For the last few years, I have been invited to speak with graduating classes of university engineering students. I call my lecture “Engineer to Entrepreneur.” From my background in teaching management and entrepreneurial mentorship, I focus on the unique challenges engineers face in entering the business world, particularly those who may consider starting their own new business. I discuss a full range of issues, but my personal emphasis from my experience is the “character” issue. Some excellent engineers have successfully made the transition to entrepreneurship and executive management, but for others, the Odyssey is a bridge too far. Engineers must learn to think differently than when they are solving an engineering problem. Consequently, I place significant emphasis on honest self-analysis and appreciation of one’s strengths and weaknesses. Listening is a priceless skill. If you have experienced Google’s Larry Page in public, he is an excellent example of an engineer who has very successfully transitioned into a senior management role. Sergei Brin, on the other hand, opted for a CTO-like role, which I think was the right choice for him. That is the point of my lecture. I hope that many who view my YouTube Channel will find it helpful. You can find the complete lecture on my website.

Remember that my website, mayo615.com has over 400 posts on a wide range of management and technology topics.

The concept of a Total Product or Complete Product is essential to product success, particularly in an emerging new company. This concept was pioneered by Harvard Business School professor Ted Levitt and later updated and adapted to the high technology industry by a group of us at Intel.

The concept of a Total Product or Complete Product is essential to product success, particularly in an emerging new company. This concept was pioneered by Harvard Business School professor Ted Levitt and later updated and adapted to the high technology industry by a group of us at Intel. Engineers commonly believe that when their product development is finished, the product is ready for market. Nothing could be further from the truth. The engineering “deliverable” is not a product. It must be surrounded by a number of other intangible value items before it is a Complete Product. In Levitt’s model, these items are the augmented product, the expected product, and the potential product. The Intel variant, shown here, is more detailed but essentially very similar.

This is yet another excellent article questioning the Canadian tech industry’s appreciation of its significant deficiencies and challenges. It reflects my own view after much research and many interviews. It is also the view of UoT Professor Richard Florida who published a similar article in the Globe & Mail recently. Venture capital is anemic, but many also believe that there is a lack of scale-up management talent. Another factor is deeply-embedded Canadian conservatism, as evidenced by the bizarre entry of high street banks’ debt offerings to entrepreneurs.

Canadian Tech Industry Still Not Confronting Its Infrastructure Issues

This is yet another excellent article questioning the Canadian tech industry’s appreciation of its significant deficiencies and challenges. It reflects my own view after much research and many interviews. It is also the view of UoT Professor Richard Florida who published a similar article in the Globe & Mail recently. Venture capital is anemic, but many also believe that there is a lack of scale-up management talent. Another factor is deeply-embedded Canadian conservatism, as evidenced by the bizarre entry of high street commercial banks’ debt offerings to entrepreneurs.

CANADIAN TECH NEEDS TO REDEFINE ITS SENSE OF SCALE/BetaKit

If like me, you spend a lot of time poring over the latest in Canadian tech, chances are good that you see both the huge potential of our technology companies and the simultaneous challenge: too often, they’re being held back by Canada’s scale-up deficit.

This, of course, isn’t news. In all the years I’ve participated in this sector, it’s been an ongoing challenge—one that has been the topic of countless discussions, panels, and debates. It’s an issue that has long challenged our innovation and technology sectors, and though it’s been talked about at length, it’s a conversation that deserves our full attention until we get it right.

Canada has become a launch-pad for early-stage companies, but, with a few notable exceptions, we are largely still lacking later-stage success stories.

PwC Canada’s recent MoneyTree report shows that our technology sector has seen a significant increase in funding deal volume in the last year—up 30 percent from 2017. But when one reads between the lines, it’s also clear that our homegrown tech companies are still largely stuck in a middle ground. In fact, of all the companies raising seed or early-stage funding during 2015-2017, only roughly 10 percent of them raised expansion or later-stage funding during 2016-2018.

Even if we leave room for successful shops that don’t need to raise further VC, that still doesn’t account for all of it. Many stall, naturally. They don’t continue to climb the curve and thereby miss the opportunity to hit scale. Of course, some companies shouldn’t scale and falter for good reasons. But many should and, for one reason or another, don’t. As a result, it seems that Canada has become a launch-pad for early-stage companies, but, with a few notable exceptions, we are largely still lacking the later-stage success stories we see in many other ecosystems.

Addressing this begins with challenging our very definition of scale. When we talk about Canada’s scale-up dilemma, we tend to focus on the obvious: raising capital, multiplying sales, and increasing market share in large, global, addressable markets. All of this is important but, in my experience, it’s only a part of the equation. Whether founders are on their first venture or their fifth, early-stage companies face many challenges to growth, and mature technology ecosystems support them by ensuring they see the bigger picture, beyond raising capital and increasing sales. It’s time to redefine our collective understanding of what scale means, and arrive at a new recipe that touches on all the moving parts companies need to master if they’re going to level-up.

To redefine scale, we need to take a closer look at the state of our ecosystems, which can become global hubs for highly skilled digital, creative, and leadership talent, and at the roadblocks that are currently preventing companies from scaling up. Let’s start by looking to the key stakeholders who will inevitably play an important role in shaping the future of the tech sector, including our government, VCs, and the public and private sector buyers of technology.

Government, of course, has several levers to pull when it comes to helping companies scale, like shaping policies and regulations that work to benefit our technology sector, while ensuring tax dollars are well spent through targeted incentive programs matched with data and IP policies that achieve the right balance.

Government(s) of all levels need to re-commit to working with Canadian technology companies at all stages of their evolution. They need to commit to procurement policies and practices that produce a real and predictable market for our tech companies to address and sell into. Federal and provincial governments of all stripes have made promises in this regard, but the velocity of, and commitment to, local sourcing hasn’t yet translated for our entrepreneurs.

Our government can also work to modernize our federal and provincial processes that foster the development and retention of IP, and continue to evolve tax incentives that support later-stage companies. These improvements would also encourage greater global investment in the Canadian ecosystem. According to the World Economic Forum Executive Opinion Survey, two of the most problematic factors of doing business in Canada are inefficient government bureaucracy and tax rates.

