Amid another leak of documents revealing large-scale international tax avoidance, the secretary-general of the Organisation for Economic Co-operation and Development (OECD) said Monday that tax avoidance was fast becoming a thing of the past. “When we’re talking about the ‘Panama Papers’ or ‘Paradise Papers’we’re talking about a legacy that is fast disappearing,” Angel Gurria said. Speaking at the Confederation of British Industry (CBI) conference in London, Gurria said governments were working hard to stop tax avoidance and evasion.

Tax avoidance is allegedly a ‘legacy issue,’ OECD’s Angel Gurria says

Gurria was Speaking at the Confederation of British Industry (CBI) conference in London

He said governments were working hard to stop tax avoidance and evasion

U.K. Prime Minister Theresa May said her government is continuing to work against tax evasion

CNBC.com

Photographer | Collection | Getty Images

Amid another leak of documents revealing large-scale international tax avoidance, the secretary-general of the Organisation for Economic Co-operation and Development (OECD) said Monday that tax avoidance was fast becoming a thing of the past.

“When we’re talking about the ‘Panama Papers’ or ‘Paradise Papers’we’re talking about a legacy that is fast disappearing,” Angel Gurria said.

Speaking at the Confederation of British Industry (CBI) conference in London, Gurria said governments were working hard to stop tax avoidance and evasion.

“When we talk about ‘Double Irish’ or ‘Double Dutch’ (tax avoidance schemes) we’re talking about structures which are no longer there,” she said, adding: “This will not be repeated because of the work you and your governments and the OECD have done in the last few years.”

“There is quite literally no place to hide,” he said, noting that 50 countries had implemented automatic information exchanges regarding tax and that more nations were planning to do the same.

Gurria’s comments come after a leak of millions of documents revealing large-scale tax avoidance by high-profile individuals and companies via offshore financial services companies. The latest tax avoidance leak has been dubbed the “Paradise Papers” and comes after a similar leak in 2016 called the “Panama Papers” that showed how a Panamanian law firm allegedly helped its clients to avoid taxes by using offshore tax havens.

Speaking at the same business conference on Monday, U.K. Prime Minister Theresa May said that her government had continued the work against tax evasion that her predecessor David Cameron had begun.

“He started this work, not only in the U.K. economy but on an international stage. So we have seen more revenues coming into HMRC (the U.K.’s tax-collecting department) over the last few years, with £160 billion extra since 2010,” she said.

More work was being done to ensure “greater transparency” in the U.K.’s dependencies and British overseas territories, May said, and HMRC was already able to access more information about so-called “shell” companies.

“We want people to pay the tax that is due,” she said. That sentiment was echoed by the leader of the opposition Labour party, Jeremy Corbyn, who said that society was “undermined” by anyone that did not pay the tax they owed.

The truth is that for all of the tough talk from Li Xinping about stopping the massive outflows of capital from China, some of it probably dark money obtained from dubious enterprises and kickbacks, nothing has changed in China or in the Western cities eager to share in the wealth. Rich, Young “Fuerdai” Chinese Are Buying Overseas Properties on Their Smartphones. Millennials acquire real estate in other countries as hedge against a weakening currency, homes for their own children when they study abroad

The truth is that for all of the tough talk from Li Xinping about stopping the massive outflows of capital from China, some of it probably dark money obtained from dubious enterprises and kickbacks, nothing has changed in China or in the Western cities eager to share in the wealth.

Rich, Young “Fuerdai” Chinese Are Buying Overseas Properties on Their Smartphones

Millennials acquire real estate in other countries as hedge against a weakening currency, homes for their own children when they study abroad

An increasingly larger group of Chinese millennials are looking to buy property abroad. Above, a potential buyer inspects a house for sale in Australia.

Reblogged from The Wall Street Journal, Real Estate

By Dominique Fong

Updated May 9, 2017 10:59 p.m. ET

BEIJING— Zheng Xiaohei, a marketer from Urumqi in western China, made his first overseas property investment without so much as a visit.

Mr. Zheng, 29 years old, in March purchased a studio apartment in Thailand for about 650,000 yuan ($94,255) using his smartphone and an app called Uoolu that connects users to overseas property listings.

“Investing in overseas real estate was mainly due to my good impression of Thailand,” Mr. Zheng said.

Founded two years ago, Beijing-based Uoolu is focused on tapping a specific group of home buyers: Chinese millennials looking for foreign properties.

About 70% of Chinese millennials, those born between 1981 and 1998, own a home, the highest share of respondents from nine countries and regions who were surveyed in a recent HSBC study. Chinese parents often register home purchases under their child’s name to prepare the child for marriage and raising a family, which likely boosts the percentage.

Still, a growing sliver of Chinese millennials are looking to buy property abroad. Kevin Lee, chief operating officer of Beijing-based consulting firm Youthology, put the percentage in the low single digits but said it would continue to increase.

Uoolu said about 80% of its monthly active users are between the ages of 20 and 39, and that 20,000 customers have bought or are in the process of purchasing overseas property. A similar real-estate platform, Juwai.com, estimates that roughly 30% to 40% of its buyers are millennials.

Cherubic Ventures, a venture-capital firm with offices in Beijing and San Francisco, invested an undisclosed sum in Uoolu. One selling point, said the firm’s founder, Matt Cheng, was Uoolu’s target of reaching young Chinese buyers who are tech savvy and interested in cross-border investments, “but don’t know where to begin.”

Overseas investing isn’t easy at a time when the Chinese government is clamping down on capital flight amid concerns about a weakening currency. Chinese citizens aren’t allowed to transfer more than $50,000 a year out of the country or use those funds to buy overseas property.

However, this increased government scrutiny is “slowing but not cutting off” the surge of investment in U.S. property, said Arthur Margon, partner at Rosen Consulting Group.

“The more the government limits people, the more they want to invest overseas,” said Wang Hao, Uoolu’s 33-year-old chief operating officer.

People often skirt the foreign-exchange rules by, for example, pooling money among family members and friends and separately sending it into overseas bank accounts. Also, Chinese citizens who have studied or worked abroad for a few years might already have bank accounts in other countries and those overseas funds are beyond the Chinese government’s control.

Alan Wang, a 19-year-old college student in Toronto who comes from Shenzhen, said he opened a bank account in Canada for education expenses. Now it is useful for buying property, too. He and his family are thinking about purchasing a home on a budget of about 1 million Canadian dollars (US$730,600) this summer. To do so, he will have relatives send money to his bank account, he said.

Uoolu helps buyers open bank accounts in other countries and apply for mortgages there. Users pay a deposit to reserve the right to purchase a home. The money is sent directly from a buyer’s bank account to the overseas developer—Uoolu says it doesn’t handle the cross-border transaction within the mobile app.

Chris Daish, a real-estate agent at Triplemint in New York, said one of his Chinese clients, an accountant in her mid-20s who works in New York, earlier this year pooled $110,000 from five family members to help buy her a condo in the city.

“It’s a really arduous task even to get a couple hundred grand out,” said Mr. Daish, who emphasized that he doesn’t help clients with money transfers.

A 28-year-old who works in finance in Beijing in February bought two apartments in Bangkok for a total of 5 million yuan ($725,000), one for a vacation home and the other for rental income. She declined to disclose her name out of fear of government retaliation for violating capital controls.

As for some of her friends, she said, “They wish to buy but dare not.”

