I want to more fully explain the concept of Strategic Inflection Points. I have referred to this topic in my Week 5 and Week 11 update videos. Former Intel CEO Andy Grove first described a strategic inflection point as a time in the life of a business when its fundamentals are about to change. That change can mean an opportunity to rise to new heights. But it may just as likely signal the beginning of the end. An inflection point can be the result of an action taken by a company or an action taken by another entity. An excellent recent example may be Facebook’s announced intention to enter the cryptocurrency market. The markets have already reacted sharply to Facebook’s move. Analysts have suggested that it may significantly alter the forecasts for cryptocurrencies. Change is inevitable and change is happening more rapidly than ever. Adaptation to change is imperative for corporate survival.

I want to more fully explain the concept of Strategic Inflection Points. I have referred to this topic in my Week 5 and Week 11 update videos. Former Intel CEO Andy Grove first described a strategic inflection point as a time in the life of a business when its fundamentals are about to change. That change can mean an opportunity to rise to new heights. But it may just as likely signal the beginning of the end. An inflection point can be the result of an action taken by a company or an action taken by another entity. An excellent recent example may be Facebook’s announced intention to enter the cryptocurrency market. The markets have already reacted sharply to Facebook’s move. Analysts have suggested that it may significantly alter the forecasts for cryptocurrencies. Change is inevitable and change is happening more rapidly than ever. Adaptation to change is imperative for corporate survival.

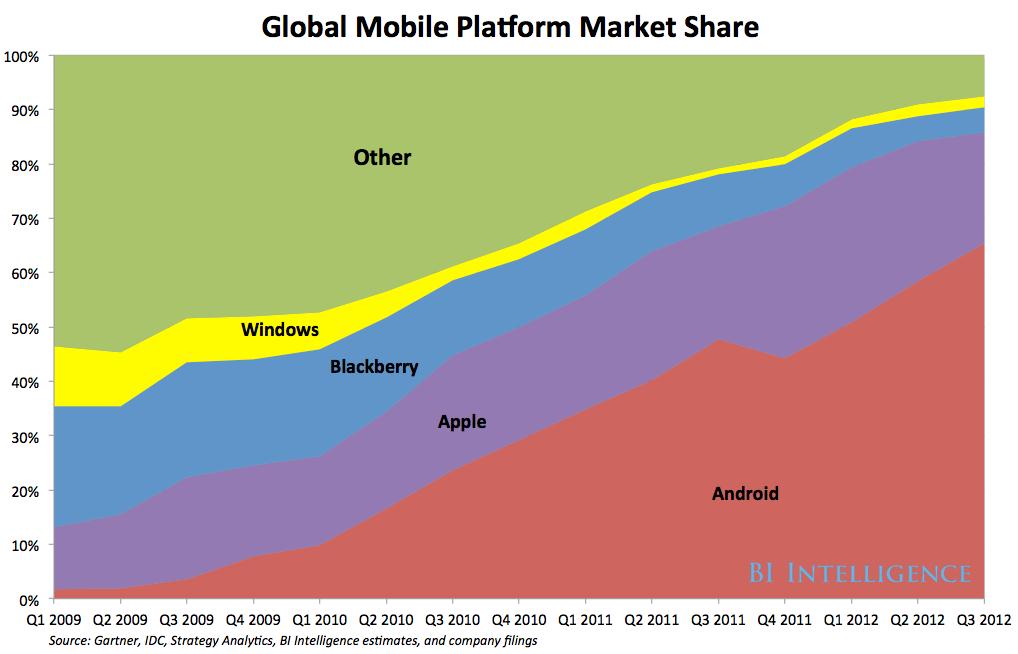

NOTE: My original post, originally published in January 2013, continues to be one of the most viewed on the site. Android and Apple have enjoyed an estimated 98% market share between the two, and many of my earlier projections regarding this market appear to have been borne out. However, the smartphone market has now matured to the point that it is at a strategic inflection point which has major implications for the future of this market and the major competitors. The rapid maturation of the smartphone market should have been foreseen: the rise of domestic Chinese competition combined with the predictable end of the Western consumer fascination with “the next smartphone”

NOTE: My original post, originally published in January 2013, continues to be one of the most viewed on the site. Android and Apple have enjoyed an estimated 98% market share between the two, and many of my earlier projections regarding this market appear to have been borne out. However, the smartphone market has now matured to the point that it is at a strategic inflection point which has major implications for the future of this market and the major competitors.

The Rapid Maturation of the Smartphone Market Should Have Been Foreseen

The signs of a dangerous strategic inflection point in the global smartphone market have been evident for some time: the rapid rise of domestic Chinese competition combined with the predictable end of the Western consumer fascination with “the next smartphone.” Five years ago, Samsung Electronics, the South Korean technology giant sat atop the Chinese market, selling nearly one of every five devices there. Today, Samsung is an also-ran, controlling less than 1% of the world’s largest smartphone market. Samsung has trimmed local staff and last month closed one of its two Chinese smartphone factories. Surely, Apple must have been aware of this and the growing number of much lower cost domestic Chinese competitors that were already hammering Samsung. Apple’s release of a lower cost iPhone, the XR, in Asia in October 2018 appears to have been a case of too little too late. Sales of the device have been disappointing in both Japan and China, and Apple has been relegated to offering “trade-ins” to camouflage slashing the price of the XR. Apple had ample warning over at least a five year period.