Data regulations and privacy policies, too, are of particular focus for governments worldwide. Ours can help us ensure that Canadian technology shops want to stay here, to do their important work, while being intentional about our data protection policies. After all, scaling does not mean scaling by any means, and protecting our data sovereignty is important.

Beyond government support, we should also look to VCs and other sources of private capital to enable companies to scale. Here, we often turn to Silicon Valley for inspiration, as investors there tend to be more willing to place big bets and write big cheques. Canada can learn from this. Any investor is going to have more misses than hits and, without higher risk tolerance, we won’t be able to finance the technological sophistication that will propel us to the next level.

According to the 2019 Canadian Startup Outlook Report, 56 percent of companies state that their long-term goal is to be acquired.

There is good news for Canada: CPPIB recently announced investments of $1 billion in venture funds, much of which will focus on technology companies. I’d love to see our wider investment community follow their lead. Funds like Novacap, Georgian Partners, OMERS Ventures, and more occupy the unique position of helping shape the future of Canada’s innovation economy. They’re already investing in some great home-grown companies, and their continued willingness to take bigger risks on innovative, growth-stage companies will help create the culture we need.

There’s even more good news when it comes to talent in Canada: we’re well positioned to become a hub for top tech and innovation talent. Our immigration policies, like BC’s Provincial Nominee Program and the federal Global Skills Strategy, are helping to draw the global talent stream north; our colleges, universities, and research hubs are world-renowned. Still, as I’ve seen with the corporate boards and senior leadership teams I’ve been involved with, companies need seasoned global talent if they want to become truly global players. It’s time we cast a wider net, finding ways to incentivize governance and executive talent from technology hubs like Boston, New York, Shenzhen, Dublin, Tel Aviv, and beyond to help Canadian companies reach their next stage and deliver on the promise of scale.

Established Canadian corporates have a big role to play here too. While our market is small by comparison to our neighbour, there is big buying power in our financial services, energy, retail, healthcare, automotive, and other major industries. Without a hint of protectionism, we can look to the Canadian innovation and technology markets each and every time we are procuring a solution, looking for new technologies or even looking for a problem to solve. In fact, according to the 2019 PwC annual CEO survey, 52 percent of Canadian CEOs surveyed see collaboration with start-up entrepreneurs as a key growth strategy.

Another way for companies to level-up and scale quickly is to reconsider some elements of the growth strategy playbook. Not surprisingly, according to the 2019 Canadian Startup Outlook Report by Silicon Valley Bank, 56 percent of companies state that their long-term goal is to be acquired. However, we should consider a shift in mindset that focuses on growth by acquisition rather than looking primarily at exit strategies or organic growth. This approach works well in dynamic sectors like fintech and healthcare. I’ve seen companies enjoy success by expanding into international markets or adjacent spaces, growing horizontally through acquisitions. Our tech leaders need to be thinking long-term so that, whether they’re building to grow, to expand, or to sell, they have the right structures and systems in place.

I am hopeful that these thoughts are provocative and assist some in considering strategies and actions that will lead to the scale Canada needs. True scale is critical if we want our technology companies to drive our GDP, provide high-paying jobs, and spur the innovations that will elevate us on the world stage.

This article was originally published on LinkedIn. Photo courtesy @dingle.

I want to talk a bit about networking with new acquaintances or renewing old contacts. Networking is often dreaded because it sounds like being disingenuous or insincere. Good networking is genuine and sincere. I made the point in Week 1 that communication skills are crucial, and they can be learned. Warren Buffett has said that “public speaking” is the most important skill he ever learned. So let’s discuss a few ideas on how to make networking less stressful and more successful. In this video, I will list three key things to remember when networking and expand on why they are so important. My UBC Management students will remember this from my Management Communication course.

Welcome to a bonus Week 2 Update of Mayo615’s Odyssey to France.

I want to talk a bit about networking with new acquaintances or renewing old contacts. Networking is often dreaded because it sounds like being disingenuous or insincere. Good networking is genuine and sincere. I made the point in Week 1 that communication skills are crucial, and they can be learned. Warren Buffett has said that “public speaking” is the most important skill he ever learned. So let’s discuss a few ideas on how to make networking less stressful and more successful. In this video, I will list three key things to remember when networking and expand on why they are so important. My UBC Management students will remember this from my Management Communication course.

Welcome to Mayo615’s Odyssey to France and the first of our Tuesday weekly updates. We invite you to subscribe to our YouTube Channel and follow our weekly updates. In this Week One update we will focus on my first Big Idea, and how I achieved it. I will also discuss my three most important key takeaways from that experience. We hope that you find this video helpful in achieving your own Big Ideas and goals. So here we go.

Welcome to Mayo615’s Odyssey to France and the first of our Tuesday weekly updates

We invite you to subscribe to our YouTube Channel and to follow our weekly updates

In this Week One update we will focus on my first Big Idea, and how I achieved it. I will also discuss my three most important key takeaways from that experience. We hope that you find this video helpful in achieving your own Big Ideas and goals. So here we go.

On this YouTube Channel, we will share our Big Idea: our personal goal and invite you to participate with us, share your comments and questions and perhaps motivate you to achieve your own Big Idea. We will post an update on our project every Tuesday. We invite your comments and questions about your own Big Idea while you follow ours. We will both reply to all comments and will feature the best questions in our YouTube update videos each week. So click SUBSCRIBE and let’s get started!

The launch of the Mayo615 YouTube Channel Trailer

On this YouTube Channel, we will share our Big Idea: our personal goal and invite you to participate with us, share your comments and questions and perhaps motivate you to achieve your own Big Idea. We will post an update on our project every Tuesday. We invite your comments and questions about your own Big Idea while you follow ours. We will both reply to all comments and will feature the best questions in our YouTube update videos each week.

