, and San Francisco, Vancouver’s luxury properties have become a favored place to stash cash for the world’s wealthiest.

According to professor David Ley at the University of British Columbia, Canada effectively sold Canadian citizenships to rich offshore investors through the now-cancelled Business Immigration Program. Ley described the scheme during a lecture last September, detailing how up to 200,000 of the world’s wealthiest may have arrived in the Lower Mainland as a result of these public policy efforts, inflating property values and contributing to our current housing woes.

According to Ley, Canada’s BIP was heavily oversubscribed because Canada was selling citizenships for far below the international market rate compared to other countries with similar citizenship-for-sale incentive programs. In the U.S., candidates had to invest $1,000,000 and employ up to 10 Americans before being granted citizenship. In Canada, investors only had to loan provincial governments $800,000 to be paid back in full after five years. This come-and-get-it attitude towards passports and global capital seems sadly similar to other national assets such as natural resources, but I digress.

Besides ballooning our housing prices, was there a net economic benefit to this citizenship fire sale? According to Ley, the federal immigration database showed that “of all immigration streams to Canada, the Business Immigration Program led to the lowest declared incomes, lower even than refugees.” This was in part because wealthy offshore investors are so skillful at avoiding taxation coupled with a shocking lack of enforcement from the CRA.

Defending against dubious lucre

What can Canada do to clean up this mess and avoid becoming an even more desirable destination for dubious global lucre? A low-cost first step would be to require all Canadian companies and trusts to declare beneficial owners and publish this information on a public searchable registry. The United Kingdom brought in such a system in 2016 to improve in law enforcement and tax collection, which will more than cover the cost of implementation.

Transparency International has several other practical suggestions that are also supported by the banking sector and law enforcement:

Besides money launderers, tax evaders and criminals, who could possibly oppose these sensible and long overdue reforms? Is the Trudeau government going to act quickly to plug these gapping holes and bring our country in line with the global fight against illicit capital? The recent cash-for-access events with wealthy offshore investors provide a telling opportunity to see on whose behalf Trudeau is acting. The whole country is watching. ![]()

Reading this article today, I am dumbfounded that Anbang managed to get this far in the purchase of B.C. commercial real-estate without red flags going up. This mysterious Chinese company, Anbang Insurance Group has attracted the attention of The New York Times, The Wall Street Journal, Forbes, Fortune Magazine, and government authorities in the United States and other countries. A months-long investigation by the New York Times revealed an extremely opaque structure, empty offices, obscure shareholders, and extensive political connections to the Chinese elite. Anbang has all the earmarks of Chinese money laundering, corruption at the highest levels, and mysterious shell companies. It is a cautionary tale for Canadian authorities fretting over foreign real-estate buyers and skyrocketing real-estate prices.

Reading this article today, I am dumbfounded that Anbang managed to get this far in the proposed purchase of B.C. commercial real-estate without red flags going up. This mysterious Chinese company, Anbang Insurance Group has attracted the attention of The New York Times, The Wall Street Journal, Forbes, Fortune Magazine, and government authorities in the United States and other countries. A months-long investigation by the New York Times revealed an extremely opaque structure, empty offices, obscure shareholders, and extensive political connections to the Chinese elite. Anbang has all the earmarks of Chinese money laundering, corruption at the highest levels, and mysterious shell companies. It is a cautionary tale for Canadian authorities fretting over foreign real-estate buyers and skyrocketing real-estate prices.

The dingy fourth floor of this building in Beijing houses two companies that control assets of Anbang Insurance Group worth more than $15 billion.

The Anbang Insurance takeover is currently under scrutiny by the federal government’s Investment Review Division because it exceeds the $600-million threshold and it will ultimately be up to Innovation Minister to make a decision.

Source: Chinese company Anbang buys stake in B.C.-based retirement home chain – The Globe and Mail

A massive Chinese insurance company with a murky ownership structure is buying a majority stake in one of British Columbia’s biggest retirement home chains, a deal believed to exceed $1-billion that would give Beijing-based Anbang Insurance an important role in the delivery of health care in B.C.

Anbang Insurance Group, which has emerged in recent years to launch a global buying spree, has cut a deal to buy Vancouver-based Retirement Concepts, a family-owned retirement home business established in 1988.

This foreign takeover is currently under scrutiny by the federal government’s Investment Review Division because it exceeds the $600-million threshold and it will ultimately be up to Innovation Minister Navdeep Bains to make a decision.

Retirement Concepts owns and operates about 24 retirement “communities,” mostly in B.C., except for several properties in Calgary and Montreal. What makes it even more attractive is that it also owns holdings of unused or partly developed land that would allow a major expansion of facilities in the future.

The company is an important part of B.C.’s health-care delivery system. Retirement Concepts is the highest-billing provider of assisted living and residential care services in the province. The B.C. government paid the company $86.5-million in the 2015-16 fiscal year, more than any other of the 130 similar providers.