Meanwhile, I sensed a very different kind of maturation of the smartphone market in North America and Europe. In what I like to call the smartphone market “Star Wars” phenomenon, each new generation of smartphones was greeted with a hysteria that was only paralleled by the Star Wars craze. This simply could not continue indefinitely. Beginning in 2017 it was apparent the smartphone market as a whole was already shrinking, and there was significant anecdotal information in the media that smartphone hysteria was waning, if not publicly available hard data. I began having discussions about this with Tim Bajarin, one of the top Apple analysts. As Apple moved to launch the iPhone X and broke the $1000 price point barrier it encountered clear if perhaps not overwhelming evidence that the smartphone market was softening: more people chose not to upgrade their phones. I like to say that the last major feature consumers seemed to want/need was water resistance, as so many had already experienced the disastrous “toilet drop.” I view the Bluetooth earbud phenomenon as a distraction and perhaps a hint of the coming change. Samsung flirted with water resistance as early as the Samsung Galaxy S5, perhaps because water resistance had become a standard feature in the Japanese market. By 2018, water resistance was standardized, and the market began experimenting with “the next big thing” for phones, folding screens. WTF? It was clear to me that the smartphone market had run out of gas, and was undergoing rapid maturation, as phones were no longer fascinating and novel, but just simply commodity devices.

To my mind, and IMHO, this has been a case study in a classic “strategic inflection point” that was missed by both Samsung and Apple. Samsung might be forgiven for being the first to cross into the inflection point, while the media was still promoting “the next smartphone” hysteria, and not yet recognizing the sense of the market. Apple has no such excuse. The rapid maturation of the smartphone market should have been foreseen by Apple. Apple’s most disturbing move was the decision to increase pricing rather than delivering greater value, at exactly the wrong time. The crucial rhetorical question is what are the larger implications for Apple’s future business?

Smartphone vendors shipped a total of 355.6 million units worldwide during the third quarter of 2018 (Q3 2018), resulting in a 5.9% decline when compared to the 377.8 million units shipped in the third quarter of 2017. The drop marks the fourth consecutive quarter of year-over-year declines for the global smartphone market.

Quarter

2017Q1

2017Q2

2017Q3

2017Q4

2018Q1

2018Q2

2018Q3

Samsung

23,2%

22,9%

22,1%

18,9%

23,5%

21,0%

20,3%

Huawei

10,0%

11,0%

10,4%

10,7%

11,8%

15,9%

14,6%

Apple

14,7%

11,8%

12,4%

19,6%

15,7%

12,1%

13,2%

Xiaomi

4,3%

6,2%

7,5%

7,1%

8,4%

9,5%

9,5%

OPPO

7,5%

8,0%

8,1%

6,9%

7,4%

8,6%

8,4%

Others

40,2%

40,1%

39,6%

36,8%

33,2%

32,9%

33,9%

TOTAL

100,0%

100,0%

100,0%

100,0%

100,0%

100,0%

100,0%

2009 to 2012

In one of the most interesting high tech scenarios in years, the “smart mobile” OS (operating system) market is shaping up to be a classic Battle of the Titans. Key strategic issues, theories, speculation, and money, lots of it, are making this a great real-time strategy and marketing case study for management students of all ages (smile). So as Dell prepares to fade into the sunset, get yourself a drink of your choice, and some popcorn, sit back and watch it all unfold.

The best metaphor I can apply to this might be a “destruction derby” featuring at least two players, or perhaps a bizarre multidimensional Super Bowl or Rugby World Cup match, with four teams on one playing field with four goal posts at each cardinal point of the compass.. At the moment all four teams are tackling, passing, and running at each other in a confused pile. There are scrums, rucks and mauls in multiple locations. Two competitors, Google and Apple appear to be winning. The other two, Microsoft and Research in Motion, are pretty banged up, but still playing.

The two currently dominant competitors, Google Android with its acquisition of Motorola Mobility, and Apple IOS are rapidly consolidating and expanding their global market positions, via partnerships, vertical integration, and application development ecosystems. Microsoft has publicly committed to spending massively to make Windows 8 the third OS option, but a recent IDC mobile OS market forecast projects Microsoft with only a miniscule share in 2015. Something tells me that Steve Ballmer will go on a rampage if that happens, rather like the video of him screaming and dancing on stage in my post “Extrovert or Introvert, Authentic Presentations Take Practice,” November 30th. http://mayo615.com/2012/11/30/introvert-or-extrovert-authentic-presentations-take-practice/

The key question is whether Microsoft or RIM, will be able to establish a third mobile OS to a survivable market position. It is not at all clear that either can do so at this point. The market is also speculating that mobile hardware market leader Samsung, is possibly considering making its own play by creating its own mobile OS ecosystem. While this may seem far fetched, this kind of vertical integration seems to be making a resurgence as a strategic move, after having been discredited. Then there is the perennial Nokia, who has seemed to be on death’s door, but may be coming back. As a strategic partner for Microsoft, Nokia’s fate may have a huge bearing on Microsoft’s strategy to reinvent itself as the PC goes into atrial fibrillation. Will Amazon enter the fray with its own smart phone entrant, and if so, with whose OS? Will Research in Motion and the Blackberry be able to achieve a survivable market share, or is RIM already a walking zombie?

Finally, in a kind of death dance patent dispute reminiscent of the film, Gladiator, Nokia and RIM are now locked in new lawsuits and counter-lawsuits, as if to say, “If neither of us are going to survive, we might as well kill each other for the entertainment value.”

Here’s a more concise overview of the race to be the third mobile platform:

For Management students, this real time case study offers the opportunity to apply and ponder:

1. The time tested 1976 Boston Consulting Group (Bruce Henderson)“rule of three and four.” In a stable mature market there can be no more than three surviving competitors, the largest of which can have no more than four times the share of the smallest of the three. Here, the question is whether a third competitor can successfully emerge at all?

2.Barriers to market entry. Former Intel Marketing VP, Bill Davidow‘s book, Marketing High Technology, An Insider’s View, still considered the standard on the topic, suggested his own metric for a barrier to a new market entrant, or even a competitor just struggling to survive the market shakeout. The market entry barrier rule of thumb in dollars is three-quarters the most recent annual revenue of the market leader. In this case, that is a very big B number… Microsoft has the bucks, but is it just too late?

3. Vertical integration. Rumors of Samsung introducing its own mobile OS seem implausible, but hey Nvidia just announced its own gaming console to compete with Microsoft, Nintendo, and Sony.