I want to return to France to give back my experience, skills, and technical knowledge to the country of my heritage. France’s industrial economy is in the doldrums, but new policies are stimulating innovation, the key to economic growth and productivity, and technology industry leaders in France with strong technology industry backgrounds are looking to contribute to this new economy in France. I want to join them and give back.

In less than 24 hours since our campaign launch, we are nearing 10% of our goal

I am a native-born Californian with French family heritage and a French wife. We are both French citizens preparing to return to France. My university background is in the Humanities and Social Sciences, with a year of graduate study at Oxford University, researching in the Bodleian Library. When I returned to northern California, I eventually landed an entry-level job at Intel Corporation, which proved to be the crucible for my entire career. I eventually rose to be a senior executive in international business development with Intel. I have continued in international business for all of my career, working for a number of tech startups and venture capital investment firms over the years. I have led two tech industry consortia to develop global industry standards. I have been the director of a tech entrepreneurial incubator in Silicon Valley for the government of New Zealand and collaborated on mentoring promising entrepreneurs in locations here and around the world. I was an Adjunct Professor of Management at the University of British Columbia for four years.

I want to return to France to give back my experience, skills, and technical knowledge to the country of my heritage. France’s industrial economy is in the doldrums, but new policies are stimulating innovation, the key to economic growth and productivity, and technology industry leaders in France with strong technology industry backgrounds are looking to contribute to this new economy in France. I want to join them and give back.

I am now semi-retired, but very eager to return permanently to France to donate my technology industry experience and knowledge to assist French entrepreneurs to transform France into an innovation-based economy.

FundRazr Campaign Story:

We are David Mayes and Isabelle Roux-Mayes, a married couple, who are also French citizens. I am also a native Californian who has spent my career working for a number of Silicon Valley companies and investment firms, beginning with Intel Corporation. I am now semi-retired, but very eager to return permanently to France to donate my technology industry experience and knowledge to assist French entrepreneurs to transform France into an innovation-based economy. I am focusing specifically on building working relationships with three major new initiatives that could benefit from my background and achievements: The Camp in Aix-en-Provence, launched last year, Startup Garage, Paris, and 1kubator in Bourdeaux.

I am more than happy to share my achievements and references to validate my credentials and verify my ability to make a serious contribution. You can start here with my LinkedIn profile and references David Mayes on LinkedIn. You may also contact me here or on FundRazr where we can discuss my crowdfunding project.

Five years ago, I wrote a post on this blog disparaging the state of the Internet of Things/home automation market as a “Tower of Proprietary Babble.” Vendors of many different home and industrial product offerings were literally speaking different languages, making their products inoperable with other complementary products from other vendors. The market was being constrained by its immaturity and a failure to grasp the importance of open standards. A 2017 Verizon report concluded that “an absence of industry-wide standards…represented greater than 50% of executives concerns about IoT. Today I can report that finally, the solutions and technologies are beginning to come together, albeit still slowly.

The Evolution of These Technologies Is Clearer

The IoT Tower of Proprietary Babble Is Slowly Crumbling

The Rise of the Intelligent Assistant

Five years ago, I wrote a post on this blog disparaging the state of the Internet of Things/home automation market as a “Tower of Proprietary Babble.” Vendors of many different home and industrial product offerings were literally speaking different languages, making their products inoperable with other complementary products from other vendors. The market was being constrained by its immaturity and a failure to grasp the importance of open standards. A 2017 Verizon report concluded that “an absence of industry-wide standards…represented greater than 50% of executives concerns about IoT.” Today I can report that finally, the solutions and technologies are beginning to come together, albeit still slowly.