Despite all of the revelations of the sources and methods of the Vancouver housing bubble over the last two years, the situation remains largely unresolved. Ditto in Toronto. The foreign buyers’ tax has had only a limited effect and has problems. Fueled by dark foreign money housed in anonymous offshore shell companies like those disclosed in the Panama Papers, the money is managed by local financial manipulators at the behest of unidentifiable persons overseas. The foreign buyers continue to enjoy the weakest enforcement jurisdiction in Canada

Despite all of the revelations of the sources and methods of the Vancouver housing bubble over the last two years, the situation remains largely unresolved. Ditto in Toronto. The foreign buyers’ tax has had only a limited effect and has problems. Fueled by dark foreign money housed in anonymous offshore shell companies like those disclosed in the Panama Papers, the money is managed by local financial manipulators at the behest of unidentifiable persons overseas. The foreign buyers continue to enjoy the weakest enforcement jurisdiction in Canada

‘Corrupt Elite’ Still Laundering Money In Canadian Housing: Transparency International Report

British Columbia’s gleaming gem, Vancouver, is found to still be the worst case example

Reblogged: The Huffington Post Canada | By Daniel Tencer

Posted: 03/31/2017 12:16 pm EDT Updated: 5 hours ago

Loopholes in Canadian law are allowing a “corrupt elite” to use the housing market for money-laundering, says a new report from Transparency International (TI).

The report found 10 problem areas with the laws related to real estate transactions in Canada, Australia, the U.K. and the U.S. — four countries it identifies as being hot-spots for real estate-related money laundering.

“Canada’s legal framework has severe deficiencies under four of the 10 identified areas,” TI stated in the report. “In the other six, there are either significant loopholes that increase risks of money laundering through the real estate sector or severe problems in implementation and enforcement of the law.”

This Grey’s Point “tear down” property shown here, recently sold for over $9 Million, more than $1 Million over the asking price of $7.8 Million. There were 11 offers, all cash, and no offer included any contingencies.

One glaring problem is a lack of rules requiring that the actual owner (or “beneficial owner”) of a property be identified. In Canada “there are no requirements for any person involved in real estate closings to identify the beneficial owner,” the TI report stated.

The report found that 29 of the homes were owned by shell companies, either Canadian or offshore.

“Offshore companies pose a serious risk … because they are able to purchase property without needing to disclose any information relating to who ultimately owns and controls them to any government authority,” TI said in the report published Wednesday.

The report noted that money-laundering through real estate is growing increasingly popular.

“Large amounts of money can be legitimized at once, maintaining or increasing its value. Investments in real estate are seen as an alternative for those who fear having offshore accounts frozen.”

This chart from Transparency International shows what is known, and not known, about the ownership of Vancouver’s 100 most expensive homes.

Because of over-reliance on banks to spot money-laundering activities, and because banks aren’t involved in cash purchases of homes, money-laundering is going unnoticed, the report said.

And like in the other countries studied, in Canada “there are no data on prosecutions against real estate agents or other professionals for facilitating money laundering.”

Canada has “the best model” for enforcement of money-laundering laws among the four countries studied, the report said, but Canada’s financial intelligence agency, FINTRAC, investigates relatively few real estate transactions.

The report lays out a series of recommendations for governments, including requiring all professionals involved in a real estate transaction to disclose the actual buyer. This should also be required of companies that are buying real estate, the report said.

It also suggested that professionals involved in real estate transactions, such as lawyers and realtors, be registered with a country’s anti-money laundering authorities before they are allowed to practice.

“Governments must close the loopholes that allow corrupt politicians, civil servants and business executives to be able to hide stolen wealth through the purchase of expensive houses in London, New York, Sydney and Vancouver,” TI chair José Ugaz said in a statement.

“The failure to deliver on their anti-corruption commitments feeds poverty and inequality while the corrupt enjoy lives of luxury.”

How many shell companies exist in Canada? How many legal trusts? Who are the beneficial owners protected by such unnecessary veils of secrecy? No one knows because in most cases there is no legal requirement to disclose actual ownership even to regulators. In fact, more information is required to get a library card than to set up a company in most jurisdictions in Canada. What we do know is that Canada ranks near the bottom among our OECD partners in terms of corporate disclosure requirements to fight money laundering and tax evasion. A recent report from Transparency International detailed the dismal situation and why our country has become a haven for dubious offshore property speculation.

The Shell Game: Canada’s Lax Disclosure Laws Open Door to Tax Fraud, Money Laundering

Transparency International warns against country becoming a ‘haven for corrupt capital.’

Canada can avoid becoming a desirable destination for dubious global lucre if it acts soon.

How many shell companies exist in Canada? How many legal trusts? Who are the beneficial owners protected by such unnecessary veils of secrecy? No one knows because in most cases there is no legal requirement to disclose actual ownership even to regulators. In fact, more information is required to get a library card than to set up a company in most jurisdictions in Canada.

What we do know is that Canada ranks near the bottom among our OECD partners in terms of corporate disclosure requirements to fight money laundering and tax evasion. A recent report from Transparency International detailed the dismal situation and why our country has become a haven for dubious offshore property speculation.

“The Canadian government must take immediate steps to require all companies and trusts in the country to identify their beneficial owners to ensure Canada does not become a haven for corrupt capital,” warns Transparency International Canada executive director Alesia Nahirny.

Canada is one of the few developed countries that does not require the identities of company directors to be verified or any information on shareholders. In most provinces, it is legal to use “nominee” directors or shareholders without disclosing that they are acting on someone else’s behalf.

A nominee is essentially a sock puppet — the proverbial student or homemaker often listed as the title owner of some of Canada’s most expensive homes. Why would someone list a multi-million dollar property in someone else’s name? Some plausible reasons include to avoid taxes or to launder money. This practice remains completely and inexplicably legal in most parts of our painfully polite country.

Lawyers can also act as nominee directors, offering their clients an additional level of secrecy under solicitor-client privilege unavailable in most other countries. A ruling from the Supreme Court of Canada in 2015 exempted lawyers and their firms from important parts of the Proceeds of Crime and Terrorist Financing Act, further widening the yawning loopholes in our laws meant to fight money laundering. According to an international oversight body, the Financial Action Task Force of which Canada is a member, “the legal profession in Canada is especially vulnerable to misuse.”

Toronto lawyer Simon Rosenfeld was secretly taped in 2002 during a meeting in a Miami bar with an undercover RCMP officer, who was posing as a member of a Columbian drug cartel needing money-laundering services. According to the officer’s testimony, after exchanging a token dollar to cement solicitor-client secrecy, Rosenfeld bragged that moving illegal funds through Canada was “20 times” easier than the U.S., where arrest and convictions are much more likely. He described the Canadian enforcement regime as “la la land” and said that five other lawyers in Vancouver laundered $200,000 per month through trust accounts for a seven per cent commission.

The transcript of this conversation did not endear Rosenfeld to the jury during his prosecution and he was sentenced to three years in jail. He appealed the conviction and the higher court judge increased his sentence to five years. This rare successful enforcement provides some fleeting schadenfreude, but Rosenfeld’s seasoned and sad assessment of “la la land” continues to ring true.

Legal black boxes

Millions of legal trusts are estimated to exist in Canada, but there is no way of knowing since there is no requirement for them to be registered or file any record of their existence — again an outlier among other countries. They are supposed to file information on assets and trustees with the Canada Revenue Agency but only a small fraction actually do.

A trust is the consummate legal black box. Considered a mere private contract under Canadian law, trusts do not need to keep records on beneficial owners, let alone file such documents with the federal government. Trustees can conduct transactions without disclosing their role as go-betweens, making it difficult or impossible for financial institutions to comply with money laundering regulations. To our international embarrassment, the Financial Action Task Force found in 2016 that Canada was less than fully compliant in 29 out of 40 anti-money laundering measures and “non-compliant” regarding transparency and beneficial ownership of such legal arrangements.