A source familiar with the deal said it exceeds $1-billion, but Retirement Concepts declined to confirm the size of the transaction. “The terms of the proposed transaction have not been disclosed publicly and we cannot comment on the amount you refer to,” said Azim Jamal, president and chief executive of Retirement Concepts.

Foreign investments are reviewed to determine whether they provide a net benefit to Canada and are compatible with this country’s industrial, economic and cultural policies and what impact they will have on Canadian participation in the business.

The Canadian government is eager to attract foreign money to make up for insufficient investment capital within Canada and acquisitions by foreigners are rarely rejected. Prime Minister Justin Trudeau is particularly eager to attract more investment from China and has begun exploratory free-trade talks with Beijing. The Liberals have already signalled they are open to rolling back a ban on state-owned Chinese investment in the oil sands imposed by former prime minister Stephen Harper.

Anbang appears to have gone to some lengths to conduct this B.C. deal below the radar.

The name of the firm acquiring Retirement Concepts is Cedar Tree Investment Canada, which was incorporated as a federal Canadian company only in July. Cedar Tree’s registration initially gave the names of its two directors as Hong Zhao and Ye Zhang with their contact address as Suite 2560 at 200 Granville St. in downtown Vancouver. People with the same names and address are also the two listed directors for Maple Red Financial Management Canada Inc., the company that Anbang used to buy a controlling interest in all four towers of Vancouver’s Bentall Centre last year.

The directors have since changed, as has their address, and Cedar Tree’s contact information is now a major Canadian law firm’s downtown Vancouver office.

Telephone calls and e-mails to Cedar Tree Investment’s listed directors were not returned. The Globe and Mail was also unable to reach anyone at Anbang International, Anbang Insurance’s global investment arm, at its Vancouver number.

In April, after abruptly walking away from an effort to buy Starwood Hotels & Resorts, one the world’s largest hotel companies, Anbang appears to have been shifting its attention to the Canadian market with a bid for Innvest, one of this country’s biggest hotel owners. This came amid reports from China that Chinese regulators were looking into whether its foreign asset acquisition binge – including the Waldorf Astoria hotel in New York – exceeded allowable limits.

Bloomberg News, citing a source involved in the transaction, reported that the CEO of the firm that would go on to buy Innvest, Bluesky Hotels & Resorts’ Li Chen, had said at the outset of the acquisition talks that she was representing Anbang but did not wish this company to be publicly identified as the buyer. Anbang later publicly denied “any connection” between it and Bluesky.

An investigation by The New York Times earlier this year revealed that 92 per cent of Anbang is currently held by firms either fully or partly owned by relatives of Anbang’s chairman, Wu Xiaohui, or his wife, the granddaughter of the former Chinese leader Deng Xiaoping, or Chen Xiaolu, the son of a famous People’s Liberation Army leader.

The B.C. retirement home acquisition thrusts Anbang into a new area of business: Canada’s health-care system.

Under international trade deals that Canada has signed, the provinces retain the right to refuse to give health-care contracts to foreign companies. That’s because Canada reserved the right in trade agreements for governments to discriminate against foreign suppliers of services in the health-care sector and foreign investors when it comes to health care.

Retirement Concepts, however, says it will remain as operator under a deal with Cedar Tree. Asked about how the Beijing company conducted itself in the transaction, Mr. Jamal said, “Anbang was transparent in its bidding from the outset.”

Mr. Jamal said Retirement Concept’s existing corporate team will remain intact to “provide continuity” to residents and the business.

“Under the partnership agreement, Retirement Concepts will retain a minority share and will continue to manage the day-to-day operations of all of our seniors’ communities,” the CEO said.

“As a result, there will be no change to staffing plans, the quality of care provided to our residents, nor to our policies, procedures and other operating standards.”

British Columbia’s Liberal government, however, says it is not concerned about the Retirement Concepts deal because it does not believe the patients at the company’s facilities will see a difference in the care they receive.

“Cedar Tree has assured patients, families and staff that it does not intend to make any changes to day to day operations, patient care, staff or leadership. In fact, they will all remain in operation as they are today,” B.C. Minister of Health Terry Lake said in a statement.

“We expect this change to be seamless, and that the patients residing in these facilities will continue to get the same quality of care.”

The B.C. government said nothing also prevents a foreign-owned company from owning a health-care provider.

“The Community Care and Assisted Living Act does not prohibit facilities from being sold to an out-of-province, or to an off-shore purchaser,” spokeswoman Kristy Anderson of B.C.’s Health Ministry said.

The Investment Review Division at the federal department of Innovation confirmed it’s reviewing the acquisition before Mr. Bains makes a decision. “Cedar Tree Investment Canada has filed an application for review under the Investment Canada Act of its proposed acquisition of Retirement Concepts,” spokeswoman Stéfanie Power said in a statement.