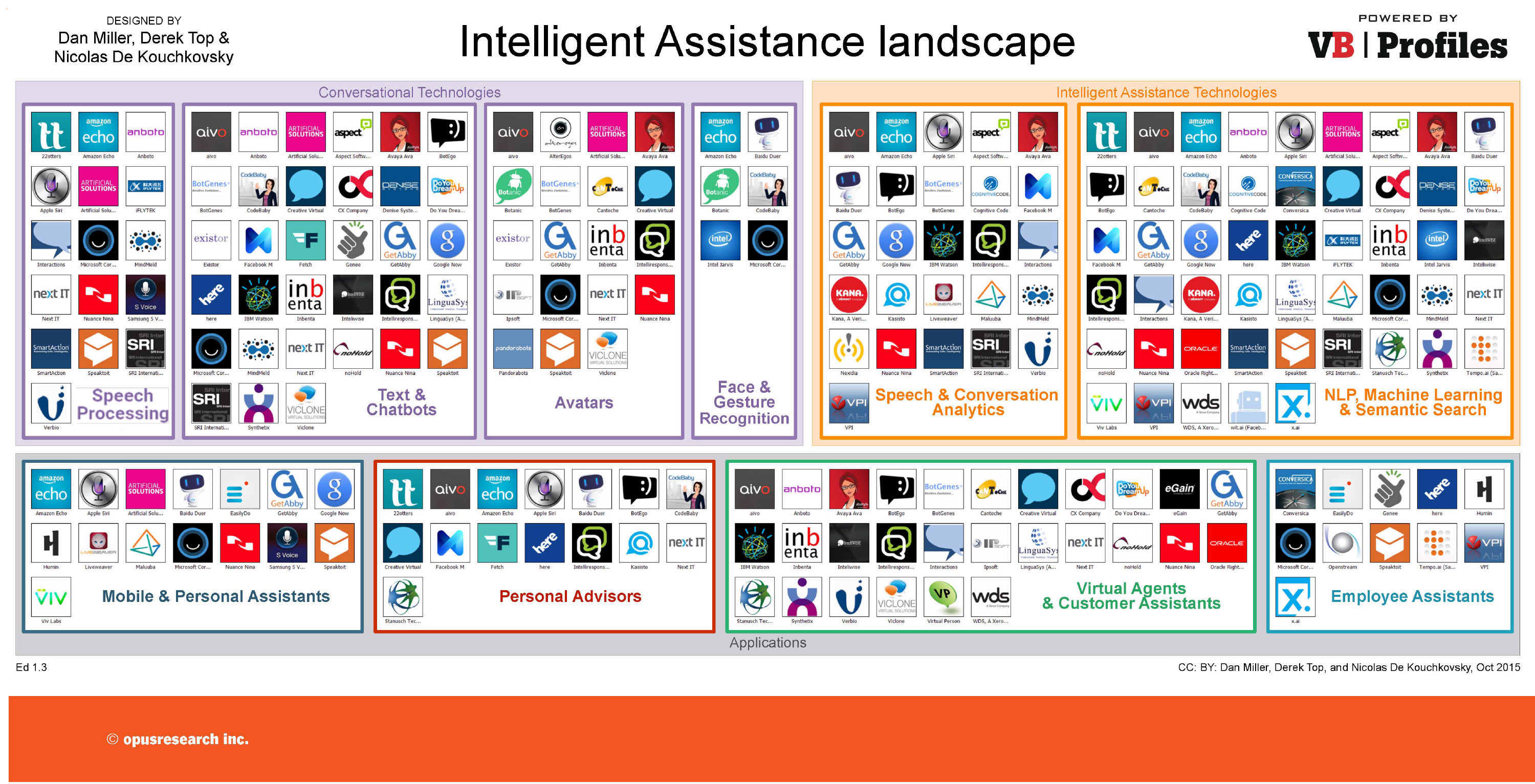

One of the most important factors influencing these positive developments has been the recognition of the importance of this technology area by major corporate players and a large number of entrepreneurial companies funded by venture investment, as shown in the infographic above. Amazon, for example, announced in October 2018 that it has shipped over 100 Million Echo devices, which effectively combine an intelligent assistant, smart hub, and a large-scale database of information. This does not take into account the dozens of other companies which have launched their own entries. I like to point to Philips Hue as such an example of corporate strategic focus perhaps changing the future corporate prospects of Philips, based in Eindhoven in the Netherlands. I have visited Philips HQ, a company trying to evolve from the incandescent lighting market. Two years ago my wife bought me a Philips Hue WiFi controlled smart lighting starter kit. My initial reaction was disbelief that it would succeed. I am eating crow on that point, as I now control my lighting using Amazon’s Alexa and the Philips Hue smart hub. The rise of the “intelligent assistant” seems to have been a catalyst for growth and convergence.

The situation with proprietary silos of offerings that do not work well or at all with other offerings is still frustrating, but slowly evolving. Amazon Firestick’s browser is its own awkward “Silk” or alternatively Firefox, but excluding Google’s Chrome for alleged competitive advantage. When I set up my Firestick, I had to ditch Chromecast because I only have so many HDMI ports. Alexa works with Spotify but only in one room as dictated by Spotify. Alexa can play music from Amazon Music or Sirius/XM on all Echo devices without the Spotify limitation. Which brings me to another point of aggravation: alleged Smart TV’s. Not only are they not truly “smart,” they are proprietary silos of their own, so “intelligent assistant” smart hubs do not work with “smart” TV’s. Samsung, for example, has its own competing intelligent assistant, Bixby, so of course, only Bixby can control a Samsung TV. I watched one of those YouTube DIY videos on how you could make your TV work with Alexa using third-party software and remotes. Trust me, you do not want to go there. But cracks are beginning to appear that may lead to a flood of openness. Samsung just announced at CES that beginning in 2019 its Smart TV’s will work with Amazon Echo and Google Home, and that a later software update will likely enable older Samsung TV’s to work with Echo and Home. However, Bixby will still control the remote. Other TV’s from manufacturers like Sony and LG have worked with intelligent assistants for some time.

The rise of an Internet of Everything Everywhere, the recognition of the need for greater data communication bandwidth, and battery-free wireless IoT sensors are heating up R&D labs everywhere. Keep in mind that I am focusing on the consumer side, and have not even mentioned the rising demands from industrial applications. Intel has estimated that autonomous vehicles will transmit up to 4 Terabytes of data daily. AR and VR applications will require similar throughput. Existing wireless data communication technologies, including 5G LTE, cannot address this need. In addition, an exploding need for IoT sensors not connected to an electrical power source will require more work in the area of “energy harvesting.” Energy harvesting began with passive RFID, and by using kinetic, pizeo, and thermoelectric energy and converting it into a battery-free electrical power source for sensors. EnOcean, an entrepreneurial spinoff of Siemens in Munich has pioneered this technology but it is not sufficient for future market requirements.