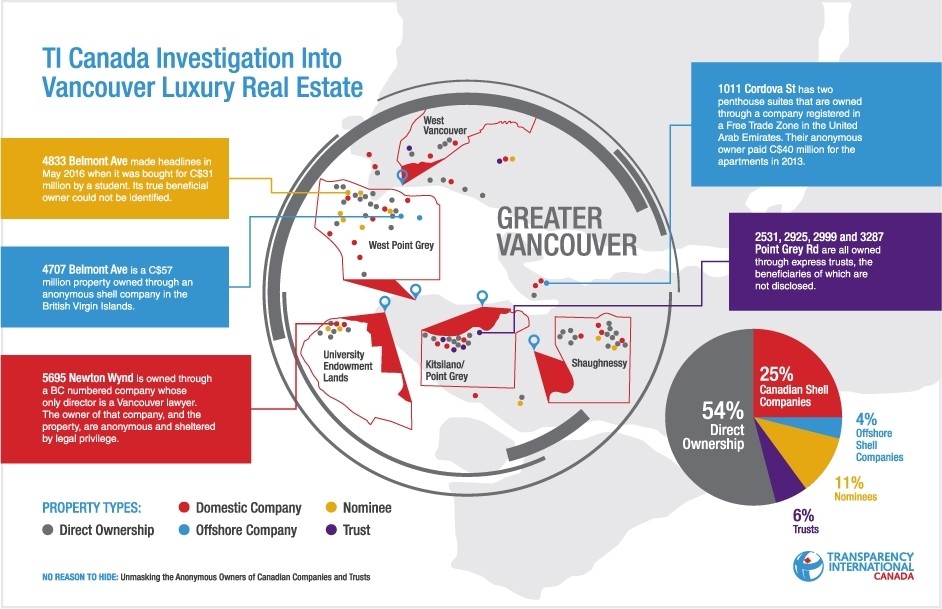

Real estate in Vancouver and Toronto is where the rubber really hits the road on these national regulatory failings. Transparency International looked at the title documents for the 100 most expensive homes in the Lower Mainland and unsurprisingly found a sampling of all these methods to conceal the beneficial owners. Twenty-nine properties were held by Canadian or offshore shell companies, 11 were owned by nominees with no obvious source of income, six more were held by trusts. In total, 49 of these luxury estates collectively worth more than $1 billion had opaque ownership.

Canada’s lax legal oversight coupled with a decades-long public policy effort to incentivize wealthy citizenship has turned Vancouver into a global hedge city. Like London, New York, and San Francisco, Vancouver’s luxury properties have become a favored place to stash cash for the world’s wealthiest.

According to professor David Ley at the University of British Columbia, Canada effectively sold Canadian citizenships to rich offshore investors through the now-cancelled Business Immigration Program. Ley described the scheme during a lecture last September, detailing how up to 200,000 of the world’s wealthiest may have arrived in the Lower Mainland as a result of these public policy efforts, inflating property values and contributing to our current housing woes.

According to Ley, Canada’s BIP was heavily oversubscribed because Canada was selling citizenships for far below the international market rate compared to other countries with similar citizenship-for-sale incentive programs. In the U.S., candidates had to invest $1,000,000 and employ up to 10 Americans before being granted citizenship. In Canada, investors only had to loan provincial governments $800,000 to be paid back in full after five years. This come-and-get-it attitude towards passports and global capital seems sadly similar to other national assets such as natural resources, but I digress.

Besides ballooning our housing prices, was there a net economic benefit to this citizenship fire sale? According to Ley, the federal immigration database showed that “of all immigration streams to Canada, the Business Immigration Program led to the lowest declared incomes, lower even than refugees.” This was in part because wealthy offshore investors are so skillful at avoiding taxation coupled with a shocking lack of enforcement from the CRA.

Defending against dubious lucre

What can Canada do to clean up this mess and avoid becoming an even more desirable destination for dubious global lucre? A low-cost first step would be to require all Canadian companies and trusts to declare beneficial owners and publish this information on a public searchable registry. The United Kingdom brought in such a system in 2016 to improve in law enforcement and tax collection, which will more than cover the cost of implementation.

Transparency International has several other practical suggestions that are also supported by the banking sector and law enforcement:

Beneficial ownership should be listed on all land title documents, ideally retroactively.

Corporate registries should have the resources and requirement to accurately identify directors and shareholders

The federal government should require all sectors — including real estate agents — to identify beneficial owners before transactions are conducted.

Besides money launderers, tax evaders and criminals, who could possibly oppose these sensible and long overdue reforms? Is the Trudeau government going to act quickly to plug these gapping holes and bring our country in line with the global fight against illicit capital? The recent cash-for-access events with wealthy offshore investors provide a telling opportunity to see on whose behalf Trudeau is acting. The whole country is watching.

Reading this article today, I am dumbfounded that Anbang managed to get this far in the purchase of B.C. commercial real-estate without red flags going up. This mysterious Chinese company, Anbang Insurance Group has attracted the attention of The New York Times, The Wall Street Journal, Forbes, Fortune Magazine, and government authorities in the United States and other countries. A months-long investigation by the New York Times revealed an extremely opaque structure, empty offices, obscure shareholders, and extensive political connections to the Chinese elite. Anbang has all the earmarks of Chinese money laundering, corruption at the highest levels, and mysterious shell companies. It is a cautionary tale for Canadian authorities fretting over foreign real-estate buyers and skyrocketing real-estate prices.

Reading this article today, I am dumbfounded that Anbang managed to get this far in the proposed purchase of B.C. commercial real-estate without red flags going up. This mysterious Chinese company, Anbang Insurance Group has attracted the attention of The New York Times, The Wall Street Journal, Forbes, Fortune Magazine, and government authorities in the United States and other countries. A months-long investigation by the New York Times revealed an extremely opaque structure, empty offices, obscure shareholders, and extensive political connections to the Chinese elite. Anbang has all the earmarks of Chinese money laundering, corruption at the highest levels, and mysterious shell companies. It is a cautionary tale for Canadian authorities fretting over foreign real-estate buyers and skyrocketing real-estate prices.

The dingy fourth floor of this building in Beijing houses two companies that control assets of Anbang Insurance Group worth more than $15 billion.

The Anbang Insurance takeover is currently under scrutiny by the federal government’s Investment Review Division because it exceeds the $600-million threshold and it will ultimately be up to Innovation Minister to make a decision.

A massive Chinese insurance company with a murky ownership structure is buying a majority stake in one of British Columbia’s biggest retirement home chains, a deal believed to exceed $1-billion that would give Beijing-based Anbang Insurance an important role in the delivery of health care in B.C.

Anbang Insurance Group, which has emerged in recent years to launch a global buying spree, has cut a deal to buy Vancouver-based Retirement Concepts, a family-owned retirement home business established in 1988.

This foreign takeover is currently under scrutiny by the federal government’s Investment Review Division because it exceeds the $600-million threshold and it will ultimately be up to Innovation Minister Navdeep Bains to make a decision.

Retirement Concepts owns and operates about 24 retirement “communities,” mostly in B.C., except for several properties in Calgary and Montreal. What makes it even more attractive is that it also owns holdings of unused or partly developed land that would allow a major expansion of facilities in the future.

The company is an important part of B.C.’s health-care delivery system. Retirement Concepts is the highest-billing provider of assisted living and residential care services in the province. The B.C. government paid the company $86.5-million in the 2015-16 fiscal year, more than any other of the 130 similar providers.

A source familiar with the deal said it exceeds $1-billion, but Retirement Concepts declined to confirm the size of the transaction. “The terms of the proposed transaction have not been disclosed publicly and we cannot comment on the amount you refer to,” said Azim Jamal, president and chief executive of Retirement Concepts.

Foreign investments are reviewed to determine whether they provide a net benefit to Canada and are compatible with this country’s industrial, economic and cultural policies and what impact they will have on Canadian participation in the business.

The Canadian government is eager to attract foreign money to make up for insufficient investment capital within Canada and acquisitions by foreigners are rarely rejected. Prime Minister Justin Trudeau is particularly eager to attract more investment from China and has begun exploratory free-trade talks with Beijing. The Liberals have already signalled they are open to rolling back a ban on state-owned Chinese investment in the oil sands imposed by former prime minister Stephen Harper.

Anbang appears to have gone to some lengths to conduct this B.C. deal below the radar.

The name of the firm acquiring Retirement Concepts is Cedar Tree Investment Canada, which was incorporated as a federal Canadian company only in July. Cedar Tree’s registration initially gave the names of its two directors as Hong Zhao and Ye Zhang with their contact address as Suite 2560 at 200 Granville St. in downtown Vancouver. People with the same names and address are also the two listed directors for Maple Red Financial Management Canada Inc., the company that Anbang used to buy a controlling interest in all four towers of Vancouver’s Bentall Centre last year.