4. Resources and capabilities. It is necessary to consider the respective resources and capabilities of each of the many direct players, and those playing in related markets that bear on the mobile OS market.

5. Related markets, new markets, peripherally involved competitors and products which all could play a role in the eventual outcome of this. The integrated Internet HDTV market is only one example. Featuring Apple, Microsoft, Google, and Samsung, and the HDTV manufacturers, it could influence things. What if Amazon were to vertically integrate and introduce its own smart phone?

This is the hairball of this Century so far. Are you all still with me, here?

LinkedIn shares yesterday plummeted precipitously after the company announced poorer than expected results, and downgraded prospects for the remainder of the year. Looking beyond the downgraded forecast and the costs associated with the $1.5 Billion acquisition of lynda.com, some analysts scrutinizing the press release, noted that there was no growth reported in the user base of “over 350 million users”, despite moves into China and other markets. Premium user revenue grew significantly but that did not come near to offsetting the total revenue number. Revenue and number of users are the two numbers followed most closely by investment analysts.

LinkedIn’s recent acquisitions have been noted as a LinkedIn strategy for compensating for flat overall user growth, and for diversifying into new markets to augment growth.

LinkedIn shares yesterday plummeted precipitously after the company announced poorer than expected results, and downgraded prospects for the remainder of the year. Looking beyond the downgraded forecast and the costs associated with the $1.5 Billion acquisition of lynda.com, some analysts scrutinizing the press release, noted that there was no growth reported in the user base of “over 350 million users”, despite moves into China and other markets. Premium user revenue grew significantly but that did not come near to offsetting the total revenue number. Revenue and number of users are the two numbers followed most closely by investment analysts.

LinkedIn’s recent acquisitions have been noted as a LinkedIn strategy for compensating for flat overall user growth, and for diversifying into new markets to augment growth.

Some journalists are already asking if the market is over-reacting to LinkedIn’s downgraded forecast yesterday. The company has demonstrated solid results since it went public in 2011, and management seems to be confidently “in charge.” However, in my personal view, as a LinkedIn user for many years, I do think that the sell-off by shareholders may be justified and prudent, even if most analysts have not followed the company as closely as some others. I have this sinking feeling of LinkedIn losing its way, strategic errors, and the accelerated corporate life cycle in social media, in Silicon Valley, and at LinkedIn in particular. John Chambers has commented on this rapid pace of change in the context of his management of Cisco Systems. It is also akin to Andy Grove’s “strategic inflection point,”where the fundamentals of a business are changing but management may or may not realize it, and may or may not take the appropriate actions. Put plainly, something simply doesn’t feel right in my gut about LinkedIn

My concerns fall into three major areas: acquisitions, Premium user subscriptions, and LinkedIn user Terms & Conditions.

1. While observers have complimented LinkedIn management for some of their recent moves to acquire synergistic businesses in new markets, other moves have seemed ill-conceived and poorly executed. I wrote on this blog about the curious LinkedIn acquisition of CardMunch, a business card processing app for smartphones. The application was only available on iPhones, and enjoyed first-mover status, but the assumption was that an Android version would be imminent for obvious reasons. That never happened. After more than a year of doing nothing with the app and “leaving open a competitive market opportunity window the size of an aircraft carrier,” LinkedIn announced that it was changing focus to Evernote business card services, and apparently ceasing support for CardMunch. IMHO, the amount of time LinkedIn frittered away on this left them no option but to kill the app. While LinkedIn may argue that Evernote provides its users with a superior solution as justification for their decision, if LinkedIn had moved promptly when they had the opportunity, partnering with Evernote would have been unnecessary. There is also the matter of the money wasted on Linkedin’s original acquisition of Cardmunch, though the Cardmunch founders may feel they dodged a bullet, and probably now own LinkedIn stock.

2. Yesterday’s announcement noted that LinkedIn Premium subscriptions had grown dramatically in the last year. What we do not know is the raw number of Premium subscribers so the percentage numbers may be misleading. My sense of Premium subscriptions is that there is a significant amount of “churn” in Premium subscriptions. That is to say that LinkedIn may be adding numbers of users in new markets but the core base of Premium subscribers may be simultaneously eroding in the core U.S. market. My evidence is based on a recent LinkedIn Support discussion asking users their assessment of the value from their Premium subscription. The responses were an almost unanimous torrent of complaints of limited to no value experienced from paying the Premium subscription. This was only the most recent incident.

3. LinkedIn’s Terms & Conditions seem to have morphed into policies designed to make the site more of an app for recruiters and staffing personal than a “professional networking” site. I think I can safely stick my neck out and say that while LinkedIn was originally conceived as a professional networking site, few if any users truly think of the site or use it for professional networking. It is a bit of an arm’s length experience for LinkedIn users. The oft cited 3rd Level connections are useless. I will go farther and say that I do not know of anyone in my 500+ network who has successfully secured a senior position via LinkedIn. As we all know, this happens primarily through the kind of networking that does not occur on LinkedIn. In an odd turn of events, LinkedIn Groups policy was unilaterally changed without notice or discussion. The change enabled group admins to unilaterally bar specific group members from posting discussions for reasons that were obscure. The obvious problem was admin censorship and bias against a particular user. The apparent concern was that some users were posting discussions to multiple groups, though this was never made clear. The decision led to an uproar of angry comments on the LinkedIn Support Forum. After weeks of stonewalling and stalling, LinkedIn finally reversed the policy in the face of the stiff criticism from users. To me this smacked of Facebook’s ill-conceived policy changes which were eventually reversed.

In summary, I think LinkedIn has evolved into something very different than the site/application that many original users imagined they were joining and using. This fact seems to be sinking in with users, some of whom are showing increasing dissatisfaction with LinkedIn and with paying for Premium services that do not seem to offer value. I sometimes wonder about the people who view my profile, many of whom have no professional connection to me whatsoever and may be halfway around the World from me. Some of the new businesses sound interesting potentially, but I am not at all certain that I would use them. I have expressed concerns that the LinkedIn brand itself is being tarnished and devalued by some of the changes and policies. Most concerning, I wonder if LinkedIn management are aware of these issues and even admitting it to themselves, if not to analysts.