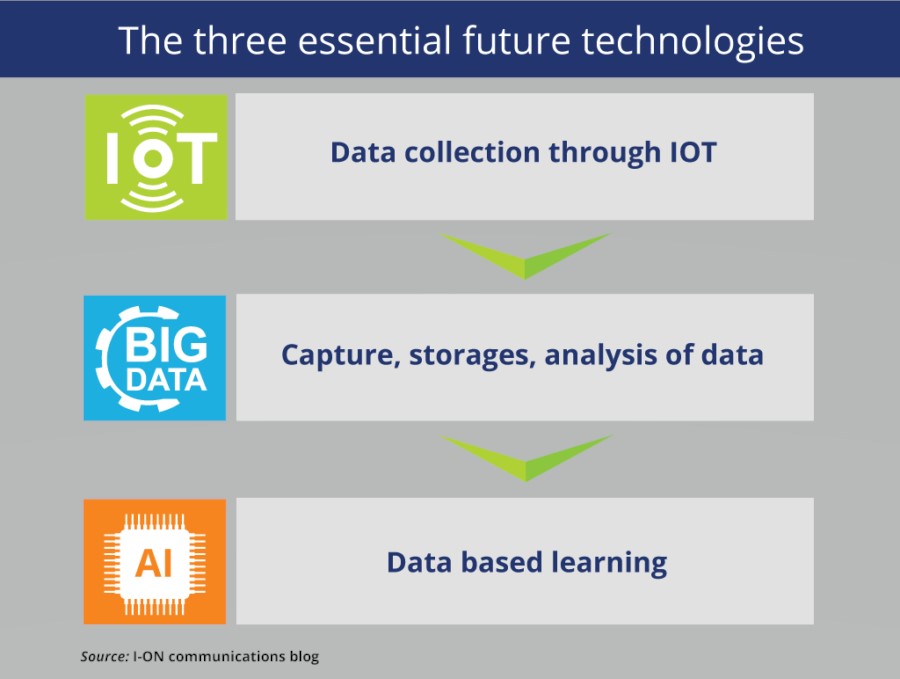

Fortunately, work has already begun on both higher throughput wireless data communication using mmWave spectrum, and energy harvesting using radio backscatter, reminiscent of Nikola Tesla’s dream of wireless electrical power distribution. The successful demonstration of these technologies holds the potential to open the door to new IEEE data communication standards that could potentially play a role in ending the Tower of Babble and accelerating the integration of AI, IoT, and Big Data. Bottom line is that the market and the technology landscape are improving.

My IEEE Talk from 2013 foreshadows the development of current emerging trends in advanced technology, as they appeared at the time. I proposed that in fact, they represent one huge integrated convergence trend that has morphed into something even bigger, and is already having a major impact on the way we live, work, and think. The 2012 Obama campaign’s sophisticated “Dashboard” application is referenced, integrating Big Data, The Cloud, and Smart Mobile was perhaps the most significant example at that time of the combined power of these trends blending into one big thing.

READ MORE: Blog Post on IoT from July 20, 2013

The term “Internet of Things” (IoT) is being loosely tossed around in the media. But what does it mean? It means simply that data communication, like Internet communication, but not necessarily Internet Protocol packets, is emerging for all manner of “things” in the home, in your car, everywhere: light switches, lighting devices, thermostats, door locks, window shades, kitchen appliances, washers & dryers, home audio and video equipment, even pet food dispensers. You get the idea. It has also been called home automation. All of this communication occurs autonomously, without human intervention. The communication can be between and among these devices, so-called machine to machine or M2M communication. The data communication can also terminate in a compute server where the information can be acted on automatically, or made available to the user to intervene remotely from their smart mobile phone or any other remote Internet-connected device.

Another key concept is the promise of automated energy efficiency, with the introduction of “smart meters” with data communication capability, and also achieved in large commercial structures via the Leadership in Energy & Environmental Design program or LEED. Some may recall that when Bill Gates built his multi-million dollar mansion on Lake Washington in Seattle, he had “remote control” of his home built into it. Now, years later, Gates’ original home automation is obsolete. The dream of home automation has been around for years, with numerous Silicon Valley conferences, and failed startups over the years, and needless to say, home automation went nowhere. But it is this concept of effortless home automation that has been the Holy Grail.

But this is also where the glowing promise of The Internet of Things (IoT) begins to morph into a giant “hairball.” The term “hairball” was former Sun Microsystems CEO, Scott McNealy‘s favorite term to describe a complicated mess. In hindsight, the early euphoric days of home automation were plagued by the lack of “convergence.” I use this term to describe the inability of available technology to meet the market opportunity. Without convergence, there can be no market opportunity beyond early adopter techno geeks. Today, the convergence problem has finally been eliminated. Moore’s Law and advances in data communication have swept away the convergence problem. But for many years the home automation market was stalled.

Also, as more Internet-connected devices emerged it became apparent that these devices and apps were a hacker’s paradise. The concept of IoT was being implemented in very naive and immature ways and lacking common industry standards on basic issues: the kinds of things that the IETF and IEEE are famous for. These vulnerabilities are only now very slowly being resolved, but still in a fragmented ad hoc manner. The central problem has not been addressed due to classic proprietary “not invented here” mindsets.

The problem that is currently the center of this hairball, and from all indications is not likely to be resolved anytime soon. It is the problem of multiple data communication protocols, many of them effectively proprietary, creating a huge incompatible Tower of Babbling Things. There is no meaningful industry and market wide consensus on how The Internet of Things should communicate with the rest of the Internet. Until this happens, there can be no fulfillment of the promise of The Internet of Things. I recently posted “Co-opetition: Open Standards Always Win,” which discusses the need for open standards in order for a market to scale up.

A recent ZDNet post explains that home automation currently requires that devices need to be able to connect with “multiple local- and wide-area connectivity options (ZigBee, Wi-Fi, Bluetooth, GSM/GPRS, RFID/NFC, GPS, Ethernet). Along with the ability to connect many different kinds of sensors, this allows devices to be configured for a range of vertical markets.” Huh? This is the problem in a nutshell. You do not need to be a data communication engineer to get the point. And this is not even close to a full discussion of the problem. There are also IoT vendors who believe that consumers should pay them for the ability to connect to their proprietary Cloud. So imagine paying a fee for every protocol or sensor we employ in our homes. That’s a non-starter.

The above laundry list of data communication protocols, does not include the Zigbee “smart meter” communications standards war. The Zigbee protocol has been around for years, and claims to be an open industry standard, but many do not agree. Zigbee still does not really work, and a new competing smart meter protocol has just entered the picture. The Bluetooth IEEE 802.15 standard now may be overtaken by a much more powerful 802.15 3a. Some are asking if 4G LTE, NFC or WiFi may eliminate Bluetooth altogether. A very cool new technology, energy harvesting, has begun to take off in the home automation market. The energy harvesting sensors (no batteries) can capture just enough kinetic, peizo or thermoelectric energy to transmit short data communication “telegrams” to an energy harvesting router or server. The EnOcean Alliance has been formed around a small German company spun off from Siemens, and has attracted many leading companies in building automation. But EnOcean itself has recently published an article in Electronic Design News, announcing that they have a created “middleware” (quote) “…to incorporate battery-less devices into networks based on several different communication standards such as Wi-Fi, GSM, Ethernet/IP, BACnet, LON, KNX or DALI.” (unquote). It is apparent that this space remains very confused, crowded and uncertain. A new Cambridge UK startup, Neul is proposing yet another new IoT approach using the radio spectrum known as “white space,” becoming available with the transition from analog to digital television. With this much contention on protocols, there will be nothing but market paralysis.