The directors have since changed, as has their address, and Cedar Tree’s contact information is now a major Canadian law firm’s downtown Vancouver office.

Telephone calls and e-mails to Cedar Tree Investment’s listed directors were not returned. The Globe and Mail was also unable to reach anyone at Anbang International, Anbang Insurance’s global investment arm, at its Vancouver number.

In April, after abruptly walking away from an effort to buy Starwood Hotels & Resorts, one the world’s largest hotel companies, Anbang appears to have been shifting its attention to the Canadian market with a bid for Innvest, one of this country’s biggest hotel owners. This came amid reports from China that Chinese regulators were looking into whether its foreign asset acquisition binge – including the Waldorf Astoria hotel in New York – exceeded allowable limits.

Bloomberg News, citing a source involved in the transaction, reported that the CEO of the firm that would go on to buy Innvest, Bluesky Hotels & Resorts’ Li Chen, had said at the outset of the acquisition talks that she was representing Anbang but did not wish this company to be publicly identified as the buyer. Anbang later publicly denied “any connection” between it and Bluesky.

An investigation by The New York Times earlier this year revealed that 92 per cent of Anbang is currently held by firms either fully or partly owned by relatives of Anbang’s chairman, Wu Xiaohui, or his wife, the granddaughter of the former Chinese leader Deng Xiaoping, or Chen Xiaolu, the son of a famous People’s Liberation Army leader.

The B.C. retirement home acquisition thrusts Anbang into a new area of business: Canada’s health-care system.

Under international trade deals that Canada has signed, the provinces retain the right to refuse to give health-care contracts to foreign companies. That’s because Canada reserved the right in trade agreements for governments to discriminate against foreign suppliers of services in the health-care sector and foreign investors when it comes to health care.

Retirement Concepts, however, says it will remain as operator under a deal with Cedar Tree. Asked about how the Beijing company conducted itself in the transaction, Mr. Jamal said, “Anbang was transparent in its bidding from the outset.”

Mr. Jamal said Retirement Concept’s existing corporate team will remain intact to “provide continuity” to residents and the business.

“Under the partnership agreement, Retirement Concepts will retain a minority share and will continue to manage the day-to-day operations of all of our seniors’ communities,” the CEO said.

“As a result, there will be no change to staffing plans, the quality of care provided to our residents, nor to our policies, procedures and other operating standards.”

British Columbia’s Liberal government, however, says it is not concerned about the Retirement Concepts deal because it does not believe the patients at the company’s facilities will see a difference in the care they receive.

“Cedar Tree has assured patients, families and staff that it does not intend to make any changes to day to day operations, patient care, staff or leadership. In fact, they will all remain in operation as they are today,” B.C. Minister of Health Terry Lake said in a statement.

“We expect this change to be seamless, and that the patients residing in these facilities will continue to get the same quality of care.”

The B.C. government said nothing also prevents a foreign-owned company from owning a health-care provider.

“The Community Care and Assisted Living Act does not prohibit facilities from being sold to an out-of-province, or to an off-shore purchaser,” spokeswoman Kristy Anderson of B.C.’s Health Ministry said.

The Investment Review Division at the federal department of Innovation confirmed it’s reviewing the acquisition before Mr. Bains makes a decision. “Cedar Tree Investment Canada has filed an application for review under the Investment Canada Act of its proposed acquisition of Retirement Concepts,” spokeswoman Stéfanie Power said in a statement.

“Due to the confidentiality provisions of the Investment Canada Act, we cannot comment further on the timing of the review.”

The department likely received the application in late September or early October but it will not confirm the date the review began. “In general terms, the Minister has 45 days from the date the application is received to make a decision. However, the Minister can extend this period by 30 days. Further extensions are possible with the investor’s consent,” Ms. Power said.

China itself faces a daunting retirement-care challenge with a rapidly graying population and it is seeking the expertise and capacity to design the vast system necessary to look after its elderly.

A mysterious Chinese company, Anbang Insurance Group has attracted the attention of The New York Times, The Wall Street Journal, Forbes, Fortune Magazine, and government authorities in the United States and other countries. The cause of the scrutiny has been Anbang’s sudden involvement in a number of massive multi-billion dollar real estate investments around the World. Formed in 2004, Anbang apparently holds assets worth at least $295 Billion, but a months-long investigation by the New York Times has revealed an extremely opaque structure, empty offices, obscure shareholders, and extensive political connections to the Chinese elite. Analysis of Anbang and its operations holds a potential lesson for Canadian authorities fretting over foreign buyers and skyrocketing real-estate prices.

A mysterious Chinese company, Anbang Insurance Group has attracted the attention of The New York Times, The Wall Street Journal, Forbes, Fortune Magazine, and government authorities in the United States and other countries. The cause of the scrutiny has been Anbang’s sudden involvement in a number of massive multi-billion dollar real estate investments around the World. Formed in 2004, Anbang apparently holds assets worth at least $295 Billion, but a months-long investigation by the New York Times has revealed an extremely opaque structure, empty offices, obscure shareholders, and extensive political connections to the Chinese elite. Wu Xiaohui, Anbang’s Chairman, is married to Deng Xiaoping’s granddaughter and involved with at least two others with family connections to the People’s Liberation Army. Both Wu and his wife, Zhuo Ran have disappeared from Anbang’s list of shareholders after the New York Times investigation began. Anbang has all the earmarks of a Panama Papers situation: Chinese money laundering, corruption at the highest levels, and mysterious shell companies. Analysis of Anbang and its operations is a cautionary tale for Canadian authorities fretting over foreign real-estate buyers and skyrocketing real-estate prices.

Last Spring, as B.C. Premier Christy Clark was preparing to announce new regulations to stem the flood of non-resident residential real-estate buyers, she simultaneously flew to China on a trade mission with a group of B.C. commercial real estate moguls, apparently to reassure the Chinese that B.C. was still interested in Chinese commercial real-estate investment. But by the time Clark made her trip to China, questions about the Anbang Insurance Group’s ownership had already been flying in the U.S. financial press for over two years. Whether it may have been more prudent for Clark to defer promoting Chinese commercial real estate investment in Vancouver, only time will tell. What does appear clear is that China is demonstrating a much more aggressive, arrogant and even hostile tone in its relations with both Canada and the United States. This is evidenced by this week’s G20 Summit in Hangzhou, beginning with the deliberate snubbing of Barak Obama on arrival in China, and a number of other incidents, including Trudeau’s inability to achieve an agreement with China on canola oil. Canada needs to be smarter about how it deals with these new realities.

Anbang Insurance Group Corporate Headquarters, Beijing

The dingy fourth floor of this building in Beijing houses two companies that control assets of Anbang Insurance Group worth more than $15 billion.

Wu Xiaohui, Chairman of Anbang Insurance Group

Reblogged from The New York Times

A Chinese Mystery: Who Owns a Firm on a Global Shopping Spree?

Owners of Anbang, a Chinese insurer behind a wave of multibillion-dollar deals, include relatives and friends of its politically connected chairman.

Pingyang County’s verdant hills still hint at a long-lost China. Rice paddies and villages surround its bustling towns, and in the fields, farmers wade into the mud to plant seedlings as they have for thousands of years.

It is an odd place to find the people behind a Chinese corporate powerhouse that is turning heads on Wall Street with a global takeover binge. Yet the area is home to a tiny group of just such people — small-time merchants and villagers who happen to control multibillion-dollar stakes in the Anbang Insurance Group, which owns the Waldorf Astoria in New York and a portfolio of global names and properties.

American regulators are now asking who these shareholders are — and whether they are holding their stakes on behalf of others.

The questions add to the mystery surrounding a company that seemed to come out of nowhere, surprising deal makers with offers to pay more than $30 billion for assets around the world.