*I want to first declare that I have no special insight or information regarding LinkedIn. My comments and opinions on LinkedIn are based only on my own observations over a considerable period of time, my own interaction with LinkedIn Support, and recent media articles on LinkedIn.

Stanford Graduate School of Business and Harvard Business School are adopting drastically different strategies for delivering business education. These differing strategies are reflected in the debate that has erupted between two of Harvard Business School’s best known professors and their visions for the future of business education, Michael Porter and Clayton Christensen. I have also been personally tire kicking MOOC’s, acting as a mentor for Stanford’s online Technology Entrepreneurship course, hosted by NovoEd. I have been pleasantly surprised by the experience, and among the teams I am mentoring is a group of Xerox senior research scientists acting as an entrepreneurial team.

Harvard Professor Clayton Christensen, author of The Innovator’s Dilemma

Harvard Professor Michael Porter, author of numerous books on Competitive Strategy

Stanford Graduate School of Business and Harvard Business School are adopting drastically different strategies for delivering business education. These differing strategies are reflected in the debate that has erupted between two of Harvard Business School’s best known professors and their visions for the future of business education, Michael Porter and Clayton Christensen. I have also been personally tire kicking MOOC’s, acting as a mentor for Stanford’s online Technology Entrepreneurshipcourse, hosted by NovoEd. I have been pleasantly surprised by the experience, and among the teams I am mentoring, is a group of Xerox senior research scientists acting as an entrepreneurial team.

Christensen predictably argues, as in his most famous book, that in order to survive disruptive change, businesses themselves must embrace disruptive change. Professor Porter on the other hand, argues that an enterprise “… must stay the course, even in times of upheaval, while constantly improving and extending its distinctive positioning.” Ironically, this debate is closely related to my most recent post, and a much earlier post on recognizing “strategic inflection points,” and acting on them.

If any institution is equipped to handle questions of strategy, it is Harvard Business School, whose professors have coined so much of the strategic lexicon used in classrooms and boardrooms that it’s hard to discuss the topic without recourse to their concepts: Competitive advantage. Disruptive innovation. The value chain.

But when its dean, Nitin Nohria, faced the school’s biggest strategic decision since 1924 — the year it planned its campus and adopted the case-study method as its pedagogical cornerstone — he ran into an issue. Those professors, and those concepts, disagreed.

The question: Should Harvard Business School enter the business of online education, and, if so, how?

Universities across the country are wrestling with the same question — call it the educator’s quandary — of whether to plunge into the rapidly growing realm of online teaching, at the risk of devaluing the on-campus education for which students pay tens of thousands of dollars, or to stand pat at the risk of being left behind.

Photo

Harvard Business School faced a choice between different models of online instruction. Prof. Michael Porter favored the development of online courses that would reflect the school’s existing strategy.CreditDavid De la Paz/European Press Photo Agency

At Harvard Business School, the pros and cons of the argument were personified by two of its most famous faculty members. For Michael Porter, widely considered the father of modern business strategy, the answer is yes — create online courses, but not in a way that undermines the school’s existing strategy. “A company must stay the course,” Professor Porter has written, “even in times of upheaval, while constantly improving and extending its distinctive positioning.”

For Clayton Christensen, whose 1997 book, “The Innovator’s Dilemma,” propelled him to academic stardom, the only way that market leaders like Harvard Business School survive “disruptive innovation” is by disrupting their existing businesses themselves. This is arguably what rival business schools like Stanford and the Wharton School have been doing by having professors stand in front of cameras and teach MOOCs, or massive open online courses, free of charge to anyone, anywhere in the world. For a modest investment by the school — about $20,000 to $30,000 a course — a professor can reach a million students, says Karl Ulrich, vice dean for innovation at Wharton, part of the University of Pennsylvania.

“Do it cheap and simple,” Professor Christensen says. “Get it out there.”

But Harvard Business School’s online education program is not cheap, simple, or open. It could be said that the school opted for the Porter theory. Called HBX, the program will make its debut on June 11 and has its own admissions office. Instead of attacking the school’s traditional M.B.A. and executive education programs — which produced revenue of $108 million and $146 million in 2013 — it aims to create an entirely new segment of business education: the pre-M.B.A. “Instead of having two big product lines, we may be on the verge of inventing a third,” said Prof. Jay W. Lorsch, who has taught at Harvard Business School since 1964.

Starting last month, HBX has been quietly admitting several hundred students, mostly undergraduate sophomores, juniors and seniors, into a program called Credential of Readiness, or CORe. The program includes three online courses — accounting, analytics and economics for managers — that are intended to give liberal arts students fluency in what it calls “the language of business.” Students have nine weeks to complete all three courses, and tuition is $1,500. Only those with a high level of class participation will be invited to take a three-hour final exam at a testing center.

“We don’t want tourists,” said Jana Kierstead, executive director of HBX, alluding to the high dropout rates among MOOCs. “Our goal is to be very credible to employers.” To that end, graduates will receive a paper credential with a grade: high honors, honors, pass.

“Harvard is going to make a lot of money,” Mr. Ulrich predicted. “They will sell a lot of seats at those courses. But those seats are very carefully designed to be off to the side. It’s designed to be not at all threatening to what they’re doing at the core of the business school.”

Exactly, warned Professor Christensen, who said he was not consulted about the project. “What they’re doing is, in my language, a sustaining innovation,” akin to Kodak introducing better film, circa 2005. “It’s not truly disruptive.”

‘Very Different Places’

Professor Christensen did something “truly disruptive” in 2011, when he found himself in a room with a panoramic view of Boston Harbor. About to begin his lecture, he noticed something about the students before him. They were beautiful, he later recalled. Really beautiful.

“Oh, we’re not students,” one of them explained. “We’re models.”