Is everyone following all of these acronyms and data comm protocols? There will be a short quiz at the end of this post. (smile)

The advent of IP version 6, strongly supported by Intel and Cisco Systems has created another area of confusion. The problem with IPv6 in the world of The IoT is “too much information” as we say. Cisco and Intel want to see IPv6 as the one global protocol for every Internet connected device. This is utterly incompatible with energy harvesting, as the tiny amount of harvested energy cannot transmit the very long IPv6 packets. Hence, EnOcean’s middleware, without which their market is essentially constrained.

The Brave New World of Internet privacy issues relating to this tidal wave of Big Data are not even considered here, and deserve a separate post on the subject. A recent NBC Technology post has explored many of these issues, while some have suggested we simply need to get over it. We have no privacy.

Stakeholders in The Internet of Things seem not to have learned the repeated lesson of open standards and co-opetition, and are concentrating on proprietary advantage which ensures that this market will not effectively scale anytime in the foreseeable future. Intertwined with the Tower of Babbling Things are the problems of Internet privacy and consumer concerns about wireless communication health & safety issues. Taken together, this market is not ready for prime time.

At its inception, Uber touted itself as a shining example of the “sharing economy” described by Jeremy Rifkin, in this now famous book, The Third Industrial Revolution. As time has passed the reality has been radically at odds with a sharing economy. Among the many issues that have emerged has been the legacy of Uber’s ugly corporate culture, secret apps used to confound regulators, and to intimidate journalists, a Justice Department investigation of illegal practices, including 200 Uber employees conspiring together to attack Lyft’s operations. The proverbial chickens have come home to roost, as municipalities around the world have begun to regain control of transportation policy within their jurisdictions, and the inflated valuations of these unicorns begin to deflate.

Regulating Ride-Sharing: New York May Be The Model For The Future

Writing On The Wall: London and Vancouver Moving In A Similar Direction

At its inception, Uber touted itself as a shining example of the “sharing economy” described by Jeremy Rifkin, in this now famous book, The Third Industrial Revolution. As time has passed the reality has been radically at odds with a sharing economy. Among the many issues that have emerged has been the legacy of Uber’s ugly corporate culture, secret apps used to confound regulators, and to intimidate journalists, a Justice Department investigation of illegal practices, including 200 Uber employees conspiring together to attack Lyft’s operations. The proverbial chickens have come home to roost, as municipalities around the world have begun to regain control of transportation policy within their jurisdictions, and the inflated valuations of these unicorns begin to deflate.

From the Wharton Newsletter/Podcast, August 14, 2018

The largest market for Uber, Lyft and other ride-hailing app companies — New York City — last week had its first successful attempt at regulating the growth of the nascent industry. On Wednesday, the New York City Council passed a series of bills, notably one that places a one-year moratorium on the issue of new for-hire vehicle (FHV) licenses. Other bills establish minimum wage levels for ride-hailing service drivers; require FHVs to submit data on ridership with penalties for failure to do so; and create driver-assistance centers to provide counseling services.

New York City had little option to act, especially after a similar move by Mayor Bill de Blasio fell apart following intense lobbying by Uber. Increasing road congestion by cars was the biggest contributing factor to the passage of the bill capping new licenses, corroborated by a decline in subway ridership. The number of FHVs in the city had grown from 65,000 in 2015 to about 130,000 currently. Uber is the biggest gainer, as shown by its almost hockey-stick growth in ridership.

New York City took the right steps to regulate the FHV industry, according to Wharton professor of operations, information and decisions Senthil Veeraraghavan. “This is the right way to go,” he said. “This is a great experiment that we’re [witnessing].”

“They had to do something,” noted Wharton management professor John R. Kimberly. “This is part of an obviously much deeper story … and the timing seems to be right.”

The move to ensure that drivers receive a minimum pay of $15 an hour after they cover expenses is also significant, said James Parrott, director of economic and fiscal policies at the New School’s Center for New York City Affairs. He had worked on an extensive study for the city’s Taxi and Limousine Commission that looked at the ride-hailing sector and its growth, and in particular its impact on driver earnings.

Kimberly, Veeraraghavan and Parrott discussed the implications of the legislative actions governing New York City’s for-hire vehicle industry on the Knowledge@Wharton radio show on SiriusXM. (Listen to the podcast at the top of this page.)

“This is the right way to go. This is a great experiment that we’re [witnessing].”–Senthil Veeraraghavan

Incentive to Improve

The establishment of a minimum pay for drivers is an important incentive for ride-hailing app companies to increase the utilization of drivers’ time, said Parrott. Drivers currently have a passenger in the car for only about 36 minutes of every hour, which means they don’t have a paying passenger for 42% of their time, he added.

Up to now, Uber’s business model has been “to flood the streets with cars,” since the firm gets a commission based on every fare, Parrott said. “There’s been no incentive for them to better utilize the drivers’ capital,” he added. “Keep in mind; this is an industry where the capital investment in the rolling stock – the cars – is entirely put up by the drivers. The pay standard gives them an incentive by allowing them to pay a little bit less if they make better utilization of the drivers’ time.”

The city will use the year ahead to study congestion levels in the city and find ways to redress that, including through congestion pricing mechanisms. Last week’s actions took a step in that direction with a surcharge on cabs below 96th Street ($2 per ride for medallion trips and $2.75 for ride-hailing app cabs). It will also allow the city to monitor how the pay standard works out, and how the ride-hailing app companies make better utilization of drivers’ time, Parrott said.

“Even if you increase utilization by 10 percentage points – from 58% to 68% – you would only increase average wait times across the city about 20 to 30 seconds,” said Parrott, citing his study’s findings. “We sense that most people can live with that.”

According to Parrott, the number of Uber trips in the city increased 100% in 2016 and 70% in 2017. Going forward, he said that figure could probably grow another 40% over the next year, “even without any additional cars on the street – just from increased efficiency.” Those increased efficiencies could come from a variety of quarters, including urging part-time drivers to go full-time and recruiting some of the drivers from the non-app services, such as the traditional livery car segment that has no minimum pay standards.