Anbang’s shopping spree is part of an outflow of money from China that has reshaped global markets but has often been shrouded in secrecy, sometimes by prominent Chinese looking to shift their wealth abroad without attracting attention at home. That poses a problem for international regulators trying to identify the buyers behind major acquisitions and to assess the riskiness of these deals.

The Anbang shareholders in the Pingyang County area hold their stakes through a byzantine collection of holding companies. But according to dozens of interviews and a review of thousands of pages of Anbang filings by The New York Times, many of them have something in common: They are family members and acquaintances of Wu Xiaohui, Anbang’s chairman, a native of the county who married into the family of Deng Xiaoping, China’s paramount leader in the 1980s and ’90s.

In many ways, Anbang and Mr. Wu appear to be archetypal products of China’s mix of freewheeling capitalism and Communist Party dominance, a formula that has fueled nearly four decades of untrammeled growth.

Anbang got its start as an auto insurance company in 2004 in the eastern Chinese city of Ningbo. For years it was only a minor player. But it took off as it became more aggressive with its finances, buying stakes in Chinese banks and bringing in money by selling high-risk, high-yield investment funds to ordinary Chinese.

Mr. Wu, 49, a former car salesman and low-level antismuggling official, led Anbang through this transformation and is now known as one of China’s most successful businessmen. He wears tailored suits and polished loafers,hobnobs with the likes of Stephen A. Schwarzman of Blackstone, and sometimes holds court at Harvard.

But he does not appear in Anbang’s filings as an owner.

It is common in China for the wealthy to have their shares in companies held in others’ names. Known in Chinese as baishoutao, or white gloves, these people are often trusted relatives or acquaintances. Many defend the practice as a way to protect their privacy in a nation where riches can be a political liability. But others say white gloves can be used to hide ill-gotten gains and thwart corruption investigators.

On the fourth floor of this shabby building in Beijing is an office that is home to two companies with a total stake of more than $15 billion in assets of one of China’s biggest financial conglomerates: the Anbang Insurance Group.CreditGilles Sabrie for The New York Times

Anbang did not respond when asked if Mr. Wu was a shareholder and declined to answer questions about its owners.

The company, a spokesman said, “has multiple shareholders who have made all required disclosures under Chinese law. They are a mix of individual and institutional shareholders who made a commercial decision to invest in the company. Anbang has now grown to be a global company thanks to the support of these long-term shareholders.”

For investors and regulators, white gloves can make it difficult to evaluate the financial health of a Chinese buyer. Ownership may be concentrated in the hands of a few people, posing hidden risks, and companies with government connections could be vulnerable to political shifts or become magnets for corruption.

“It is very important for businesses to know who they are ultimately doing business with, and for investors, what they are investing in,” said Keith Williamson, a managing director in Hong Kong at Alvarez & Marsal, a firm that carries out corporate fraud investigations.

It is not clear whether the shareholders in the Pingyang County region are holding large stakes on behalf of anyone else. But on May 27, Anbangwithdrew its application with New York State to buy an Iowa insurer, Fidelity & Guaranty Life, for $1.6 billion. Regulators had asked about ties between several shareholders with the same family names, said one person briefed on the matter who spoke on the condition of anonymity.

A $6.5 billion deal for a portfolio of hotels that includes the Essex House in New York and several Four Seasons locations is awaiting results from a security review by the American government. In March, Anbang withdrew a $14 billion bid for Starwood, the operator of Sheraton and Westin hotels, in a move that surprised Wall Street.

The company could come under greater scrutiny as it prepares to sell sharesin its life insurance business on the Hong Kong stock exchange next year. Already, at least one major New York-based investment bank has raised concerns about Anbang’s ownership after studying its shareholding structure to evaluate whether to help with its overseas deals, according to two people involved in the matter who asked not to be identified because the process was private. The bank did not participate in Anbang’s deals.

Separately, the Chinese magazine Caixin reported in May that Chinese regulators were examining Anbang’s riskier financial products. It is unclear where that inquiry stands or whether Anbang’s ownership structure is being investigated.

President Xi Jinping has waged a campaign against graft since taking office, and the use of white gloves has recently come under scrutiny. “White gloves are accompanied by power’s black hands,” the Communist Party’s disciplinary watchdog wrote in a report last year.

Questions about Anbang’s owners come as Chinese companies make deals around the world — sometimes representing efforts by China’s powerful to move money out of the country, as the economy slows and the party tightens its grip on everyday life.

Photo

Wu Xiaohui, chairman of Anbang, at a global insurance conference in 2015.CreditBen Asen/International Insurance Society

China has encouraged some capital outflow to improve the performance of its investments and expand its influence. But the subject of the elite moving money overseas is politically sensitive, raising questions about the source of their wealth and their confidence in the Chinese economy.

Luo Yu, the son of a former chief of staff of China’s military, said China’s most politically powerful families had been transferring money out of the country for some time.

“They don’t believe they will hold on to power long enough — sooner or later they would collapse,” said Mr. Luo, a former colonel in the Chinese Army whose younger brother was a business partner with one of Anbang’s founders. “So they transfer their money.”

At its founding in 2004, Anbang had an impressive list of politically connected directors. Records show early Anbang directors included Levin Zhu, son of a former prime minister, and Chen Xiaolu, the son of an army marshal who helped bring Communist rule to China.

Then there was Mr. Wu, who was born Wu Guanghui but was known as Wu Xiaohui from a young age. Relatives said he grew up in a Catholic family; a crucifix sat on his aunt’s dining room table, and she wears a necklace with a portrait of the Virgin Mary.

Mr. Wu married Zhuo Ran, a granddaughter of Deng, the Chinese leader who brought China out of the chaos of the Mao era. Together, Mr. Wu, Ms. Zhuo, Mr. Chen and their relatives owned or ran the companies that controlled Anbang, according to company filings.

Anbang leapt onto the global stage with last year’s purchase of the Waldorf Astoria and its aborted bid for the Starwood chain. By this year, Anbang’s assets had swelled to $295 billion.

It is not clear what prompted Anbang’s sudden interest in overseas assets. But the shift came after a reshuffling of its ownership structure that also led to the injection of more than $7.5 billion into the company.

Company documents filed with Chinese agencies show that the number of firms holding Anbang’s shares jumped to 39, from eight, over six months in 2014. Most of those firms received large injections of funds. At the same time, Anbang’s capital more than quintupled.

Ms. Zhuo disappeared from the ownership records by the end of that year. Many of Mr. Wu’s relatives did as well. Mr. Wu and Mr. Chen had disappeared earlier from the records.

Photo

The Anbang Insurance Group owns the Waldorf Astoria in New York, above, and a portfolio of global names and properties.CreditChang W. Lee/The New York Times

Mr. Zhu, who does not appear to have owned shares, disappeared in paper filings from Anbang’s roster of directors by 2009, though he was listed as a director on online government filings as late as 2014.

Mr. Wu, Mr. Chen and Mr. Zhu did not respond to requests for comment, and Ms. Zhuo could not be reached. In March, Mr. Zhu told Chinese reporters that he was not an Anbang director.

Anbang’s current shareholding firms are not well-known names in China, and some appear to have been set up just to hold Anbang shares. One lists its address as the empty 27th floor of a dusty Beijing office building. Two more list an address at a mail drop above a Beijing post office.

Using corporate filings, The Times compiled a list of nearly 100 people who own shares in the firms and traced about a dozen to Pingyang County or nearby. Reporters visited the area, in China’s eastern Zhejiang Province, and interviewed dozens of residents, including several whose names appeared on the list. They also interviewed an uncle, an aunt and a nephew of Mr. Wu.

The latter two, as well as others in the area, said one name matched that of his sister, Wu Xiaoxia. The family members said several other names matched those of Mr. Wu’s extended kin, including two cousins and others on his mother’s side of the family. Through their various stakes in Anbang shareholding companies, these people control a stake representing more than $17 billion in assets.

Other names matched local acquaintances of Mr. Wu, including Huang Maosheng, a local businessman who confirmed in a brief phone interview that he had a business relationship with Mr. Wu but declined to elaborate.