“Due to the confidentiality provisions of the Investment Canada Act, we cannot comment further on the timing of the review.”

The department likely received the application in late September or early October but it will not confirm the date the review began. “In general terms, the Minister has 45 days from the date the application is received to make a decision. However, the Minister can extend this period by 30 days. Further extensions are possible with the investor’s consent,” Ms. Power said.

China itself faces a daunting retirement-care challenge with a rapidly graying population and it is seeking the expertise and capacity to design the vast system necessary to look after its elderly.

————–

The agency warning about a strong risk of Canadian housing market problems on the horizon has been expected. “CMHC has recently observed spillover effects from Vancouver and Toronto into nearby markets,” said CMHC chief executive officer Evan Siddall said in an opinion column in The Globe and Mail. These nearby housing market effects have radiated from Vancouver to the Fraser Valley and particularly the Okanagan. The effect of Vancouver sellers purchasing properties in desirable areas beyond Vancouver proper, and Asian buyers purchasing properties in the Okanagan have been noted, following the same pattern as in Vancouver.

The agency warning about a strong risk of Canadian housing market problems on the horizon has been expected. “CMHC has recently observed spillover effects from Vancouver and Toronto into nearby markets,” said CMHC chief executive officer Evan Siddall said in an opinion column in The Globe and Mail. These nearby housing market effects have radiated from Vancouver to the Fraser Valley and particularly the Okanagan. The effect of Vancouver sellers purchasing properties in desirable areas beyond Vancouver proper, and Asian buyers purchasing properties in the Okanagan have been noted, following the same pattern as in Vancouver.

Source: CMHC to issue first ‘red’ warning for Canada’s housing market – The Globe and Mail

Canada’s housing agency is raising the alarm over the country’s real estate sector, warning about a strong risk of problems on the horizon.

Canada Mortgage and Housing Corp. will increase the risk rating in its overall assessment of the country’s residential market to “strong” from “moderate” when it issues a new report on Oct. 26.

“CMHC has recently observed spillover effects from Vancouver and Toronto into nearby markets,” CMHC chief executive officer Evan Siddall said in an opinion column in The Globe and Mail. “These factors will be reflected in our forthcoming Housing Market Assessment on Oct. 26. They will cause us to issue our first ’red’ warning for the Canadian housing market as a whole.”

CMHC’s decision to issue the red alert has been months in the making. Under the agency’s analysis that looks for “evidence of problematic conditions,” it rates 15 metropolitan markets based on weak (green), moderate (yellow) or strong (red) risk signals.

Earlier this month, federal Finance Minister Bill Morneau announced measures to tighten mortgage rules. Ottawa is also closing tax loopholes used by some foreign buyers.

“High levels of indebtedness coupled with elevated house prices are often followed by economic contractions,” Mr. Siddall said. “We expect Mr. Morneau’s actions therefore to support our economy. Seen this way, the resulting delay in when people can purchase their first home, or their decision to buy a smaller home, rent or stay put is rather a small price to pay.”

In July, CMHC increased its warning for Canada as a whole from weak to moderate. The Vancouver region has come under increased scrutiny this year.

“A ‘stress test’ using the higher Bank of Canada posted rate must now be used to underwrite guaranteed mortgages. This measure will help offset the highly stimulative effect of low interest rates,” Mr. Siddall said.

The federal Crown corporation changed its quarterly rating on the Vancouver area to moderate in April and to strong in July.

CMHC also saw Calgary, Saskatoon, Regina and Toronto as housing markets that showed strong signs in July of problems looming. Five markets were seen as having moderate risks (Edmonton, Winnipeg, Hamilton, Montreal and Quebec City) while five others were deemed weak for problematic conditions (Victoria, Ottawa, Halifax, Moncton and St. John’s).

The federal agency looks at four key areas of concern: “Overheating, price acceleration, overvaluation and overbuilding.” It cautioned in July that the country’s residential markets as a whole already displayed strong signs of being overvalued.

“House prices across Canada remain higher than levels consistent with personal disposable income, population growth and other fundamental factors,” CMHC said in July. It added that the risk of problematic conditions would increase “if the acceleration in prices intensifies in Ontario and British Columbia so as to outweigh challenges in the oil-dependent provinces.”

The B.C. government announced a 15-per-cent tax on purchases by foreign home buyers in the Vancouver region, effective Aug. 2.

Property sales last month in Greater Vancouver dropped 32.6 per cent from a year earlier, as the housing market adjusts to the impact from the B.C. tax on home buyers in the Vancouver area who are not Canadian citizens or permanent residents.

By contrast, residential sales in the Greater Toronto Area jumped 21.5 per cent in September, compared with the same month last year.