“Uber and the drivers are on both sides of the story,” noted Veeraraghavan. Riders want low waiting times, which can be achieved with more vehicles. But drivers want fewer drivers, because that would allow them to get better pricing, he said.

“Granted it might have been done a lot sooner, but it seems to me that at least in the city of New York there’s a real, serious effort to get their arms around the problem.”–John Kimberly

Worsening Congestion

Parrott said New York City had first started talking about capping Uber and Lyft cars in 2015, drawing “heavy pushback” from the ride-hailing industry at that point. Between then and now, the number of trips using ride-hailing apps has skyrocketed to 600,000 a day, which is more than five times the level in 2015, he noted. A 2016 study by the mayor’s office proposed several remedial measures including those to reduce congestion, improve air quality, protect drivers’ interests and enhance passenger experiences.

Parrott said that while the city bears some responsibility for not acting sooner on the unbridled growth of the FHV industry, it faced a different climate when it attempted that in mid-2015. Uber at the time controlled 90% of the market in the city as opposed to 66% now, he pointed out. Suicides by six cab driversalso highlighted the “economic crisis” and changed public opinion in favor of the changes, he said.

“Theoretically speaking, there’s always a gap between what firms will want to optimize and what society wants to optimize,” said Veeraraghavan. “And it’s hard for individuals to see what’s optimal for this society.” However, as city residents have begun seeing the impact of the FHV industry’s growth — including on public transportation ridership numbers — they now have had a better understanding. “So we have a redo from 2015 to 2017 … and we’re seeing better support for this.”

“Granted, it might have been done a lot sooner, but it seems to me that at least in the city of New York there’s a real, serious effort to get their arms around the problem and to figure out how to solve it,” said Kimberly.

Congestion in New York City has worsened in recent years with not just the influx of cabs, but also other vehicles “providing instant service for a variety of needs that people believe they have,” including delivery vehicles, said Kimberly. “The density of tourists on the sidewalks is so great it spills over into the street – that slows down traffic and makes it hard for cars,” he added. The option of levying congestion pricing is being seriously considered also at the state headquarters in Albany, he noted.

At the same time, “the growth of FHVs has meant that there’s much better transportation access in the outer boroughs, so the city doesn’t want to diminish that newly available service,” said Kimberly. “And yet the city also has a great interest in making sure that the drivers are able to remain economically viable to meet their expenses and to earn a decent living.” Higher wages would also enable drivers to work fewer than the 10-12 hours a day they now put in, he added, and that would have safety benefits as well.

“If they can show that they have stability and regulatory certainty in their largest market in the U.S., that will give investors a lot more certainty….”–James Parrott

Congestion pricing will also help fund investments in maintaining and upgrading the city’s aging subway and public bus system, Parrott said. The decline in mass transit ridership is not just because of the growth of the FHV industry, he noted; commuters are turning away because of “under-investment and under attention to adequately maintaining the mass transit system.”

Uber’s Leadership Challenge

The changes also highlight a “leadership challenge” for Uber, said Kimberly. “They have hundreds of markets around the globe, and each market has its own political configuration, and its own way of doing business,” he noted. “When you think about the challenges of operating an enterprise like Uber on a global basis with all the local idiosyncrasies that need to be taken into account both economically and politically, it’s a really interesting [problem].”

Uber, which is currently valued at about $62 billion, is said to be preparing for an initial public offering of its stock next year. “If they can show that they have stability and regulatory certainty in their largest market in the U.S., that will give investors a lot more certainty about the potential prospects for the company,” said Parrott.

Uber’s impact on employment is also large, Parrott noted. Uber drivers are not legally considered employees, but if they were to be treated as full-time equivalent (FTE) employees, Uber would be the largest private-sector employer in New York City, with about 35,000 FTEs, he said. “[Ride sharing] has become a huge enterprise in New York City, and it and it’s not what people usually think of as gig work where you are doing this to supplement other income. We found that 80% of the drivers bought their cars mainly for the purpose of providing transportation services, and two thirds of the drivers are full-time drivers.”

Parrott noted that both Uber and Lyft embraced the pay standard proposal. But Kimberly thought they had little option in the matter. “I don’t think it’s by accident that they’re embracing the pay standard,” he said. “Left to their own devices, they probably would not have done that. But there’s been so much social criticism – and valid criticism – of their models that they’ve really had no choice.”

Wikipedia defines Specsmanship as the inappropriate use of specifications or measurement results to establish the putative superiority of one entity over another, generally when no such superiority exists. It is commonly found in high fidelity audio equipment, automobiles and other apparatus where uneducated users identify some numerical value upon which to base their pride or derision, whether or not it is relevant to the actual use of the device. Smartphones and the early microprocessor market are also examples.

Two Specsmanship Case Studies

Most recently, we are seeing specsmanship in the smartphone market. As the smartphone market has matured into 7th, 8th, 9th generations of smartphones, the differentiation among products has been reduced to smaller and smaller differences in the products : resolution of the camera, display size or alleged brightness, etc.. In earlier generations, Apple, and the Android phone manufacturers created a highly effective intangible market need to possess their latest generation phone in which features were less important. I called this market need the smartphone “Star Wars” phenomenon causing people to line up around the block as if to see the latest Star Wars film. Most market analysts now agree that the smartphone market frenzy has run its course. Apple’s strategy to reinvigorate the market by creating a higher price point product has predictably fallen flat. Apple’s move surprised me because the marketers at Apple seemed to miss the consumer market sentiment. Water resistance in my view was the last major device feature with a market need to protect phones from the dreaded “toilet drop.” Samsung introduced water resistance in the 5th generation Galaxy, and permanently in the Galaxy 7. I have not been motivated to buy a new phone since the Galaxy 7.