One village leader and neighbors identified the names of four of Mr. Huang’s relatives — including some whom they described as common workers — from among those on the list. Their Anbang holdings represent about $12 billion in assets.

Another resident, Mei Xiaojing, said two names on the list matched those of her relatives. Asked if she knew Mr. Wu, she said, “Well, yes,” then ended the phone conversation and did not respond to subsequent calls. Through multiple holding companies, those three people have a stake representing about $19 billion in Anbang assets.

As Anbang rose, so did Mr. Wu’s profile. In 2013 Mr. Wu secured a yearlong position as a visiting fellow at the Asia Center of Harvard, joining a growing list of politically connected Chinese billionaires with ties to Harvard.

Ezra F. Vogel, a professor emeritus at Harvard who wrote a biography of Deng, said he met Mr. Wu on several occasions.

“He had this staff of sharp people who were working for him,” Mr. Vogel said. “It seems that they were doing the detail work, and he was the friendly man supplying the connections.”

UC Berkeley Professor, and former U.S. Secretary of Labor, Robert Reich posted this article providing further evidence of the massive scale of foreign investment in North American real estate, driven largely by dark Mossack Fonseca money.

The Surge in Foreign Real Estate Investment in the United States

Foreign real estate investment in the United States, both commercial and residential, is a huge phenomenon that is only expected to accelerate, maybe even to skyrocket, in 2016.

In fact, the United States, New York to be exact, is the top global destination for foreign real estate investors.

The top three U.S. cities, New York, San Francisco, and Houston, also ranked among the top global cities for investors. Here is the ranking of the top global cities for real estate investment:

New York City, USA

London, England

San Francisco, USA

Tokyo, Japan

Madrid, Spain

Houston, USA

Berlin, Germany

Sydney, Australia

Shanghai, China

A strong U.S. economy is the driving factor for foreign real estate investment. Compared with other countries that are seeing an economic slowdown, such as China and Brazil, the United States makes for a safer investment.

Residential Real Estate Investment

Combine the relative strength of the U.S. economy with low interest rates and low prices after the housing crash, and you have a foreign real estate investment frenzy. From the period between April 2014 and March 2015, 8 percent of all home sales in the United States were to foreign investors.

Foreign investors buy residential real estate for different reasons. Some buy a home with the intention of it being their primary residence. But other times, foreign investors use the property as a vacation home, an investment, or as a way to diversify their assets.

Investments from China

Many foreign investors have large amounts of money, which they need to invest somewhere.China has been one of the most active players investing its capital in U.S. real estate. From April 2014 to March 2015, the Chinese invested $28.6 billion in the United States. And the investing is still happening. Chinese developer, Zhang Long, for example, bought land in late 2015 north of Dallas, Texas, to turn it into a subdivision populated with 99 McMansions for Chinese buyers.

But the Chinese buying spree in the United States didn’t start in Texas. It began in Manhattan and Silicon Valley and was a major factor in inflating home prices in those areas. California, overall, has been an attractive place for Chinese investors who often think nothing of paying cash for a $500,000 home in Orange County (mainly Irvine) or the San Gabriel Valley. And that’s just the average price. Some investors shell out millions of dollars for U.S. real estate. China’s impact did wane since its economic slowdown of 2015, but the investing lull might be only temporary.

Investments from Other Countries

Other large-scale investment activity into the United States comes from Canada, India, Mexico, and the United Kingdom. These four countries plus China made up 51 percent of all foreign purchases into the United States between April 2014 and March 2015. Although Chinese buyers focus largely on the West Coast, especially California, foreign investment in real estate happens throughout the country. Here’s a breakdown from the National Association of Realtors of where the other top foreign investors buy:

Canadians tend to buy in the warm climates of Arizona, Nevada, and Florida, mainly as vacation homes to escape Canadian winters.

Investors from India buy all over the United States, mainly as business ventures.

Mexicans tend to buy in Texas, particularly in the cities of San Antonio, Houston, and El Paso. San Diego, California, and Miami, Florida are also popular investment areas. Investments are a combination of business ventures and vacation homes.

K. investors tend to buy for business or vacation reasons in Los Angeles and San Francisco, California; New York City, New York; Orlando and Kissimmee, Florida; and Houston, Texas.

Pros and Cons of Foreign Investment

Having large amounts of money coming into the United States from foreign investors seems like a great thing. And it can be, but there is also a downside to all this foreign investment in U.S. real estate.

Pro: If you already own property in areas that are now attractive to foreign investors, you’ll see foreign investment as a benefit. Your house will be worth more with all the increased demand from foreign buyers, and you’ll probably make a profit if you decide to sell. If you decide to stay, you’ll enjoy a stronger local economy and potentially new housing developments that come with added amenities for the community.

Con: If you live in an area that’s attracting foreign investors, you might find that your neighborhood has a lot of vacant homes. Not all foreign investors, as was pointed out earlier, buy residential real estate to use as a primary residence. The home might be a vacation home that sits empty for much of the year. Or if foreign investors do intend to live in the home, it might take a long time for them to make the move from their country, again leaving the house vacant for a significant period.

Con: If you live in a hot investment area but don’t already own property there, you might be forced out of the housing market from the spike in real estate prices. Foreign investment can create a housing bubble in certain areas, making it difficult or practically impossible for Americans to buy a home in their own country. Although foreign investors typically are not in the same market as first-time homebuyers are (they are generally in a more upscale, higher-priced market), there could be a trickle-down effect that could ultimately raise prices for all price points.

Con: If you’re currently renting, you’ll probably be renting for a while longer, and rent prices will likely go up if demand increases.

Bottom Line

Whether you like the idea of foreign investors buying up property in the United States or whether you don’t, as long as wealthy foreign buyers see the United States as a safe place to park their money, the practice will continue. Although there are some cons to foreigners investing in the Unites States, the money they bring here strengthens local economies.

I am sharing this because of its particular relevance to the ongoing revelations about connections between global tax evasion shell companies and real estate markets: London, Miami, New York City, San Francisco and Vancouver.

UPDATE May 5, 2016: National Public Radio’s Takeaway news analysis program, today interviewed James Henry, senior adviser at the Tax Justice Network and a senior fellow at the Columbia Center for Sustainable Investment. He’s examined World Bank and IMF data over the last 45 years, and has found that kleptocrats have taken $12.1 trillion from developing countries. James’ interview specifically discusses the foreign dark money driving the housing markets in Miami, New York and Vancouver, providing further confirmation of my points. Audio of the interview begins at 19:45 in the podcast below.

I am sharing this because of its particular relevance to the ongoing revelations about connections between global tax evasion shell companies and real estate markets: London, Miami, New York City, San Francisco and Vancouver.

The Panama Papers—the massive collection of leaked documents from Mossack Fonseca, a Panamanian law firm that helps set up offshore shell corporations—have already had political consequences. Iceland’s prime minister, Sigmundur David Gunnlaugsson, resigned after the leak revealed that he had partly owned an offshore firm. David Cameron, the British prime minister, is facing criticism over an offshore company that his father set up. In Brazil, many of the people connected to the country’s unfolding corruption scandal appear to have held offshore shell companies set up by Mossack Fonseca. And in Russia, Sergei Roldugin, a cellist who is a close friend of Vladimir Putin, appears to control assets of over $100 million. Roldugin hasclaimed that this fortune is the result of donations from Russian businessmen to help buy expensive musical instruments for poor students. Clearly, classical music has some very generous friends among the Russian business elite.

At first glance, the Panama Papers leak looks a lot like other big leaks, such as the classified documents that U.S. Army soldier Chelsea Manningprovided to WikiLeaks or the former NSA contractor Edward Snowden’s trove of information on international surveillance. Like those leaks, the Panama Papers highlight the hypocrisy of prominent politicians and officials. The leak also recalls a series of less glamorous data leaks on the customers of secretive Swiss and Liechtenstein-based banks, which put pressure on governments to crack down on tax havens and allowed some authorities to pursue cases against tax evaders. Although few may remember, WikiLeaks began with a similar leak from the Swiss bank Julius Baer.