They were there to look as if they were learning: to appear slightly puzzled when Professor Christensen introduced a complex concept, to nod when he clarified it, or to look fascinated if he grew a tad boring. The cameras in the classroom — actually, a rented space downtown — would capture it all for the real audience: roughly 130,000 business students at the University of Phoenix, which hired Professor Christensen to deliver lectures online.

Why had his boss, Mr. Nohria, given him permission to moonlight? “Because we didn’t have an alternative of our own” online, Mr. Nohria explained.

The dean had taken a wait-and-see approach — until 18 months ago, when his own university announced the formation of edX, an open-courseware platform that would hitch the overall university firmly to the MOOC bandwagon.

He said he remembered listening to an edX presentation at an all-university meeting. “I must confess I was unsure what we’d be really hoping to gain from it,” he said. “My own early imagination was: ‘This is for people who do lectures. We don’t do lectures, so this is not for us.’ ” In the case method, concepts aren’t taught directly, but induced through student discussion of real-world business problems that professors guide with carefully chosen questions.

“Nitin and I are close friends, and we’ve talked about this repeatedly,” Professor Porter said. “I think the big risk in any new technology is to believe the technology is the strategy. Just because 200,000 people sign up doesn’t mean it’s a good idea.” Though Professor Porter published “Strategy and the Internet” in the Harvard Business Review in 2001, before the advent of MOOCs, the article makes his sternest warning about the perils of online recklessness: “A destructive, zero-sum form of competition has been set in motion that confuses the acquisition of customers with the building of profitability.”

Mr. Nohria ultimately chose for the business school to opt out of edX. But this decision forced a question: What should the school do instead? “People came out in very different places,” Mr. Nohria said. “Very different places.”

One morning, he sat down for one of his regular breakfasts with students. “Three of them had just been in Clay’s course,” which had included a case study on the future of Harvard Business School, Mr. Nohria said. “So I asked them, ‘What was the debate like, and how would you think about this?’ They, too, split very deeply.”

Some took Professor Christensen’s view that the school was a potential Blockbuster Video: a high-cost incumbent — students put the total cost of the two-year M.B.A. at around $100,0000 — that would be upended by cheaper technology if it didn’t act quickly to make its own model obsolete. At least one suggested putting the entire first-year curriculum online.

Photo

On the topic of online instruction, Prof. Clayton Christensen said: ‘Do it cheap and simple. Get it out there.”CreditRick Friedman for The New York Times

Others weren’t so sure. “ ‘This disruption is going to happen,’ ” is how Mr. Nohria described their thinking, “ ‘but it’s going to happen to a very different segment of business education, not to us.’ ” The power of Harvard’s brand, networking opportunities and classroom experience would protect it from the fate of second- and third-tier schools, a view that even Professor Christensen endorses — up to a point.

“We’re at the very high end of the market, and disruption always hits the high end last,” said Professor Christensen, who recently predicted that half of the United States’ universities could face bankruptcy within 15 years.

Mr. Nohria states flatly, “I do not believe our M.B.A. program is at risk.” He concluded that disruption is not always “all or nothing,” and cited the businesses of music and retailing as examples. “In the music business, all record stores are gone,” he said, while in retailing, “it’s not like Amazon has eliminated everything; after those debates, my feeling was that we’re going to be more in that category.”

Still, Mr. Nohria said, he wanted some insurance. “Our beliefs can always turn out to be wrong,” he said. Harvard Business School could not afford to stand on the sidelines. So last summer, he said, he asked the business school’s administrative director, “What would you say if we started a little skunk works around this technology?”

‘Hollywood’ at Harvard

That skunk works, in a low-slung building 300 yards from campus, is not little. It buzzes with 35 full-time staff members — Wharton’s online efforts, by comparison, employ one-half of one staffer, Mr. Ulrich said — who are scrambling to complete a proprietary platform that, after this summer’s limited go-round, could support much larger enrollments.

“Here’s Hollywood,” Ms. Kierstead said on a recent tour, passing an array of video equipment that’s hauled around to film business case-study protagonists on location. Nearby, two digital animators worked on graphics for Professor Christensen’s forthcoming course. Another staff member handled financial aid.

To run HBX with Ms. Kierstead, Mr. Nohria tapped Bharat Anand, 48, a strategy professor who had been researching how traditional media companies have coped, or haven’t, with digital disruption. “I think about those cases a lot,” said Professor Anand, who is also Mr. Nohria’s brother-in-law.

The dean handed him a sheet of six guiding principles, including these: HBX should be economically self-sustaining. It should not substitute for the M.B.A. program. It should seek to replicate the Harvard Business School discussion-based style of learning. This was no easy assignment, Professor Anand conceded.

“What is competitive advantage?” he asked, invoking Professor Porter’s signature theory. “It comes from being fundamentally different. We teach this all the time. But saying it is one thing. Putting it into practice is hard. When everyone is going free, everyone is going with a similar type of platform, it takes courage to do your own thing.”

On campus, Harvard business students face one another in five horseshoe-shaped tiers with oversized name cards. They fight for “airtime” while the professor orchestrates discussion from a central “pit.”

“We don’t do lectures,” Mr. Nohria said. “Part of what had already convinced me that MOOCs are not for us is that for a hundred years our education has been social.”

The challenge was to invent a digital architecture that simulated the Harvard Business School classroom dynamic without looking like a classroom. In a demonstration of a course called economics for managers, the first thing the student sees is the name, background and location — represented by glowing dots on a map — of other students in the course.

A video clip begins. It’s Jim Holzman, chief executive of the ticket reseller Ace Ticket, estimating the supply of tickets for a New England Patriots playoff game: “Where I have a really hard time is trying to figure out what the demand is. We just don’t know how many people are on the sidelines saying, ‘Hey, I’m thinking about going.’ ”

It’s a complex situation meant to get students thinking about a key concept — “the distinction between willingness to pay and price,” Professor Anand said. “Just because something costs zero doesn’t mean people aren’t willing to pay something.” A second case study, on the pay model of The New York Times, drives the point home.