In another, more dramatic and pivotal example, my first personal experience of the specsmanship phenomenon was at Intel, during the original first generation microprocessor war: the Intel 8086 versus the Motorola 68000. Without diving too deeply into the technical specifications, the Intel 8086 on its face was technically inferior to the Motorola 68000 at a critical time when microprocessors were very new, customers had doubts, and the market was just beginning to establish a foothold in electronics design. Facing this marketing challenge, Intel’s Vice President of Marketing at that time, Bill Davidow, made a momentous decision to “differentiate” Intel and the 8086 not its specifications, but on Intel’s long-term vision for its microprocessor family of products and to focus its marketing efforts on senior management executives of its customers, not the engineers. Davidow famously delivered a presentation to the Intel sales force, “How To Sell A Dog.” The message was to ignore the spec and concentrate on the customers higher level needs, and the security of an investment in Intel with its long-term vision to provide them with greater value and competitive advantage.

Motorola fatefully decided to concentrate its marketing strategy entirely on the superior technical specifications of the 68000, poignantly winning a small skirmish but losing the war. Intel dominates the general purpose microprocessor market to this day. The Intel versus Motorola story is definitively detailed in Bill Davidow’s now famous book, Marketing High Technology: An Insider’s View. Davidow’s book also includes numerous gems of insight into marketing. Bill’s thoughts on the barriers to a new entrant into an existing market have stuck with me over the years.

If the smartphone market is ever to revive, it needs to learn from Davidow’s lesson, ignore the specs, and concentrate on creating a higher level marketing message that meets deep customer needs.

Bill Davidow, former Intel Marketing Vice President

HBS Professor Ted Levitt’s Total Product Concept And Its Influence On Davidow

Though I have met with Bill Davidow many times, spent time with him, and invited him to speak with executives of an emerging technology company, I have never directly asked him about the degree to which Harvard Professor Ted Levitt’s concept of a Total Product influenced him. It does seem highly likely that it is the case. By way of example, marketers often refer to “product differentiation.” Specsmanship is the lowest possible form of product differentiation. Creating a higher level of product value is the true essence of product differentiation. This is also the essence of Levitt’s now legendary Total Product. What is different in the Intel case is my memory of how Levitt’s Total Product model, was adapted at Intel. I will explain.

Levitt’s classic Total Product model is graphically displayed here:

In my personal view and recollection which I show here, I believe Davidow focused on the “Augmented Product,” “Expected Product” and the “Potential Product,” and avoided the “Generic Product” to win the specsmanship war with Motorola. I also distinctly remember a slightly different Intel model which is shown below.

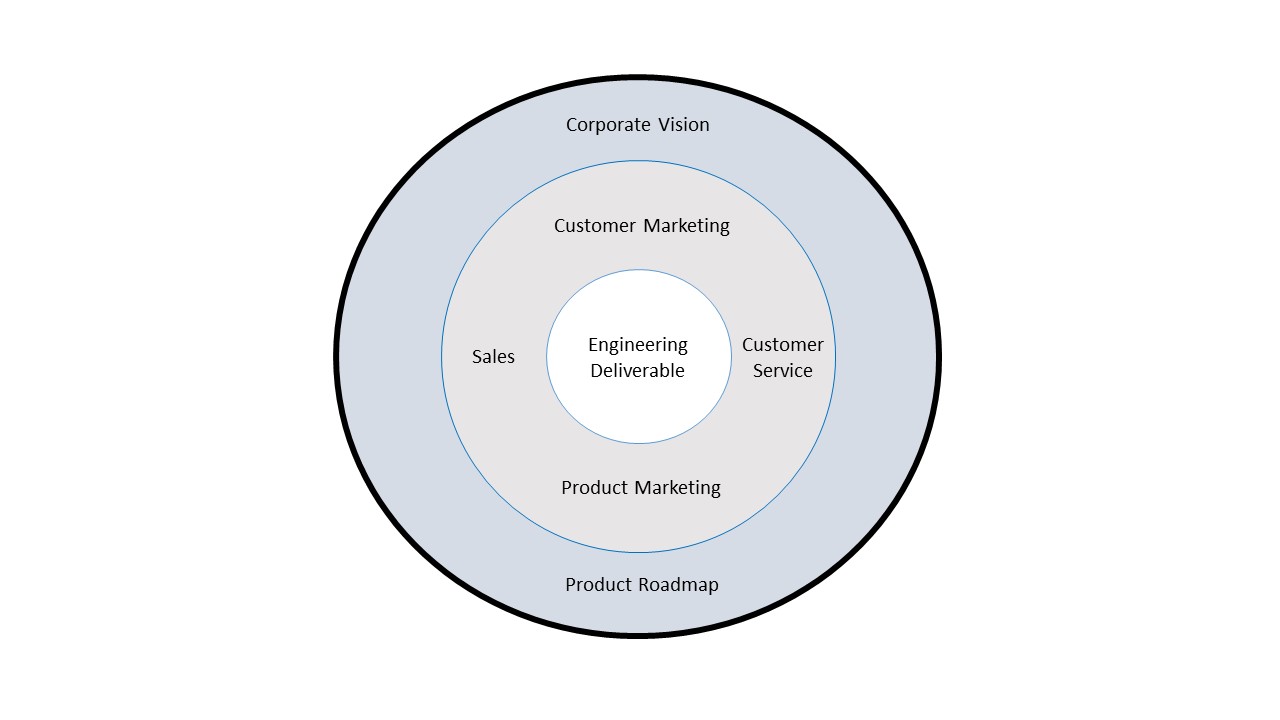

The Intel Variation On The Ted Levitt Total Product Model

It is my recollection that we at Intel, and most likely Bill Davidow in particular, adapted the Ted Levitt model to Intel’s particular new market realities, and focused on the outer circle, “Corporate Vision” and “Product Roadmap” to win the microprocessor war. The “Engineering Deliverable” is not a product. It is only a naked engineering project deliverable. Specsmanship does not make it a product. The “Corporate Vision” and “Product Roadmap” offer greater long-term value to customers, and ultimately create a powerful brand image.