Yet the best comparison—and the best guide to what may happen next—is not to Snowden or Julian Assange but to Thomas Piketty, the famous French economist. Piketty’s book, Capital in the 21st Century, has been interpreted as an economic history, as a grand economic theory and a gloomy political prognosis. Yet few have paid attention to its closing pages, where Piketty lays out the political bet that underlies his research program: that people simply do not know the full extent of economic inequality, and that politics would be transformed if they ever found out.

Piketty’s research and his political program are motivated by a belief that the true extent of economic inequality is invisible. Everyday statistics simply cannot capture the extent to which the rich are different from ordinary people. They are not designed to. Common techniques of measuring inequality, by comparing the income or wealth of the top ten percent of the population to the rest, do not capture how much richer the top one percent is than the top 10 percent, or how much richer the top 0.1 percent is than the mere one-percenters. As the American political commentator Chris Hayes observed in Twilight of the Elites: America After Meritocracy, inequality is like a fractal in that it gets deeper and stranger the further one investigates it. One reason why Piketty’s research has influenced other economists is that it figures out clever ways, such as using university endowment funds as a proxy for hidden fortunes, to measure the consequences of inequality despite imperfect data.

Piketty’s aspirations may yet be fulfilled, but only if the Panama Papers create a new, self-sustaining politics that demands ever more information on the ways in which wealth is being hidden.

But the problem goes beyond deficient datasets. The truly rich have the means and the incentives to hide their staggering wealth. Piketty’s collaborator, the Berkeley economist Gabriel Zucman, estimates that $7.6 trillion is hidden in offshore arrangements. The London real estate market has been reshaped by oligarchs from Russia and elsewhere who use shell corporations to park their capital in a safe and predictable economic system. Activists run Hollywood-style bus tours of the houses of the new kleptocracy.

An activist shows fake banknotes during a demonstration outside the European Commission headquarters after the Panama Paper revelations, in Brussels, April 2016.

As the economist Branko Milanovic argues in his new book, Global Inequality, these trends are reshaping economic and political development. It used to be that economic elites had an interest in building up the rule of law in their own country, if only to protect their own property. Now they can just transfer the loot to London or New York, where “nobody will ask where the money came from,” Milanovic writes. Financial globalization is building a world similar to the one depicted in William Gibson’s grimly satirical science fiction novel, The Peripheral, in which the truly rich are unaccountable to anyone but themselves.

Piketty wants to map this hidden world and destabilize it. He believes that ordinary people simply don’t understand the extent of wealth because they aren’t able to comprehend it. There is thus an urgent need to generate new information that will help people understand how important wealth is, and who has it. This explains, for example, why Piketty wants a utopian global tax on economic capital. It’s not because such a tax would be a complete solution to inequality but because the tax would generate reporting requirements, and hence information on who holds which assets, allowing democracies to hold a “rational debate about the great challenges facing the world today” and who should pay for them.

Piketty’s perspective provides a different—and more fundamental—way of thinking about the long-term consequences of the Panama Papers. The Panama leaks, measured in gigabytes of information, are far larger than the Snowden and Manning ones. Yet compared with the true size of the offshore sector, they are less a leak than a trickle. Mossack Fonseca is not the only law firm setting up shell corporations to help people avoid taxes and scrutiny. And shell corporations are just one small part of a much larger system designed to hide people’s wealth. The document release—although significant—is no substitute for the kind of detailed and comprehensive information that a global tax arrangement might provide.

The truly rich have the means and the incentives to hide their staggering wealth.

Still, the leak brings the world one step closer toward better information on global wealth. The United Kingdom, for example, has come under pressure to stop protecting its tax haven dependencies. France and Germany are calling for a blacklist of tax havens, which might be cut off from the SWIFT financial messaging network, a global network that financial institutions use to transmit information securely, if they do not make their ownership structures completely transparent.

People demonstrate against Iceland’s Prime Minister Sigmundur David Gunnlaugsson in Reykjavik, April 2016.

Perhaps more important, in some countries the revelations are creating a new popular politics around tax avoidance and fraud. The Panama Papers have spurred massive public protests in Iceland and political furor in the United Kingdom. They are connecting technical questions of tax evasion and tax avoidance to everyday politics by identifying well-known politicians, officials, and celebrities who benefit from complex arrangements. Some of Piketty’s hopes for popular debate are being realized.

Even so, the effects have been sporadic. The revelations have had little popular impact in the United States, where no public figures have been identified as taking advantage of Mossack Fonseca. They have also yet to lead to substantial public outcry in countries such as Russia or China, where there are limited channels for public dissent. If this is indeed a first step toward identifying the true extent of global wealth inequality, it is only that.

Piketty’s aspirations may yet be fulfilled, but only if this release of information creates a new, self-sustaining politics that demands ever more information on the ways in which wealth is being hidden. This is a tall order given the complexities of international politics and the incentives for individual states to cheat, but the world is significantly closer to it now than anyone would have predicted three weeks ago.

This is a metaphorical essay on personal ethics, worthy of a serious read and contemplation. When I saw the title I was intrigued but suspected it had something to do with Andy Grove’s adage, “sewage flows downhill,” which means “if anything bad happens it will eventually flow down to you.” This is about ethics. The points made here are particularly apt in light of the huge number and sheer scale of recent business frauds: the Volkswagen fraud, LIBOR, Lehman Brothers, Bernie Madoff’s pyramid scheme, Conrad Black in Canada, Olympus in Japan, Bernie Ebbers and Worldcom, Tyco International, stretching back all the way to Enron, Michael Milken’s junk bonds, and the 1980’s savings & loan debacle.

This is a metaphorical essay on personal ethics, worthy of a serious read and contemplation. When I saw the title I was intrigued but suspected it had something to do with Andy Grove’s colorful adage, “sewage flows downhill,” which means “if anything bad happens it will eventually flow down to you.” This is about ethics. The points made here are particularly apt in light of the huge number and sheer scale of recent business frauds: the Volkswagen fraud, LIBOR, Lehman Brothers, Bernie Madoff’s pyramid scheme, Conrad Black in Canada, Olympus in Japan, Bernie Ebbers and Worldcom, Tyco International, stretching back all the way to Enron, Michael Milken’s junk bonds, and the 1980’s savings & loan debacle.

This is only a small selective list and many will be able to think of many other well-known scandals. The problem is that there are no easy answers in many situations. How much do we risk by taking an ethical stand on an issue, and the fact that the bigger the issue the bigger our personal risk? It is very existential. At the same time appear to have learned nothing from all these recent scandals, tightened regulations or changed personal behavior. A recent study of Wall Street brokers suggests that most would still commit fraud, if they benefited substantially, and believed that they would not be prosecuted for it.

Some years ago I heard an analogy that resonated with me. It was a description of learning something – some piece of information about a person’s character – that was so negative, so vile, that no matter what else you knew about that person, you instantlyunderstood the core of the person in question. There is, in fact, a folk-wisdom saying that illustrates this concept, which I first heard on a talk radio show: “That tells me everything I need to know about him.” Ironically, the talk radio host from whom I first heard this expression was revealed to have done something I consider so vile that, even before he was taken off the air, I realized that deed (plus his “Yeah, so what?” attitude) told me everything I needed to know about him – and I stopped listening… and having stumbled across his new broadcast home while channel-surfing, I still refuse to listen to him.

Before I dig into this, I want to be clear – nobody is perfect. We all have our flaws, being human beings, and need to be forgiving and tolerant. We all struggle with weaknesses and sin, and while Jewish I’ve found I like the instructional concept of the Seven Deadly Sins (and the other side of the coin, the Seven Cardinal Virtues), and am convinced that while all these are human weaknesses, each person has their “one sin” with which they wrestle as their dominant weakness. And in that struggle with and – hopefully – victory over it do we demonstrate that we are more than a collection of chemicals and cells, but sentient creatures striving to improve ourselves.