Then a box pops up on the screen with the words “Cold Call.” The student has 30 seconds to a few minutes to type a response to a question and is then prodded to assess comments made by other students. Eventually there is a multiple-choice quiz to gauge mastery of the concept. (This was surprisingly time-consuming to develop, Professor Anand said, because the business school does not give multiple-choice tests.)

At a faculty meeting in April, Professor Anand demonstrated the other two elements of HBX: continuing education for executives and a live forum. He unveiled the existence of a studio, built in collaboration with Boston’s public television station, that allows a professor to stand in a pit before a horseshoe of 60 digital “tiles,” or high-definition screens with the live images and voices of geographically dispersed participants. “I’m proud of our team, and how carefully they’ve thought about it even before they’ve done it,” Professor Porter said.

The Clashing Models

Not everyone was so impressed. Professor Christensen, for one, worried that Harvard was falling into the very trap he had laid out in “The Innovator’s Dilemma.” “I think that we’ve way overshot the needs of customers,” he said. “I worry that we’re a little too technologically ambitious.”

Photo

The dean, Nitin Nohria, found that students were also divided on the issue of online instruction.CreditRick Friedman for The New York Times

He also feared that HBX was tied too closely to the business school.

“There have been a few companies that have survived disruption, but in every case they set up an independent business unit that let people learn how to play ball in the new game,” he said. IBM survived the transition from mainframe computers to minicomputers, and then from minicomputers to personal computers, by setting up autonomous teams in Minnesota and then in Florida. “We haven’t got the separation required.”

Professor Porter has expressed the opposite view. Companies that set up stand-alone Internet units, he wrote in 2001, “fail to integrate the Internet into their proven strategies and thus never harness their most important advantages.” Barnes & Noble’s decision to set up a separate online unit is one of his cautionary tales. “It deterred the online store from capitalizing on the many advantages provided by the network of physical stores,” he said, “thus playing into the hands of Amazon.”

Here is where the two professors’ differences come to a head. In the Porter model, all of a company’s activities should be mutually reinforcing. By integrating everything into one, cohesive fortification, “any competitor wishing to imitate a strategy must replicate a whole system,” Professor Porter wrote.

In the Christensen model, these very fortifications become a liability. In the steel industry, which was blindsided by new technology in smaller and cheaper minimills, heavily integrated companies couldn’t move quickly and ended up entombed inside their elaborately constructed defenses.

“If Clay and I differ, it’s that Clay sees disruption everywhere, in every business, whereas I see it as something that happens every once in a while,” Professor Porter said. “And what looks like disruption is in fact an incumbent firm not embracing innovation” at all.

In other words, it’s not that U.S. Steel was destined to be undone by minimills. It’s that its managers let it happen.

“The disrupter doesn’t always win,” argued Professor Porter, who nonetheless called Professor Christensen “phenomenal” and “one of the great management thinkers.”

Who will win the coming business school shakeout? Professor Porter acknowledged that it’s a multidimensional question.

Most schools offering MOOCs do so through outside distribution channels like Coursera, a for-profit company that has Duke, Wharton, Yale, the University of Michigan and several dozen other schools in its stable. EdX, of which Harvard was a co-founder with the Massachusetts Institute of Technology, counts Dartmouth and Georgetown among its charter members.

“These will come to have considerable power,” predicted Jeffrey Pfeffer, a professor of organizational behavior at the Stanford Graduate School of Business. He pointed to the aircraft industry: “In order to get into China, Boeing transferred its technology to parts manufacturers there. Pretty soon there’s going to be Chinese firms building airplanes. Boeing created their own competition.” Business schools, he said, “are doing it again; we are creating our own demise.”

Professors as Online Stars

The worry is all the more acute at midtier schools, which fear that elite business schools will move to gobble up a larger share of a shrinking pie.

“Would you rather watch Kenneth Branagh do ‘Henry V,’ or see it at a community theater?” asked Mr. Ulrich at Wharton. “There are going to be some instructors who become more valuable in this new world because they master the new medium. We’d rather be those guys than the people left behind.”

This raises a still more radical case, in which the winners are not any institution, new or old, but a handful of star professors. One of Professor Porter’s generic observations — that the Internet increases the “bargaining power of suppliers” — suggests just that. “It’s potentially very divisive in a way,” he acknowledged. “We’re all partners; we all get paid roughly the same. Anything that starts to fracture the enterprise is a sobering prospect.”

François Ortalo-Magné, dean of the University of Wisconsin’s business school, says fissures have already appeared. Recently, a rival school offered one of his faculty members not just a job, but also shares in an online learning start-up created especially for him. “We’re talking about millions of dollars,” Mr. Ortalo-Magné said. “My best teachers are going to find platforms so they can teach to the world for free. The market is finding a way to unbundle us. My job is to hold this platform together.”

To that end, he has changed his school’s incentive structure, which, as in most of academia, was based primarily on the number of research articles published in elite journals. Now professors who can’t crack those journals but “have a gift for inspiring learning,” he said, in person or online, are being paid as top performers, too. “We are now rewarding people who have tenure to give up on research,” Mr. Ortalo-Magné said.

Mr. Ortalo-Magné spins out the possibilities of disruption even further. “How many calculus professors do we need in the world?” he asked. “Maybe it’s nine. My colleague says it’s four. One to teach in English, one in French, one in Chinese, and one in the farm system in case one dies.”

What is to stop a Coursera from poaching Harvard Business School faculty members directly? “Nothing,” Mr. Nohria said. “The decision people will have to make is whether being on the platform of Harvard Business School, or any great university, is more important than the opportunity to build a brand elsewhere.

“Does Clay Christensen become Clay Christensen just by himself? Or does Clay Christensen become Clay Christensen because he was at Harvard Business School? He’ll have to make that determination.”

This is another on my series on industry analysis. The recent University of Ottawa study on the demise of Nortel Networks, tells us what many of us already knew. The most important constructive criticism of this study is that it should have been done years ago. The Nortel collapse was followed by a surprisingly similar scenario at RIM, now Blackberry. Mike Lazaridis, who served as RIM’s co-CEO along with Jim Balsillie until January, 2012, are generally considered to have failed to respond adequately to the market encroachments of Apple’s iPhone and Google’s Android phones, as Blackberry’s market share plummeted. I recently showed my undergrad and graduate strategy students a video of a Charlie Rose interview with John Chambers, CEO of Cisco Systems. Chambers emphasized the acceleration of the Adizes corporate life cycle, in many cases to less than ten years, and the need for constant reinvention to survive in this challenging and rapidly changingnew world.

Former Nortel CEO John Roth

Former RIM CEO, Jim Balsillie

This is another on my series on industry analysis. The recent University of Ottawa study on the demise of Nortel Networks, tells us what many of us already knew. The researchers should be congratulated for their work and their conclusions, in what is an important case study of Canadian corporate mismanagement, which will help Canadian business avoid a deja vu. But many of us in the high tech industry already knew the answer in our guts. The most important constructive criticism of this study is that it should have been done years ago. The Nortel collapse was followed by a surprisingly similar scenario at RIM, now Blackberry. Mike Lazaridis, who served as RIM’s co-CEO along with Jim Balsillie until January, 2012, are generally considered to have failed to respond adequately to the market encroachments of Apple’s iPhone and Google’s Android phones, as Blackberry’s market share plummeted. There seems to be a pattern here for students of Canadian innovation and management. I recently showed my undergrad and graduate strategy students a video of a very recent Charlie Rose interview with John Chambers, CEO of Cisco Systems. In that interview Chambers emphasized the acceleration of the Adizes corporate life cycle, in many cases to less than ten years, and the need for constant reinvention to survive in this challenging and rapidly changingnew world. This is now also true about the teaching of Information Technology to management students and to all undergraduate students for that matter.

Cisco System’s CEO, John Chambers discusses the acceleration of the corporate life cycle: Chambers Interview

The collapse of telecommunications giant Nortel Networks Corp. was caused by “a culture of arrogance and even hubris” that led to numerous management errors and weakened the firm’s ability to adapt to changing customer needs in a fast-paced industry, according to a new in-depth analysis of the company’s final decade of operations.

A University of Ottawa team of professors, led by lead researcher Jonathan Calof, released a detailed analysis Monday of Nortel’s failure, outlining a litany of complex factors that caused Nortel’s collapse in 2009, when the firm filed for bankruptcy protection and was disbanded.

The report is based on three years of research and dozens of interviews with former employees, executives and top customers to try to understand what went wrong at the company. The project was launched after former chief executive officer Jean Monty approached the research team and offered to contribute to the financing of the project.

The study concludes that Nortel lacked the internal “resilience” to cope with a changing external marketplace, and missed key opportunities between 2002 and 2006 to retrench as it struggled to survive. In the end, customers said they could not stick with Nortel as a “black cloud” formed over the company, raising doubts about its long-term future.

Prof. Calof said in a release Monday that the findings are “more than a Nortel story” and present broader lessons about preventing further failures of large companies in Canada.

“It’s our hope that this research will aid in educating tomorrow’s leaders,” he said.

The report says Nortel in its early days was a model of deep technological expertise through its Bell Northern Research (BNR) laboratories and its strong connection to customers, enabling the company to maintain a “first-mover” advantage in many markets. At its peak in 2000, Nortel was Canada’s largest public company, accounting for a third for the value of the S&P/TSX composite index, and employed more than 93,000 people worldwide.

But the authors concluded that Nortel’s growing dominance in its markets in the 1990s “led to a culture of arrogance and even hubris combined with lax financial discipline. Nortel’s rigid culture played a defining role in the company’s inability to react to industry changes.”

While Nortel doubled its revenue between 1997 and 2000 through a spree of expensive acquisitions – and tripled its share price in the same period – the company lost focus on profitability and was in a “precarious position” when the market for technology companies crashed in 2001, the report says. The report says its acquisition spree was a “complete departure” from Nortel’s established skills base and from its tradition of developing its own products.

“This approach proved to be a failure because ill-chosen and poorly integrated acquisitions defocused and overcomplicated the organization,” it concludes. “The company’s high cost structure and lack of financial discipline eventually led to financial ratios that were among the worst in the industry.”

The company also made a series of poor product-related decisions in the same period, including deepening its focus on the declining market for land-line technology and in the increasingly competitive optical market, while missing opportunities in the exploding wireless technology market, where it once had an early lead.

The researchers also concluded that Nortel made operational mistakes, including dismantling the centralized research and development platform from BNR “that was culturally and structurally optimized to create, innovate and develop telecommunications products using co-operative teams.”

From the era of John Roth’s leadership as CEO in the late 1990s onward, “it was felt by many R&D staff that management rarely listened to the engineers and that, when they did, they did not appear to understand.”

In the same era, Nortel gave more power to individual business teams, “which resulted in increased internal politics and fruitless competition.”

The report also says Nortel could have solved its problems in 2002 by retrenching and selling business units, but missed the opportunity, and again missed an opportunity in 2005 and 2006 to sell units and retrench in key business sectors.

“As difficult as it is to consciously reduce the size of a business by selling units, this study concludes that, in the case of Nortel, this option may have been the best and only alternative.

As if to underscore my previous posts on the extraordinary rapidity of disruptive change for the utility industry, This is turning out to be potentially more significant than the smart mobile phone revolution. Issues here include the utility industry’s failure to recognize a strategic change caused by disruptive technological change, and to respond to it, and the rapid acceleration in Adizes’ corporate life cycle model. Citibank is now predicting severe consequences for utility companies if they do not grasp the massive changes confronting them.