So… this analogy goes as follows:

Imagine you have two cups. One contains the purest, clearest, most wonderful water possible. The other, raw sewage. When you mix the two, you get sewage. The same for a cup of sewage and a pitcher of water, or a barrel of water. Regardless of the size of the pure water container, the sewage contaminates it.

This became the root of what I refer to as “The Rules of Sewage” in regards to a person’s character. This one is the First Rule of Sewage, The Non-Proportional Rule of Sewage. It means, as the saying above goes, that you can sometimes learn a thing about a person that taints the entirety of their personality – e.g., a person beats their spouse. It doesn’t matter what else they are, what acts they do, they are polluted by that one thing.

This simmered in my mind over a couple of years, and I started to formulate other Rules of Sewage. Each was based on the same base concept – mixing water and sewage. Thus far I’ve come up with six.

The Second Rule of Sewage is the Non-Compartmentalized Rule of Sewage. You cannot pour a cup of sewage into a container of water, and have it only remain in the place you poured it. Bad character leaks into other elements of character. E.g., a person who cheats on their spouse – thus breaking a sacred oath – cannot be counted on to keep an oath in any other part of their life.

The Third Rule of Sewage is the Immersive Rule of Sewage. Imagine an edible fish taken from that pure water, placed in sewage, and somehow surviving – no matter the fish’s immune system and other defenses, it will become contaminated. No matter how pure you are to begin with, if you are surrounded by bad people or bad content, it will start to affect you. E.g., a good, honest person who goes to work in a place with bad ethics and stays there – for whatever reason – will sooner or later find they are making compromises to their own character and standards, and rationalizing their doing so. (And this is, of course, the root of the proverb “Birds of a feather, flock together.”)

The Fourth Rule of Sewage is Irreversible Rule of Sewage. Simply put, it’s a lot easier to mix the sewage in and ruin the water than reversing the process. While people are certainly capable of change, it takes deliberate effort to do so, and usually also an ongoing awareness and maintenance of that change to avoid slipping back to whatever factor is being avoided.

The Fifth Rule of Sewage is the Odiferous Rule of Sewage. Sewage, to put it bluntly, stinks like sh*t. Bad odors like that can be covered up or contained, but not forever. Sooner or later the malodorous item in a person’s character will out, and be readily apparent. This actually ties in with…

The Sixth Rule of Sewage, the Reactive Rule of Sewage – when faced with a tank of sewage, normal people react negatively. And while a person learning something about another (ref: Rule One) won’t physically turn their head away and scrunch up their face in disgust, I believe the plain truth is that upon learning of such a think will cause a decent person to dissociate – to whatever degree possible – from the other. Failing to do so, or worse expressing approval, could be considered an example application of Rule One about them too.

In putting this concept “out there” it will be interesting to see if other Rules of Sewage develop in the comments.

Pfizer’s announcement this week of its intricate $160 Billion merger/acquisition with Irish pharmaceutical company Allergan, revealed that Pfizer will be moving the new corporate headquarters to Dublin. Essentially, Pfizer, the much larger company, is providing a bridging loan to Allergan to purchase Pfizer so that it may move to Ireland. This enables Pfizer to avoid paying U.S. taxes, even after receiving massive support for R&D from U.S. government programs.

Pfizer CEO Ian Read

Pfizer’s announcement this week of its intricate $160 Billion merger/acquisition with Irish pharmaceutical company Allergan, revealed that Pfizer will be moving the new corporate headquarters to Dublin. Essentially, Pfizer, the much larger company, is providing a bridging loan to Allergan to purchase Pfizer so that it may move to Ireland. This enables Pfizer to avoid paying U.S. taxes, even after receiving massive support for R&D from U.S. government programs. Pfizer CEO, Ian Read, has deflected questioning about the apparent tax avoidance scheme by simply saying that the price of the deal would have been different had Pfizer bought Allergan and remained in New York. Needless to say, the reaction to this has been swift and harsh from many quarters.

Colorfully named offshore tax avoidance strategies like the “Dutch Sandwich” and the “Double Irish” have been superseded by wholesale corporate uprooting and transplantation in foreign jurisdictions. Ireland is particularly notable for its favorable tax treatment of foreign companies, which has attracted the attention of the EU and U.S. tax authorities. Burger King’s merger with Tim Horton’s and corporate move to Canada is a recent case. KPMG Canada’s Isle of Man scheme, while designed for high wealth individuals, is another example. The Pfizer/Allergan merger is a barely disguised form of corporate tax evasion that is for the moment legal, and evidence of the return of a Gilded Age of corporate excess and plutocracy. It is a social and political issue of the highest order, not to mention business ethics.

Included here is today’s editorial from the New York Times.

Pfizer’s Big Breakthrough: Global Tax Avoidance

The $160 billion deal to combine Pfizer and Allergan, the maker of Botox, does not appear to be illegal. But it should be. This merger is a tax-dodging maneuver that enriches shareholders and executives while shortchanging the public and robbing the Treasury of money that would pay for a host of government programs — including education, scientific research and other services that also benefit corporations.

Pfizer, with a market value of nearly $200 billion, will be acquired by the smaller Allergan, which is run from New Jersey but technically headquartered in Ireland. This will allow Pfizer, which is based in New York, to pass itself off as Irish as well. Once the paper shuffling is complete, much if not most of Pfizer’s earnings — including those that are made in the United States — will be taxed at global tax rates that are generally lower than American tax rates.

In recent years, dozens of American companies have used similar tactics, known as inversions, to reincorporate in Ireland, Britain and other countries with lower corporate tax rates than those in the United States — at a cost to the Treasury conservatively estimated at $20 billion over 10 years. Pfizer’s merger is by far the largest such move.

But if it’s a loss for taxpayers, it’s a great deal for Pfizer. As with other companies that have “inverted,” the only thing it has to lose is its tax obligations. Inverted companies almost invariably keep their headquarters and top executives in the United States. They remain listed on United States-based stock exchanges, where they raise capital under the protection of American securities’ laws. The newly combined Pfizer Inc. and Allergan P.L.C., for instance, will be renamed Pfizer P.L.C. and trade under the ticker symbol PFE, Pfizer’s current symbol, on the New York Stock Exchange, according to The Wall Street Journal.

In addition, inverted companies continue to enjoy the protection of patent laws in the United States, as well as their connections, official and unofficial, with federal research agencies — all of which are crucial to drug-company profits. Contrary to popular belief, much high-risk, pathbreaking research and development can be traced not to the big drug companies but to taxpayer-funded research at the National Institutes of Health.

Traditionally, corporate taxation was a way to repay the public for benefits companies received from federal support. But in recent decades, corporate taxes as a share of federal revenue have shriveled. Inversions will only worsen that trend, effectively bolstering corporate profits at the expense of the public.

Pfizer executives, and the executives of inverted companies, don’t put it that way. They say they cannot remain competitive if they have to pay tax on profits at the relatively high United States top rate of 35 percent.

That claim does not stand up. American multinationals routinely take advantage of write-offs that reduce the top rate to a much lower level. Moreover, even an inverted company is supposed to pay tax on earnings generated in the United States at American rates. But by having a foreign parent company in one country — Ireland in this case — while remaining headquartered in the United States, a company can lower its tax bill through an accounting gimmick known as “earnings stripping,” in which profits from the United States are shifted to the foreign parent in the lower-taxed country, thus reducing the American tax bill.

It is not hard to write legislation and draw up rules outlawing inversions, and bills currently in Congress could put a stop to them quickly. What is lacking is political will to tell powerful corporate interests to stop. The Treasury Department under President Obama has issued rules to curb the practice. But the Pfizer and Allergan hookup is expected to get around these constraints. The administration could do more, but even more aggressive executive action would not be as effective as robust legislation.

Reincorporating abroad is a sophisticated variation on the old practice of avoiding corporate taxes by renting a post office box in the Caribbean and calling it corporate headquarters. Congress put a stop to those tactics in 2004. It is past time to shut down inversions as well.