Industry Analysis

Citibank: Utilities are dinosaurs waiting to die

As if to underscore my previous posts on the extraordinary rapidity of disruptive change for the utility industry, This is turning out to be potentially more significant than the smart mobile phone revolution. Issues here include the utility industry’s failure to recognize a strategic inflection point caused by disruptive technological change, and to respond to it, and the rapid acceleration of the Adizes’ corporate life cycle model, as is now occurring routinely in the high tech industry: Blackberry for example.

Citibank is now predicting severe consequences for utility companies if they do not grasp the massive changes confronting them. My fear, is that the traditional mindset of these companies is like that of the telecommunication companies in the face of the mobile and Internet onslaught. The telecom carriers reaction was dismissive and disdain. The current reactionary behavior of the energy utilities is foreshadowing the same sorry saga.

Tony Seba, MGMT 450 Guest Lecturer and Stanford University Lecturer on Entrepreneurship, will be discussing this topic tomorrow, Thursday, October 10th, at 2:30PM in EME 2181.

Quick Take: A new report authored by prominent Citibank analysts claims the global energy mix is shifting more rapidly than realized. If true – and these are some smart, smart people – it has major implications for generators, consumers, and most of all utilities. In fact, the study says utilities are most at risk because their business model is likely to change.

I’ve been arguing for years that utilities should either evolve to become “wires only” companies. Or else get busy offering additional services, such as rooftop solar and microgrids. For instance, in my “Electronomics” series, I explained why utilities MUST change their business model (and one way to get started).

This Citibank report suggests that the problem is even more urgent than we realized.

Today’s electric power utilities could lose half their addressable market to energy efficiency, solar and storage, and other distributed generation, according to “Energy Darwinism – the evolution of the energy industry,” a new report from the investment banking arm of Citibank.

“Consumers face economically viable choices and alternatives in the coming years which were not foreseen 5 years ago,” the analysts write. According to REneweconomy, the price fall of solar panels has exceeded all expectations, resulting in cost parity being achieved in certain areas much more quickly. “The key point about the future is that these fast ‘learning rates’ are likely to continue, meaning that the technology just keeps getting cheaper. At the same time, the alternatives of conventional fossil fuels are likely to gradually become more expensive.”

This is not a ‘tomorrow’ story. We are already seeing utilities altering investment plans, even in the shale-driven U.S., with examples of utilities switching plans for peak-shaving gas plants, and installing solar farms in their stead,” the report says.Even wind may cut into traditional approaches, despite its intermittency. Citi says that while wind’s intermittency is an issue, with more widespread national adoption it begins to exhibit more baseload characteristics (i.e. it runs more continuously on an aggregated basis). “Hence it becomes a viable option, without the risk of low utilisation rates in developed markets, commodity price risk or associated cost of carbon risks.”

Citi admits that storage is still a nascent industry, but so was solar 5 to 6 years ago. “The increasing levels of investment and the emergence of subsidy schemes which drive volumes could lead to similarly dramatic reductions in cost as those seen in solar, which would then drive the virtuous circle of improving economics and volume adoption.”

How fast will the changeover take place? Citi says history tells us that such changes are never gradual, citing the graph below as evidence.

In his book, Only The Paranoid Survive, Andy Grove, former CEO and Chairman of Intel describes a “strategic inflection point” as being similar to the situation when a hiker on a trail suddenly realizes he is lost. The hiker doesn’t know when he became lost, but something has changed.

The concept of strategic inflection points is perhaps Grove’s most important contribution to high tech management. I believe that this is because of the lightning speed of change and events in high tech markets like semiconductors. Then there is the sheer volume of information flying by, and the need to be able to discern what’s important from all of it.

In the early 1980’s the Japanese began a coordinated global campaign to displace Intel’s dominance in semiconductor memory. The Japanese industry effort was coordinated by MITI, the government ministry of industry. My Intel counterpart in Finland was reporting that the Japanese semiconductor reps were working directly from the Japanese Consulate in Helsinki. At Intel’s technical center in Tokyo, Intel engineers were besieged with claims of Intel chip performance anomalies, requiring that Intel share complex testing results, known as “schmoo plots,” after the Rube Goldberg cartoon strip. Increasingly this appeared to be a coordinated effort at “reverse engineering.” The Japanese also appeared to be engaging in an elaborate global pricing scheme designed to confound Intel in markets outside the continental US.

Simultaneously, I became a member of the hand-picked Intel Memory Components Marketing team, just as we relocated the division from California to Oregon. At the direction of Ed Gelbach, senior Intel Marketing VP, and Andy, we quickly formed into an elite group of Ivy League MBA’s and Intel veterans to attack this Japanese challenge to Intel. At about the same time, the Japanese challenge so disturbed US government officials that an arranged investment marriage was executed with IBM taking a 15% minority stake in Intel to send a message to the Japanese. The strategic situation was seen as dire. For a number of years the elite Memory Components Marketing group succeeded in achieving miracles, and confounded the Japanese. The global Intel Sales organization, repeatedly voted us the #1 marketing group at Intel, though we brought them less commission than other divisions. Barry Cox, Scott Gibson, Frank Costa (my housemate), Bill Howe, Roy Coppinger, Larry Gordon, Nick Stier, Craig Brooksby, Ray Rund and many others made the difference. I should also give a nod to Tim Sweeney, who is the true “Intel alumni” who preceded those of us who followed him to Intel’s European organization.

Grove has not revealed much about this time, and the internal Intel effort to combat the Japanese, before he and Gordon Moore finally decided to exit the memory business, as a “strategic inflection point.” NPR recently broadcast an interview with both Gordon and Andy that did not touch on Intel’s efforts to confront the Japanese.

A key factor in this global battle, was the traditional belief that new leading edge semiconductor manufacturing processes needed to be “proved out,” in high volume memory production, before moving the most advanced microprocessor designs onto the new process.

The first strategic inflection point at Intel occurred when Gordon and Andy famously made the decision to end the memory business. They concluded that high volume memory production was not required to “prove” semiconductor manufacturing processes before putting microprocessors into production, and that Intel could safely exit the memory business, and remain highly competitive.